Blogs review: Understanding the mechanics and economics of Bitcoins

What’s at stake: The value of Bitcoins – the peer-to-peer currency – has been soaring so much of late that you have certainly heard about it. It is al

What’s at stake: The value of Bitcoins – the peer-to-peer currency – has been soaring so much of late that you have certainly heard about it. It is also likely that you still don’t fully understand how this decentralized payment mechanism works in practice as it is hard to build a bridge between the overly general and the overly complicated descriptions of the system. Here is our (imperfect) take at it based on what we have read so far. The monetary economics of it is fairly straightforward and uninteresting, but the mechanics of making payments over a communications channel without a trusted party is really interesting.

The recent popularity of Bitcoins

James Surowiecki writes when the virtual currency bitcoin was released, in January 2009, it appeared to be an interesting way for people to trade among themselves in a secure, low-cost, and private fashion. The Bitcoin network uses a decentralized peer-to-peer system to verify transactions, which meant that people could exchange goods and services electronically, and anonymously, without having to rely on third parties like banks. Its medium of exchange, the bitcoin, was an invented currency that people could earn—or, in Bitcoin’s jargon, “mine”—by lending their computers’ resources to service the needs of the Bitcoin network. Once in existence, bitcoins could also be bought and sold for dollars or other currencies on online exchanges.

Maria Bustillos writes that a number of businesses have recently begun accepting bitcoins in payment for their services. At bitcoinstore.com, you can buy electronics—including cameras, musical instruments, blood-pressure monitors, and computers—using just bitcoins. There are bitcoin-only casinos, like SatoshiBet, and a bitcoin-based Intrade-style prediction market called Bets of Bitcoin.

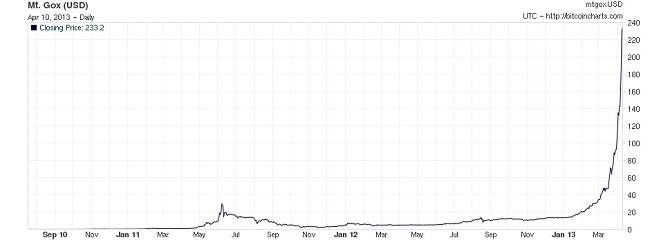

Yves Smith writes at Naked Capitalism that Bitcoins have been making headlines on mainstream news sites, on blogs and even on precious metal forums recently and with good reason given the vertical rise in price per Bitcoin.

Source: Bitcoin Charts

Felix Salmon writes that Bitcoin has become suddenly popular in Cyprus for obvious reasons: no government can confiscate your bitcoins, or prevent you from transporting them out of the country. Yves Smith notes that much of this speculation about the impact of Cyprus on the popularity of Bitcoins, however, boils down to an increase in app downloads in a single country where iPhones do not have a large market share. Alec Liu thinks that Bitcoin is rallying because of government-backed legitimacy thanks to the recent guidance from the anti-money laundering arm of the U.S. Treasury, FinCEN (see here). A number of authors think that it’s simply a bubble.

The rationale for an alternative currency

Satoshi Nakamoto – the pseudonymous person or group of people who designed and created the original Bitcoin software – writes that the root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency. Banks must be trusted to hold our money and transfer it electronically. We have to trust them with our privacy, trust them not to let identity thieves drain our accounts… With e-currency based on cryptographic proof, without the need to trust a third party middleman, money can be secure and transactions effortless.

Satoshi Nakamoto writes that the commerce on the Internet that relies on financial institutions works well for most transactions, but suffers from the inherent weaknesses of the trust based model. First, the cost of mediation increases transaction costs, limiting the minimum practical transaction size and cutting off the possibility for small casual transactions. Second, with the possibility of reversal of transactions, merchants must be wary of their customers, hassling them for more information than they would otherwise need.

Satoshi Nakamoto writes that the idea of a purely peer-to-peer version of electronic cash is to allow online payments to be sent directly from one party to another without going through a financial institution. Digital signatures provide part of the solution, but the main benefits are lost if a trusted third party is still required to prevent double-spending. To deal with the problem of double-spending, Nakamoto proposed a solution that uses a peer-to-peer network. The network timestamps transactions by hashing them into an ongoing chain of hash-based proof-of-work, forming a record that cannot be changed without redoing the proof-of-work.

Satoshi Nakamoto points that no mechanism existed, prior Bitcoins, to make payments over a communications channel without a trusted party. The idea of Bitcoin is to define an electronic coin as a chain of digital signatures. Each owner transfers the coin to the next by digitally signing a hash of the previous transaction and the public key of the next owner and adding these to the end of the coin. For the system to work, we need a way for the payee to know that the previous owners did not sign any earlier transactions. The only way to confirm the absence of a transaction is to be aware of all transactions. To accomplish this without a trusted party, transactions must be publicly announced, and we need a system for participants to agree on a single history of the order in which they were received.

