Introducing the Bruegel dataset of sovereign bonds holdings (and more)

Early this year Jean Pisani-Ferry and I wrote a policy contribution titled “Who’s afraid of sovereign bonds”, where we were investigating the role of euro area banks in holding of domestic government debt securities, one of the important aspects of the sovereign-banking crisis loop.

In order to do so, we needed to know how the share of domestic banks in total holdings had evolved over time. This required a breakdown of sovereign bond holdings by the different sectors of the economy, for each country and at the highest possible frequency. But in the process, we discovered that there is neither a single source for this kind of information, nor any common practice across the institutions providing the data[1].

We therefore constructed a new cross-country database of sectorial sovereign bond holdings, gathering publicly available data provided by national authorities on a country-by-country basis. The project required time and effort, but now we have data on sectorial holdings of sovereign bonds for 12 countries (Belgium, Finland, France, Germany, Greece, Ireland, Italy, Netherlands, Portugal, Spain, UK and US). Data go back for most of the countries to the late Nineties and are mostly at quarterly frequency.

The sectorial breakdown provided by national authorities usually differs across countries, complicating to some extent the cross-country analysis. We therefore complemented the original data with a synthetic and standardised re-classification, based on 5 categories identical for all countries (banks, central banks, public institutions, other resident sectors and non-resident holders).

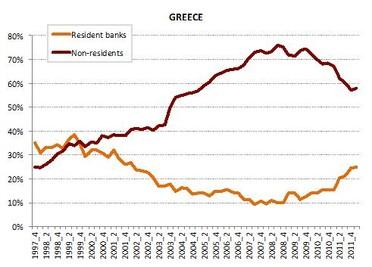

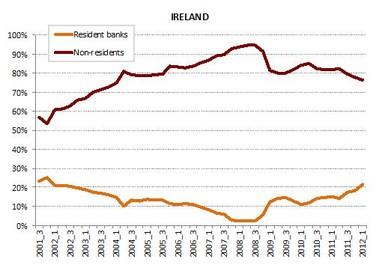

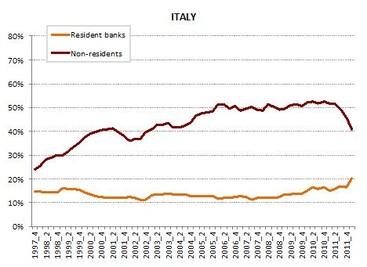

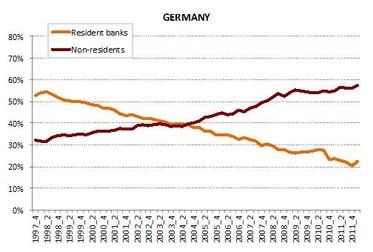

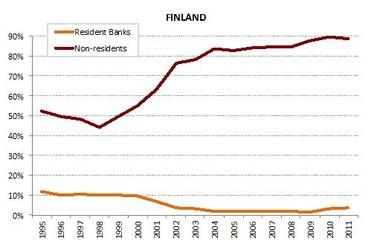

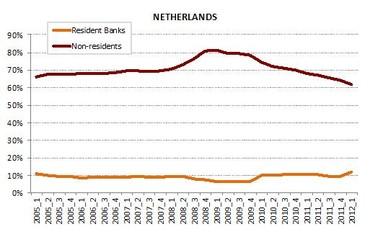

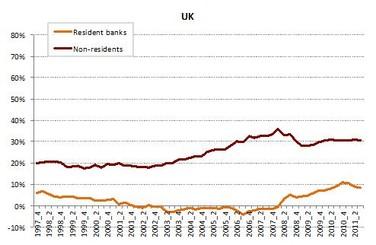

Share of resident banks and of non-resident investors in the total holding of sovereign bonds

(selected countries)

Source: Bruegel dataset of sovereign bond holdings. See explanatory notes in the excel file for definitions and explanations.

Figure 1 gives an example of the informative potential of the data, plotting the share of sovereign bonds held by domestic banks against the share held by non-residents for selected European countries. As we were showing in February, a pattern emerges across the euro area periphery, where foreign investors have been off-loading risky bonds that have been increasingly absorbed by domestic banks. This process has continued and for countries like Italy and Spain it has accelerated, pointing to an increasing fragmentation of the sovereign bond markets. In Spain the situation is particularly striking, as the relative positions of non-residents and domestic banks have inverted and are back to the pre-euro level of 1999. Germany on the other hand has seen no flection in the increasing trend of on-resident holdings, benefitting from the “flight to quality” from the periphery.

To our knowledge, this is the first cross-country database on sectorial bond holdings that covers almost all the sovereign issuer of the euro area and we believe that it could therefore add a significant value to the existing sources. For this reason, we have decided to make it publicly available on Bruegel’s website, subject to the only request that users quote as a source the Bruegel dataset on sovereign bond holdings and the original paper (Merler, S. and Jean Pisani-Ferry (2012), “Who’s afraid of sovereign bonds?”, Bruegel policy contribution 2012|2, February) for which the dataset was constructed. The dataset published on our website will be updated quarterly, to incorporate the latest data releases.

This paper is part of a more comprehensive work we at Bruegel have been doing on capital flights, sovereign-banking loop and financial fragmentation in the euro area. We are planning to publish further datasets gradually, hoping to make a further contribution to the analysis and policymaking of the financial crisis.

Download dataset in XLS format

Who's afraid of sovereign bonds?

[1] EUROSTAT conducts a survey and provides data on the breakdown of government debt by country but they are only annual and they do not disaggregate banks within the sector of financial corporations.

About the authors

Related content

Is the current crisis management framework enough for the age of digital bank runs?

Fast and furious: how digital bank runs challenge the banking-crisis rulebook

The speed of recent bank failures has shown the need for more systemic protection of the financial system.

How Europe can sustain Russia sanctions

Russia's war in Ukraine has underscored the need for Europe finally to invest more in its own defence and security. Such an outrageous act of aggressi

The microeconomics of Christmas

Review of major contributions to the literature on the controversial topic of the deadweight loss of Christmas.