Why is there no TARGET2 debate in the US?

Both Target2 and ISA balance have risen considerably since the outbreak of the crisis. We address the differences and similarities between ISA and Target2 imbalances and argue that without a well-functioning interbank market only two options remain: mounting or discounting.

Our previous blog post on Target 2 imbalances received a lot of attention and generated a couple of questions. TARGET2 is a real-time gross settlement system operated in central bank money by the Eurosystem that lies at the basis of the European Monetary Union (EMU). It provides payment and settlement services to both public and private market participants (see here for institutional details). Euro area national central banks (NCBs) can build up gross and net claims and liabilities through Target2 over time, in principle without limit. Since it became clear that these balances of Euro area NCBs have strongly increased, a lively debate on this subject has emerged, see for example this contribution by Willem Buiter, Ebrahim Rahbari and Juergen Michels for a detailed discussion. The US also has its mechanism for settling imbalances between Federal Reserve Banks (FRB) called the Interdistrict Settlement Accounts (ISA). In this post we discuss the differences and similarities between ISA and Target 2 imbalances.

Imbalances inside a monetary union arise in different ways

ISA imbalances in the US can arise in two ways. First, they may stem from capital movements across district borders. If clients of banks registered in Richmond move deposits to banks registered in New York, deposits at the FRB in Richmond fall and at the FRB in New York (FRBNY) rise. A decrease in the FRB Richmond’s ISA balance and an increase in the FRBNY ISA balance compensate this flow. The more likely origin of ISA imbalances is, however, a second channel, which rests on the FRBNY conducting open market operations on behalf of the other FRBs.

Since the Lehman bankruptcy, the FOMC decided to buy assets on a large scale to ensure market liquidity, reduce interest rates and ensure the stability of the US banking system. These open market operations are executed by the trading desk of the FRBNY on behalf of the FED-system: if the FRBNY buys an asset, each FRB receives a percentage of that purchase as an asset in the form of a claim on SOMA holdings and incurs a liability on its ISA balance. The percentage is according to the FRB’s weight in the US system, which fulfills the role of the ECB capital shares. Note that as a result, the asset mix of two regional FRBs will be comparable in quality.

When assets are purchased from a counterpart with a depository account at one of the FRBs, this particular FRB then credits the counterpart’s depository account, which increases the liabilities of that FRB. This increases the FRBs ISA balance, while the ISA balance of the FRBNY is decreased. While on an aggregate level the ISA balances cancel, assets and liabilities at the FRB level do not need to match. The differences result in ISA imbalances. If more assets are bought from banks registered in Dallas, the Dallas Fed has larger bank deposits (liabilities) and a larger, positive ISA balance (asset) to compensate.

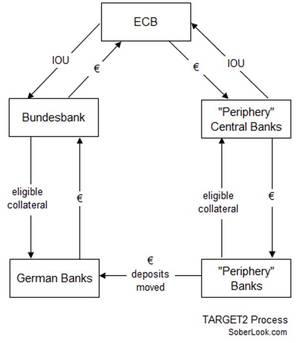

In the Euro area, the national central banks handle most open market operations themselves, so limited imbalances arise through that channel. Here, target2 imbalances are the result of capital movements across national borders, just as ISA imbalances can result from interdistrict capital transfers. As a result of this decentralized system and in contrast with the US, the quality of collateral held can differ across National Central Banks. The mechanisms underlying the imbalances are therefore somewhat different: in the US they are primarily the consequence of purchases of securities by the FRBNY. In the EMU area they are the result of capital fleeing from one country’s banking system to another. Below is a graph illustrating the effect of capital flight taken from soberlook.

Figure 1: graph illustrating Target 2 imbalances

But both imply a malfunctioning financial system

In both cases, however, we would argue that sustained imbalances signal a malfunctioning financial system. In a well functioning interbank market, liquidity is shifted by the participants to the point were it is most needed. Currently, the Target2 or ISA system takes on this role. As the Bundesbank points out on page 52 of their Jahresbericht 2011, there is no liquidity creation via the Target2 system, only liquidity movement. In other words, liquidity movement by the official channels is cheaper than by the market. If this were not the case, the market would arbitrage the imbalances away: commercial banks would make a loan to each other that results in a countering capital flow in the system, cancelling to a large extent the imbalances.

A persistent positive balance of a national central bank or FRB implies that member banks deposit additional funds voluntarily; the central bank has additional liabilities to the banking sector. Voluntary deposits carry relatively little interest: currently 0.25% in the Euro area as well in the US. As banks can get much higher yields on the interbank market at higher risk, this implies that they are not willing to take that risk. At the other end of the spectrum, a central bank with a persistent negative balance, lends additional funds to member banks. That banks are interested in borrowing more from their central bank indicates that they cannot borrow it at this price from other banks on the interbank market. Clearly, the fact that the ECB currently offers unlimited allotment at 1% interest, makes official lending relatively inexpensive, which risks crowding out the interbank market.

Size of imbalances is comparable

What about the differences in size of the imbalances in the US and EMU? As Professor Sinn notes in his latest contribution to the debate on Target 2, imbalances in terms of GDP the US are a roughly factor of 4 smaller than in the EMU. But these imbalances emerge from the banking sector and their structure of very different in the US and in Europe it is natural to relate them to the size of the banking sector rather than the size of GDP.

