Blogs review: Bold ideas for the eurozone from economic history

What’s at stake: Bruegel has recently come under criticisms for not proposing bold enough ideas to reform the eurozone. In this review, I pr

What’s at stake: In this review, I present an eclectic set of proposals and analyses that have been put forward by economic historians to reform the functioning the eurozone in a big way. The first category of proposals discuss ways though which monetary policy could be differentiated across different countries within the monetary union. The second category of analyses challenges the now conventional view that a monetary union necessarily requires some form of fiscal, banking and/or political union.

Making monetary policy more flexible

Markus Brunnermeier writes that the ECB could optimize its currency area by using “regional tools” that affect the regional credit and term spreads. Unconventional monetary policy allows central banks to influence term and credit spreads directly by buying or selling long-term risky assets. But the ECB could also use its haircut policy to lean against regional imbalances. Using haircuts to lean against regional imbalances is in sharp contrast to the ECB’s current policy. Currently, the ECB uses collateral and haircut policy purely as a risk management tool, i.e., to minimize potential losses from lending against certain assets. Furthermore, there is a tendency to treat all member countries the same and avoid any differentiation. This makes all spreads more uniform across the membership countries – the opposite effect of what a targeted active policy that leans against regional imbalances would prescribe.

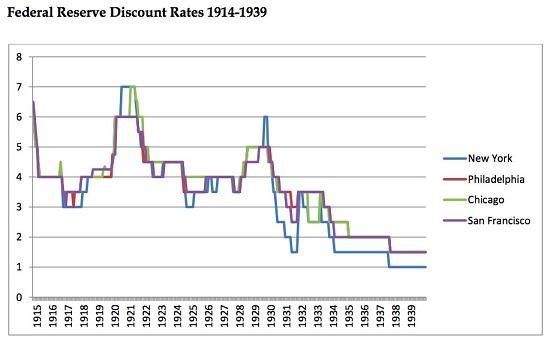

Harold James also argues that different interest rates in different countries might open the door to a more stable eurozone, but notes that different policy rates might even be possible. When the EC Committee of Central Bank Governors began to draft the ECB statute, it took the indivisibility and centralization of monetary policy as given. But it was not really justified either historically or in terms of economic fundamentals. The history of the gold standard, and of other large common-currency areas show that despite the theoretical possibility of capital being sent over vast distances to other parts of the world, much capital remained local, making the differentiation of interest rates possible. In the early history of the Federal Reserve System, individual Reserve Banks set their own discount rates. In smooth or normal times, the rates tended to converge. But in times of shocks, they could move apart. The Eurozone is now moving to a modern equivalent as bank collateral requirements are being differentiated in different areas. This represents a remarkable incipient innovation.

Source: Harold James

A common currency does not mean a single currency

Harold James notes that was one of the possibilities that was raised in the discussions on monetary union in the early 1990s was that there might be a common currency but not necessarily a single currency. Keeping the Euro for all members of the Eurozone but also allowing some of them (in principle all of them) to issue national currencies would be the modern equivalent to the band widening of 1993. The countries that do that would find that their new currencies immediately trading at what would probably be a heavy discount. California recently adopted a similar approach, issuing IOUs when faced by the impossibility of access to funding. Such a course would not require the redenomination of bank assets or liabilities, and hence would not be subject to the multiple legal challenges that a more radical alternative would encounter.

Harold James writes that such a state of affairs is not just a theoretical construct in fringe debates in the early 1990s, but a real historical alternative. There is in fact a rather surprising parallel for such a stable coexistence of two currencies over a surprisingly long period of time. Before the victory of the gold standard in the 1870s, Europe operated with a bimetallic standard for centuries, not only gold but also silver. One trick that made this regime so successful was that the coins were used for different purposes. High value gold coins were used as a reference for large value transactions and for international business. Low value silver coins were used for small day to day transactions, for the payment of modest wages and rents. A depreciation of silver relative to gold in this system would bring down real wages and improve competitiveness. In the modern setting, the equivalent of the adjustment mechanism in the early modern world of bimetallism would be a fall in Greek (or other crisis country) wage costs as the wages were paid in the national currency, as long as it was traded at a discount. These would be the equivalent of silver currencies. Meanwhile, the Euro would be the equivalent of the gold standard. It would be kept stable by the institutions which already exist today, the ECB and the ECSB of those national central banks who have no new alternative.

