Austerity needed to start, now we need a fiscal union

The main driver of public debt increases in the last 4 years has been high public deficits, not austerity. Budget consolidation is necessary to avoid

The main driver of public debt increases in the last 4 years has been high public deficits, not austerity. Budget consolidation is necessary to avoid excessive increases in debt levels. The central question is about the best moment to pursue the adjustment. I provide a simple scenario analysis, which suggests that fiscal adjustment should be gradual in order to balance risks. Arguably, adjustment has been gradual in some though not all countries considered. The simulations suggest that significant recessions are still ahead of us. This calls for a Marshall plan for Southern Europe and a more forceful use of restructuring and resolution tools. Contracts could be a good way of providing fiscal support in exchange for reforms.

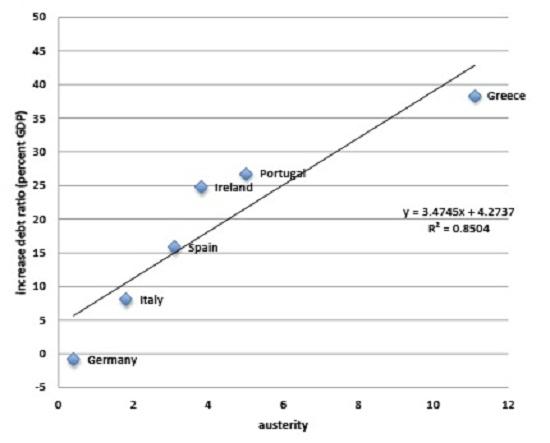

Paul de Grauwe and Yuemei Ji in a recent blog post study market induced austerity and its consequences. I disagree on a number of points and would like to present my view. The authors look at the speed of fiscal adjustment in Greece, Ireland, Portugal, Spain, Italy and Germany and find that more adjustment was applied in countries with higher spreads. My first disagreement is on the sample studied. The speed of adjustment in Greece, Ireland and Portugal was essentially determined by the Troika and all three countries were not on the market. So it is not clear why markets were really the determinant here. They continue to argue that budget consolidation has been hurting growth, a statement which most economists including myself agree with. However, they also claims that austerity is the main driver of the increasing debt – accordingly, budget consolidations do not even help getting the fundamentals fixed. For convenience, I reproduce their graph here.

Source: de Grauwe and Yi (2013)

According to their estimates, a budget cut of 1 percentage point would lead to a 3 percentage point increase in the debt ratio. This cannot be right even assuming extremely high multipliers. Something must be spurious here.

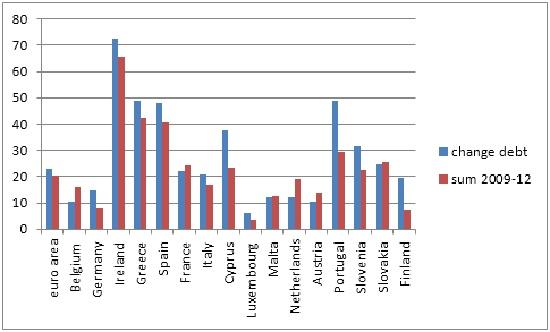

So what has been the real driver of increased debt levels? Well, I would content it has been the high deficit levels that several euro area countries have had in the last couple of years. Below, I show a simple graph comparing the accumulated deficits with the change in the debt level, both measured in percent of GDP.

Figure: Deficits and debt in euro area countries, 2009-12

Source: European Commission, February 2013 forecast.

The graph is striking: Countries that have been running high deficits in the last 4 years all have had their debt levels increase very substantially. The correlation coefficient is 92.3%. Take the case of Spain. Four years of budget deficits of around 10 percent correspond to an increase of Spanish debt by 48 percentage points leading to a debt to GDP ratio of 88% at the end of last year. Repeating the same exercise only for 2011 and 2012 still results in a correlation coefficient of 81% (adjustment for the Irish case and the debt restructuring in Greece would likely change result). Italian debt equally increased by more than 20 percentage points and is now above 120%. Or to put it bluntly: borrowing leads to debt and that effect is first order. So there is no question that deficit levels have to adjust or else public debt to GDP ratios will explode.

This is why Paul de Grauwe at the end of his piece does agree that fiscal consolidation will eventually be needed. The really big question should thus be about the right moment to consolidate and the speed of consolidation. This is basically a question about the assumptions we have on fiscal multipliers. Let’s compare 3 different scenarios in a simple simulation. The first scenario is one of a gradual fiscal adjustment with half of the adjustment done in the first period and the second half done in the second period and assuming that the multiplier declines. The second scenario is one where no adjustment is done in the first period and all the adjustment is done in the second period when the multiplier is lower. The third adjustment equally has all the adjustment in the second period but the multiplier – contrary to expectations – has not come down. Paul de Grauwe estimates the multiplier to be 1.4 so I take this as the high multiplier and 0.7 as the low multiplier, which is in line with most of the empirical literature on multipliers. I start from a deficit of 10%, which corresponds to Spain’s current deficit.