This puts the relative importance of the imbalances in the EMU and US in a new perspective. As the EMU banking sector is much larger than the American one, the imbalances in the US are comparable to those in the EMU. According to the FED, the total size of the US banking sector in 2011 is approximately 12,625 billion dollar, while according to the ECB the total size of the banking sector in EMU countries equals 33,722 billion euro. Given an exchange rate of approximately 0.75 the ratio of banking US banking assets to EMU banking assets is roughly 3.6. In terms of banking sector assets, the ratio of imbalances in the US and EMU drops to roughly 1.4.

Table 1: Target 2 and ISA liabilities compared

|

|

Amount |

As % of 2011 GDP |

As % of banking sector assets |

|

EMU |

892 billion euro |

9,4 |

2.6 |

|

US |

245 billion dollar |

1.7 |

1.9 |

Decentralized versus centralized ownership matters

The Eurosystem is effectively owned by the European national governments (although the ECBs capital is held by the National Central Banks, national governments are the ultimate beneficiaries), each for a proportionate share according to its ECB capital key. In the US, the FRBs are effectively owned by the federal government.

In our previous post, we wrote that in the US, the FRBs are owned by the federal government. Koning noted however that this is not entirely correct: the equity of the FRBs is owned by their member banks (i.e. private banks). These, however, are not regular shares, but entitle the shareholders to a fixed 6% annual return on equity by the Federal Reserve Act. The net earnings minus 6% times the total equity value are transferred to the US treasury. In 2010, the FRBNY paid out a dividend of 455 million USD to its shareholders, while it paid out 39 billion USD to the federal government.

We couldn’t come up with a realistic scenario in which the FRBs member banks could credibly be asked to bear ultimate risk i.e. recapitalize their FRB. The US federal government is the residual beneficiary and should thus bear the ultimate risk, so member banks will not be willing to chip in. Neither will they be able: when ISA liabilities mount in a particular district, the banks there have turned to central bank financing as a replacement for interbank financing. Such a banking sector will not be able to recapitalize its central bank, precisely because these imbalances reflect the inability of the banking sector to secure private funding. For these reasons, for practical purposes, we think of the federal government as the owner of the FRBs.

But implications depend on your view of a monetary union

Although the need to eliminate imbalances is unclear, let’s look at different policy options for the US and EMU in order to manage these imbalances. In the long run, we argued that imbalances would be eliminated if the financial system were to return to health and the interbank market were to function fully. To eliminate these balances in the short run, they can be settled or discounted. (For those who missed our previous post, in the US, the annual settlement hasn’t taken place since 2008.) Settlement is currently not feasible; it would completely drain some European central banks and some FRBs of their assets and prevent them from providing necessary central bank money to the financial institutions in their jurisdiction.

In response to our previous post, JP Koning, who provides an excellent explanation of the workings of ISA in his idiots guide, correctly noted that settlement takes place via SOMA holdings and not Gold Certificates. Indeed, the accounting manual states that: “the adjustment that would be required in each Bank's gold certificate total is applied by the New York Reserve Bank against each Bank's holdings in the System Open Market Account.”

Is discounting feasible? Discounting implies that regional central banks write down (part of) their interdistrict claims. As Koning pointed out, this has happened in the US during the great depression. As these claims add up to zero, this has no impact on the gains and losses of shareholders aggregated over all districts. Whether you worry about discounting these claims depends on your idea of what being in a monetary union implies. If you view a monetary union as a temporary bundle of nation states that happen to have the same currency, the continued existence of the monetary union depends on the support by the nation states. Discounting your central banks claims on other central banks then constitutes a transfer of assets. If you view a monetary union however as an irreversible project that comes with mutual obligations and responsibilities, discounting may be viewed as an accounting operation that concerns only central bankers as overall profitability is unaffected.

Thus, the centralized structure of the US system reduces the probability of the decision to discount to become politicized. If the possibility of the monetary union breaking-up is non-zero, then discounting has material consequences. As in our view leaving the euro is the reverse operation of joining, a departing central bank is entitled to assets and liabilities according to its capital share in the system. The composition of these assets and liabilities is then relevant. In that case, discounting claims now might lead to a transfer from one country to another later.

In the end, unhealthy banking sectors remains problematic

In both EMU and US, allowing the claims to mount (the European solution) or discounting (the 30s solution) will be the only way ahead in the short run. In the long run, however, the imbalances will disappear if the banking system is returned to health.

The most important difference is the distribution of any losses incurred due to the support given to the banking system. Both in the EMU and in the US, the central banks have a large amount of assets on their books, which are of relatively low quality. In the US, the central government, which is the prime beneficiary of FED revenues, will bear the losses. In the Euro area, however, profit and losses of the ECB are distributed according to the national central banks’ capital keys. If these losses arise largely due to collateral offered by Greek commercial banks to the Greek central bank for instance, other countries will effectively (through lower dividend payments by the ECB) have financed retroactively a bailout of the Greek banking system while the distributional consequences of this support would have escaped public scrutiny. This raises one more time the question of a proper European discussion about the creation of a proper banking crisis resolution framework.

About the authors

Related content

Six lessons for Europe from the nationalization of SNS Reaal

Recently the Dutch government nationalized the Dutch financial conglomerate SNS Reaal. The intervention was the first use of the Intervention Act

Who’s afraid of the AQR?

Banks have incentives to recapitalize in socially undesirable ways and to hide losses on their balance sheets. Will the comprehensive assessment solve

Cross-country insurance mechanisms in currency unions

Countries in a monetary union can adjust to shocks either through internal or external mechanisms. We quantitatively assess for the European Union&nbs

The changing landscape of financial markets in Europe, the United States and Japan

We compare the structure of the financial sectors of the EU27, Japan and the United States, looking at a set of 23 indicators.