Hugh Rockoff argues that the case of the West in the 19th century suggests that dividing the Eurozone in two currency zones is possible. From the outbreak of the war until 1879 the West remained on the gold standard while the East was on the greenback standard. National banks in the West issued “goldbacks” redeemable in gold. The exchange rate between greenbacks and goldbacks fluctuated. A curiosum, but perhaps one that suggests that dividing the Eurozone in two currency zones is possible.

A monetary union without a fiscal/political union

Simon Wren-Lewis writes that the view that the Eurozone will have to move to fiscal union, which implies some form of political union, seems to be a very common view at the moment. Those working in the political unions that are the US or the UK, know combined monetary and fiscal unions can work. From this perspective, the monetary only union of the Eurozone was a largely untried experiment, and it appears to be failing. Within the Eurozone itself, there has always been a powerful lobby for further integration. It is therefore not surprising that actors like the Commission see further integration as the longer-term solution to the Eurozone’s problems.

Harold James writes that the idea that Europeans simply need a country because they happen to have a currency reflects a misunderstanding about the reasons politicians embarked on the economic and monetary union of Europe.

Simon Wren-Lewis writes that we should be very cautious about making generalizations from a single observation. The Eurozone has not been a fair test of monetary union without fiscal union since poor policies were also put in place at the same time. 1) No attempt was made to use fiscal policy to offset overheating in periphery countries. 2) Instead of recognizing the need for default early on, the union made a futile attempt to avoid it by replacing private debt with intergovernmental lending. 3) The fiscal position of Eurozone economies became critical because the ECB refused to act as a lender of last resort. 4) The current double dip recession in the Eurozone is largely about a collective failure of fiscal and monetary policy.

Benjamin Cohen writes that history suggests that political union is not necessary for the longevity of the euro area. In the modern era (19th century onward), there are at least seven notable examples – other than EMU – of formal monetary unions without political union: The Latin Monetary Union, the Scandinavian Monetary Union, the Belgium-Luxembourg Economic Union, the CFA Franc Zone, the East African Community, the East Caribbean Currency, and the West African Monetary Area. Two of the seven (CFA, ECCA) remain in existence to the present day; a third (BLEU) existed for 3/4 century until incorporated into the larger EMU; and two other (LMU, SMU) managed to survive for more than a half century until brought to an end by World War I.

Randall Henning writes that a couple of observations emerge from the history of the US fiscal rulemaking that seem especially relevant to the EU now.

1. Even though the debt brakes of the fiscal compact are introduced into national constitutions and framework laws, the process has been initiated by the center and in some cases under duress. In the United States, rules were adopted autonomously by the states. This has implications for domestic political “ownership”.

2. Community institutions play a leading role in enforcing the rules, whereas the U.S. federal government has no such role. In fact, the U.S. federal government in fact cannot legislate fiscal rules for the states; this would be an unconstitutional infringement on “state sovereignty.” The U.S. model of fiscal rectitude for the states rests on multiple layers of rules combined with the no bailout norm.

Germany: the missing hegemon

Benjamin Cohen writes that experience suggests that in the absence of political union, a local hegemony or solidarity are necessary to keep a monetary union functioning reasonably well; where both conditions are present, they are sufficient. The importance of a local hegemon was well demonstrated by BLEU (Belgium, twenty times the size of Luxembourg, called the shots). The importance of solidarity is evident in the longevity of SMU, BLEU, ECCA. All three involved groups of partners with a strong sense of common identity, grounded in a shared cultural and political background and institutionalized in a broad network of related economic and political agreements.

Brad DeLong writes that the Kindlebergian perspective would lead one to think that the problem of Europe today is that Germany does not want to assume the burden, or assume the role, or is not wanted by the rest of Europe to assume the explicit role on terms that Germany wishes to exercise it. Brad DeLong and Barry Eichengreen write the German Federal government has room for countercyclical fiscal policy. It could encourage the European Central Bank to make more active use of monetary policy. It could fund a Marshall Plan for Greece and signal a willingness to assume joint responsibility, along with its EU partners, for some fraction of their collective debt. But Germany still thinks of itself as the steward in a small open economy.