A number of interesting results emerge. First of all, the debt to GDP ratio ends up almost the same in the first and the second scenario while in the third scenario it is significantly higher. Second, the second scenario is more favourable in terms of the decline in GDP than the first one. In the first scenario, it declines by 10.5% while in the second scenario the decline amounts to only 7%. This is a strong argument for delaying the fiscal adjustment. However, the third scenario offers a strong warning. In the third scenario, the decline in GDP is even more dramatic amounting to 14% and the debt to GDP ratio explodes.

|

t0 |

t1 |

t2 |

||

|

Scenario 1: gradual fiscal adjustment and gradual decline of multiplier |

Deficit |

10 |

5 |

0.0 |

|

debt |

90 |

100 |

105.0 |

|

|

gdp |

100 |

93 |

89.5 |

|

|

debt/gdp |

90% |

108% |

117% |

|

|

deficit/gdp |

10% |

5% |

0% |

|

|

multiplier |

|

1.4 |

0.7 |

|

|

Scenario 2: postpone fiscal adjustment to second period when multiplier is small |

deficit |

10 |

10 |

0.0 |

|

debt |

90 |

100 |

110.0 |

|

|

gdp |

100 |

100 |

93.0 |

|

|

debt/gdp |

90% |

100% |

118% |

|

|

deficit/gdp |

10% |

10% |

0% |

|

|

multiplier |

|

1.4 |

0.7 |

|

|

Scenario 3: Postpone fiscal adjustment to second period, but multiplier remains high |

deficit |

10 |

10 |

0.0 |

|

debt |

90 |

100 |

110.0 |

|

|

gdp |

100 |

100 |

86.0 |

|

|

debt/gdp |

90% |

100% |

128% |

|

|

deficit/gdp |

10% |

10% |

0% |

|

|

multiplier |

|

1.4 |

1.4 |

|

Debt dynamics are likely to be worse due to two additional factors not considered here. The decline in prices as well as the interest rate effect on debt dynamics. Both factors call for earlier adjustment.

The big question is what we assume will be the magnitude of multipliers today and tomorrow. As regards current multipliers, most economists argue that it is higher than normally. While I do not find the evidence all that conclusive, I do agree that it probably is higher. So let’s say today’s multipliers are 1.4. So what will be the multipliers tomorrow? A number of arguments can be made:

· Postponing adjustment increases debt levels. It is therefore possible that market interests will be higher in the future which will weigh on economic activity and increase multipliers because corporations will be credit-deprived.

· Postponing fiscal adjustment delays price adjustment and therefore reduces scope for corporations to export. Price adjustment has barely started and Italian inflation remains stubbornly above euro area average (Wolff 2013), even though inflation in Spain has come down.

· External debt levels remain very elevated for entire economies and public deficits don’t help reducing them.

· Increased interest rates call for frontloading fiscal adjustment in order to reduce overall fiscal burden. In turn, low interest rates speak in favor of later adjustment as fiscal costs are minor.

· Higher debt is associated with higher interest rates so that deficits together with debt rollover will lead to further increases in interest payments.

· Multipliers could also be lower in the future: The euro area is putting in place very significant institutional reforms that will also be beneficial for bank lending. In particular, the establishment of a banking union with the corresponding fiscal union will likely help reducing interest rates to corporations (Pisani-Ferry and Wolff 2012). Moreover, forceful bank resolution will reduce private debt burdens which will also reduce market pressure.

· Moreover, spreads could further come down if markets start believing even more in the ECB’s OMT. Or in other words, if current yields still have a significant panic component, then they may come down further.

Paul de Grauwe essentially dismisses the first arguments. In my reading of his post, he essentially claims that public debt does not matter for sovereign interest rates. He claims to prove this by showing that countries that had the largest increase in debt actually have had the largest decrease in spread in the last year. Now here I fundamentally disagree with Paul. There is no doubt that spreads have come down very substantially thanks to the ECB’s OMT announcement, a policy I fully support. But of course the spreads have come down most in the countries with the worst fundamentals, i.e. the highest debt and deficit levels. So ECB policy has helped significantly reduce market panic but that does not mean that fundamentals don’t matter. I show the simple correlation between debt and risk premia in my last paper (Wolff 2012) and there is also ample other empirical evidence that shows that yields also depend on fiscal fundamentals. Increasing debt levels thus does come with a cost and we should be acknowledging this.

Depending on your views about the future of the multiplier, different strategies should be adopted. In my view there is a significant probability that things will get worse and multipliers will increase but there is also a significant probability that things will get better thanks to the arguments above. I therefore content that the best strategy is to pursue a gradual fiscal adjustment, or essentially scenario 1. Scenario 1 balances the risk of a late adjustment under adverse circumstances with the potential benefits of a later adjustment when multipliers are lower. The basis of this view is thus the assumption that both scenarios 2 and 3 are possible. If we were sure that scenario 3 is impossible, it would clearly be preferable to delay adjustment to later when multipliers are lower. However, if we were sure that scenario 3 is the right one, then one should essentially frontload all the fiscal adjustment to the present.

