Blogs review: The Baltic experience

What’s at stake: The Baltic economies of Latvia, Lithuania, and Estonia have recently taken center stage in macroeconomic policy discussions as advoca

What’s at stake: The Baltic economies of Latvia, Lithuania, and Estonia have recently taken center stage in macroeconomic policy discussions as advocates of internal devaluations have pointed to these countries as examples that could be generalized to the euro area periphery. These experiences certainly show that large front-loaded consolidations are, sometimes, politically acceptable. And that adjustment under a fixed exchange rate regime (or within a currency union for the case of Estonia) is, after all, possible. But, given the large economic costs associated with these strategies and the specific circumstances under which these adjustments were made possible, it is far from clear whether these experiences should qualify as success stories and are generalizable.

The Baltics as a success story

Mark Griffiths – the IMF mission chief for Latvia – writes that Latvia, a nation of about 2.2 million people bordering the Baltic Sea went through the most extreme boom-bust cycle of the emerging market countries of Europe. Back in the dark days of December 2008, many doubted that Latvia—which joined the European Union in 2004 together with its Baltic neighbors Estonia and Lithuania—would be able to stick to the tough economic program it had just agreed with the IMF and the European Union. But it did. Against the odds, it successfully completed its IMF-supported program in December 2011. Today, Latvia is one of the fastest growing economies in the European Union. Real GDP grew by 5½ percent in 2011, and is now projected to expand by 3½ percent in 2012, a number that possibly will come out even higher.

Dani Rodrik writes that Latvia rejected much external advice and did not devalue, despite a huge current account deficit that exceeded 20% of GDP in 2007. The lat had been pegged to the euro in anticipation of Eurozone entry and the government refused to do anything that would jeopardize that goal. The IMF were told to go home if they were going to insist on devaluation. In the end, the country implemented a radical fiscal contraction that pushed the country back into external surplus. The shock produced a loss of output of almost 20% of GDP in one year, and a rise in unemployment to 18.4% (from 6% in 2007). By 2011, the worst seemed over and the economy grew at a healthy rate of 5.5%, one of the highest in Europe.

Charlemagne writes that at a time of acute gloom, EU and IMF bigwigs see hope in this Baltic resilience. Jörg Asmussen – a member of the Executive Board of the ECB – said in a recent speech that Latvia offers an example to troubled euro countries of how to carry out an internal devaluation. External devaluation was presented as the only way forward. But Latvia did not choose the easy “quick fix”. It embarked on a courageous fiscal consolidation path and structural reforms. Two years later, the speed of the economic rebound is as extraordinary as the depth of the recession.

Collapse + moderate recovery = success !

Mark Weisbrot writes that it is amazing to hear Christine Lagarde calling Latvia a "success". It is like calling the Great Depression a success – after all, the US economy did eventually recover in the 1940s. And the US lost a comparable amount of output during 1929-33 to what Latvia lost in just two years (2008 and 2009).

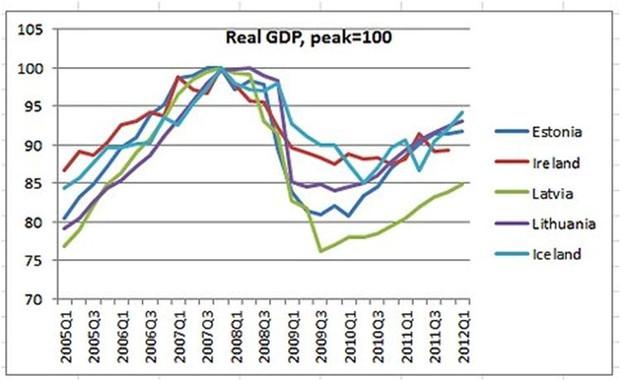

Paul Krugman writes that one year of pretty good growth after an incredible decline — growth that still leaves you 15 percent below previous peak — is not exactly a proof of concept for fiscal austerity. Simon Wren-Lewis writes that by the logic that when growth returns you can call this success, an even better strategy is to close the whole economy down for a year. The following year we could get fantastic growth as the economy starts up again.