The details of the Bitcoin network (very wonkish)

Felix Salmon writes that for the time being, Bitcoin is in many ways the best and cleanest payments mechanism the world has ever seen. So if we’re ever going to create something better (see next section on the economics of the system), we’re going to have to learn from what Bitcoin does right – as well as what it does wrong.

Nemo has the best understandable description of the technical aspects of the Bitcoin network in a series of posts on his blog Self-evident. He starts by noting that Bitcoin relies on extremely elementary cryptography.

Nemo writes that a central ingredient in the system is the use of one-way functions. A one-way function is a function that is easy to compute but hard to invert. The formal definition of “hard” is a little tricky, but the basic idea is that you either have to get very lucky or you have to take a very long time to invert them. Indeed, good one-way functions usually have the property that your best strategy for inverting them is to keep guessing values of x until you stumble across one with f(x) = y. Indeed, Bitcoin “miners” are currently doing precisely this fifty trillion times per second.

The key ingredient is actually a trapdoor one-way function, which is a function that is easy to compute but hard to invert… for everybody except the person who created it. The idea is that you create your own personal function g(x) that has a secret (called a private key), such that inverting g is easy if and only if you know the secret. You share the function — but not the secret — with the whole world. So now the whole world can compute the function, but only you can invert it. Every Bitcoin “address” represents a unique trapdoor one-way function.

Nemo gives a simple example illustrating how these functions can be used. Suppose you and I want to bet on a coin toss over the phone. Is it possible for two untrustworthy people, like you and me, to play this game fairly? By the power of the one-way function, it is! Here is how. First, we agree on a one-way function f. Then I flip a coin. If the coin lands “tails”, I pick a big even number. If it lands “heads”, I pick a big odd number. Call that number x. Then I compute y=f(x) and tell you y. Then you guess “heads” or “tails”. Then, finally, I reveal x. Since you cannot invert f(x), you have no idea whether x is even or odd at the time you make your guess. And since I cannot invert f either, you can check the x I revealed simply by confirming that f(x)=y. Thus we have flipped a coin over the phone fairly, even if both of us would rather cheat.

Izabella Kaminska writes on her personal blog that miners effectively make money from seigniorage in its very basic form.

Nemo explains how mining works. Miners are clients that attempt to create new valid blocks. A block is a record of some or all of the most recent Bitcoin transactions that have not yet been recorded in any prior blocks. They do this by putting some transactions in a candidate block, picking a nonsense word called a nonce, computing the hash of the resulting block, and repeating with different nonces until they find a block whose hash does not exceed a certain threshold called a target. The current target for the block chain is defined by a calculation, so any two clients looking at the block chain will calculate the same target. This calculation aims to adjust the target such that one block will be mined every ten minutes, no matter how much total computing power is devoted to mining. Then they broadcast that block to the network, thus appending it to the block chain that every client sees. The Bitcoin software's Prime Directive is: When faced with conflicting versions of the block chain, the one with the greatest total sum of work is the Truth.

Paul Bohm writes that to rig the vote an attacker would need to control more computational power than the honest nodes. To ensure it's more expensive for an attacker to purchase the computational power needed to attack the system, Bitcoin adds an incentive scheme. Users who contribute computational power get rewarded for their work. This computational process ("mining") is not wasteful at all, but an incredibly efficient way to make attacks economically unprofitable.

Nemo explains the structure of the financial incentive for miners: They can embed one coinbase transaction in each block they mine. The coinbase transaction includes new bitcoins (hence the term “mining”) and also any transaction fees associated with the transactions in the block.

The economics of Bitcoins

James Surowiecki writes that the problem with Bitcoins is that instead of being used as a currency, bitcoins are today mostly seen as (and traded as) an investment. The problem with having the Bitcoin economy dominated by speculators is that it gives people an incentive to hoard their bitcoins rather than spend them, which is the opposite of what you need people to do in order to make a currency successful. Zachary Seward reports that when researchers examined the bitcoin universe last year, they found that between 55% and 73% of bitcoins, depending on how you count, were being held in dormant accounts.

Paul Krugman writes that Bitcoin has created its own private gold standard world, in which the money supply is fixed rather than subject to increase via the printing press. Bitcoin, rather than fixing the value of the virtual currency in terms of those green pieces of paper, fixes the total quantity of cybercurrency instead, and lets its dollar value float. What that means is that if you measure prices in Bitcoins, they have plunged; the Bitcoin economy has in effect experienced massive deflation. The actual value of transactions in Bitcoins has fallen rather than rising. In effect, real gross Bitcoin product has fallen sharply.