If you follow me up to here, you will agree that gradual fiscal adjustment is desirable. Now it boils down to an empirical question, whether the fiscal adjustment that the euro area is undertaking is gradual or excessively high. De Grauwe seems to argue that it is very fast but I don’t understand what his metrics for coming to that conclusion is and his data sources are unclear. One simple way of looking at fiscal adjustment is the change in the budget balance, another one is the change in the structural balance. All these measures are very imperfect and you can debate about them. So it is a very difficult judgment call to be made. Below, I show a table with the structural and the headline deficit of Spain and Italy. I then compute the implied end year of adjustment if the speed of consolidation follows the one in 2012.

Table: Structural and headline budget balance and implied adjustment period

|

|

2010 |

2011 |

2012 |

Implied year of finished adjustment |

|

Spain structural deficit |

-7.4 |

-7.3 |

-5.9 |

2017q1 |

|

Spain headline deficit |

-9.7 |

-9.4 |

-10.2 |

Never |

|

Italy structural deficit |

-3.6 |

-3.7 |

-1.4 |

2013q3 |

|

Italy headline deficit |

-4.5 |

-3.9 |

-2.9 |

2015q4 |

For Spain, the data suggest that the adjustment will take roughly 5 years until the structural balance is zero in 2017. However, the headline number shows no adjustment – of course, there have been bank bail-outs. With a bit of faith, one can say that this is a one-off and should therefore not be counted. I conclude that adjustment in Spain is gradual. Turning to Italy, a different picture emerges. Structural adjustment has been very significant in 2012 and if the speed was to continue, Italy would reach structural balance in the second half of 2013. For the headline deficit number, the data suggest a completion of the adjustment by 2015. Arguably, Italy performed a front-loaded adjustment.

In sum, I conclude that the adjustment in Spain is pretty gradual while in Italy it was somewhat frontloaded but I do admit that the measurement problem of fiscal adjustment is significant. The European Commission as well as markets were of the view that Italy needed to re-establish its credibility through forceful action. The market panic was not sufficiently reduced by the ECB’s SMP programme despite it being heavily biased towards Italy and the institutions did want a strong front-loaded contribution by the national authorities as well. In both countries, the emphasis was on structural adjustment so as to provide a signal of credibility while at the same time having a smaller actual adjustment. Overall, the adjustment in Italy may have been a bit too quick while in Spain the speed seems roughly appropriate.

A second question is about the speed of fiscal adjustment in the three programme countries. Here I note that it is not markets that determine this speed but rather the political difficulty of Troika negotiations as well as the will to support adjustment with early debt restructuring and more forceful bank resolution involving bank creditors.

In my view, the above scenarios hold a much more important and different lesson. Balancing budgets is ultimately unavoidable in a monetary union, an insight already advanced by Bill Oates (1968). Yet, something is needed to offset the recessionary effects of the fiscal discipline. The eurozone’s South will likely have a significant recession for several years to come. I conclude that Europe’s South needs a Marshall plan to re-invigorate growth. Re-shaping of structural and cohesion funds could have been one way to generate growth in the South of Europe (Marzinotto 2011), but the last budget negotiations were a missed opportunity. One could also start a program linking fiscal support measures with binding contracts for reform. Such reforms continue to be vital in order for prices to adjust and linking them to significant payments would make them politically more acceptable. Moreover, in some cases public and/ or private debt levels may already be unsustainable calling for a robust use of restructuring and resolution tools. Overall, some form of fiscal union will be needed (Wolff 2012). This is what Paul de Grauwe and Paul Krugman should be calling for – not delaying fiscal adjustment hoping for dramatically lower multipliers in the future and risking the next financial crisis in the meantime.

References

De Grauwe, Paul and Yuemei Ji (2013), Panic driven austerity in the eurozone and its implications, VoxEU

Marzinotto, Benedicta (2011), A European fund for economic revival in crisis countries, Bruegel Policy Contribution 2011/01

Oates, Wallace (1968) ‘The Theory of Public Finance in a Federal System’, Canadian Journal of

Economics 1(1): 37-54

Pisani-Ferry and Wolff (2012), The fiscal implications of banking union, Bruegel Policy Brief 2012/02

Wolff, Guntram (2012), A budget for Europe’s monetary union, Bruegel Policy Contribution 2012/22

Wolff, Guntram (2013), What does the Big Mac say about euro area adjustment?, Bruegel blog 6 February 2013

About the authors

Related content

The European defence industrial strategy: important, but raising many questions

The European defence industrial strategy helps to focus thinking but has significant flaws

Use the financial system to enforce export controls on Russia

Use the financial system to enforce export controls on Russia

Prohibition of Western tech exports to Russia is not working; rapid measures are needed to tighten up