Mark Weisbrot and Rebecca Ray write in a CEPR paper that the average loss for countries with devaluations in crisis situations was 4.5 percent of GDP. This compares to a loss of 24.1 percent of GDP for Latvia during its recession, while it kept its exchange rate fixed. More importantly, three years after these large, crisis-driven devaluations, most of the countries are considerably above their pre-devaluation level of GDP three years later. The average economy is up by 6.5 percent over their pre-devaluation level of GDP. Latvia, by contrast, is down 21.3 percent of GDP, three years after the crisis began.

Paul Krugman also notes that the decline in unemployment has a lot to do with a huge fall in the labor force, driven to an important extent by emigration.

The adjustment of the external balance

Paul Krugman argues that there’s no obvious sign that Latvia’s balance of payments experience represents more than a big trade balance improvement thanks to a huge economic contraction, with the deficit reemerging as the economy bounces back a little.

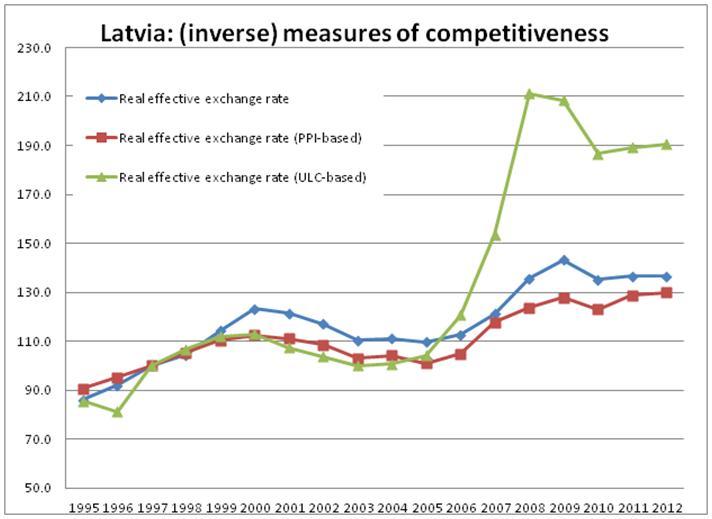

Dani Rodrik writes that even though Latvia’s external imbalance was eliminated, it is not clear that there has been a sizable improvement in competitiveness. The much-vaunted internal devaluation has been small. Wage cuts have been mostly in the public sector, where they don’t really help with export competitiveness. Private sector wages have been surprisingly resilient. As the next chart shows, the unit labor costs-based measure of the real exchange rate has come down (depreciated) only moderately, following a huge rise over 2004-2008. Consequently, it is not at all clear whether Latvia has regained sufficient competitiveness to sustain growth without running sizable external deficits yet again.

The Baltic experience and the euro area periphery

Ryan Avent writes that internal devaluation work under the following conditions:

1. The economy in question is willing to suffer.

2. The economy is small and open.

3. The economy has flexible labour markets, especially in wage contracts.

4. The economy has a relatively small debt stock.

5. The economy's major trading partners have relatively healthy economies.

But exactly for these reasons, internal devaluations are less likely to work for the euro area periphery. As much larger economies, domestic demand is a more important component of output, and a much larger increase in trade is necessary to restore growth. As heavily indebted economies, internal devaluation makes debt burdens harder to service, raising the prospect of defaults or crises. And because most of their major trading partners are in recession, often because they're also trying to devalue.

The Baltic experience and the frontloading of fiscal consolidation

Olivier Blanchard writes that over the first two years of the program, the cyclically adjusted primary balance was increased by 11% of GDP. Whether a slower adjustment would have led to less of an overall output loss just cannot be assessed. The Latvian experience makes, however, a strong political case for taking into account adjustment fatigue. While the large initial budget cuts went through relatively easily, taking much smaller steps proved much more difficult in the 2011 budget. The political argument for frontloading thus strikes me as fairly strong. So does the political argument for focusing on spending cuts initially. Targeted spending cuts are typically more costly politically than general tax increases; thus it may be better to keep those tax increases in reserve for later, if and when fatigue is settling in.