10 years EU enlargement anniversary: Waltzing past Vienna

Since their accession to the European Union ten years ago, something extraordinary has been going on in Central European capitals. Measured in purchas

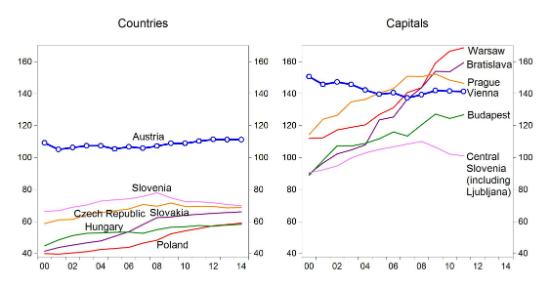

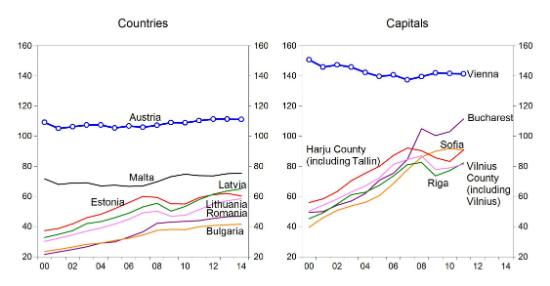

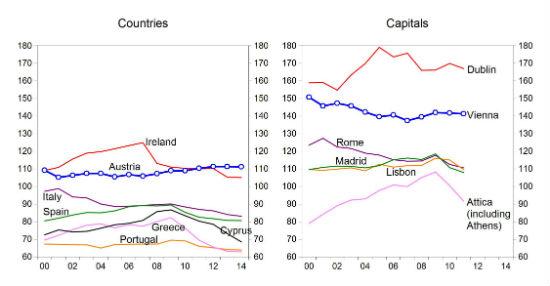

Since their accession to the European Union ten years ago, something extraordinary has has been going on in the central European capitals. Measured in purchasing power standards (PPS), Warsaw, Bratislava and Prague now have a higher GDP per capita than Vienna. The Österreichs Kaiserstadt has been the reference point for central European countries for centuries – and a reference point now too, due to geographical closeness and strong trade and financial links.

Budapest is also not far behind Vienna and the other anniversary members' capitals are closing the gap as well, except the Ljubljana region. This development is in sharp contrast to the relative positions of capitals in southern European countries, which have not converged to the average of the core EU countries during the past decade and have even diverged since 2009. Rome, Madrid and Lisbon now have a GDP per capita at PPS comparable to Bucharest and lower than in Warsaw, Bratislava, Prague and Budapest (Figure 1).

Quite right, GDP per capita is just one indicator of economic performance and in capital cities the share of corporate profits in GDP is often disproportionately high, leaving somewhat less to citizens. Vienna also used to rank in the top five of the world’s most liveable cities (based on indicators such as security, healthcare, culture, environment, education and infrastructure), while central European capitals have still to improve on this matter. Yet the rapid catching-up of central European capitals in terms of GDP is truly remarkable and should make it possible to improve other aspects of life in these cities.

Figure 1: GDP per inhabitant in purchasing power standards (EU core = 100), 2000-2014

Source: author’s calculations using Eurostat’s national accounts database and the IMF April 2014 World Economic Outlook (countries) and Eurostat’s GDP by NUTS 3 regions database (capitals).

Note: GDP per capita at purchasing power standards is typically compared to the average of the EU28. Instead of using this benchmark, which by definition includes converging central European countries and lagging-behind southern European countries too, we compared GDP per capita relative to the weighted average of ten core EU countries: Austria, Belgium, Denmark, Finland, France, Germany, Luxembourg, Netherlands, Sweden and United Kingdom (we use the same EU core country-average also in the right hand panels for assessing GDP/inhabitant in capitals). Country-data is available from Eurostat up to 2012: we chained IMF data for 2013-14 to Eurostat data. Regional data is available only up to 2011. No regional data is available for Cyprus and Malta and therefore these countries are not included in the panels showing capital city data.

While progressing at a slower pace than their capitals, the anniversary members' total economies have also generally converged towards the average of core EU countries since their accession, though there are some notable exceptions: Slovenia and Cyprus are now falling behind (largely due to their respective banking troubles) and the Czech Republic and Hungary have not converged much in recent years. These country-specific differences likely reflect the varying ability of individual anniversary members to exploit the opportunities offered by their EU membership.

In an econometric study covering both the pre-crisis period as well the crisis, I found that enlargement boosted annual country-wide GDP growth by about half a percent per year on average in the ten new central and eastern European members (see here). This is sizeable, even if this estimate is smaller than what some other studies have found. EU accession has offered a number of opportunities and improved economic growth prospects by a number of channels, such as:

- By adopting EU laws, market institutions have been strengthened, improving the business environment and attracting investments from abroad, which boosted the capital stock, productivity and improved corporate governance;

- Access to the single market increased competition, fostering efficiency of firms;

- As a result, several central European firms have become integrated into European and global value chains, benefiting both the manufacturing and the services sectors (see a nice report on Europe’s manufacturing);

- Access to education in other EU countries, along with labour mobility, allowed upgrading of skills, which had trickle-down effects on the domestic economy, even if many of those who left their country have not returned;

- Vast financial support from various EU funds boosted the development of infrastructure, education, research, healthcare, environment and subsidized agriculture, just to mention some main goals. While there are question marks about the efficiency of the use of EU funds (see e.g. a meta-analysis of cohesion policy), even if only some of the EU-funded spending have benign longer term effects, some effects are there.

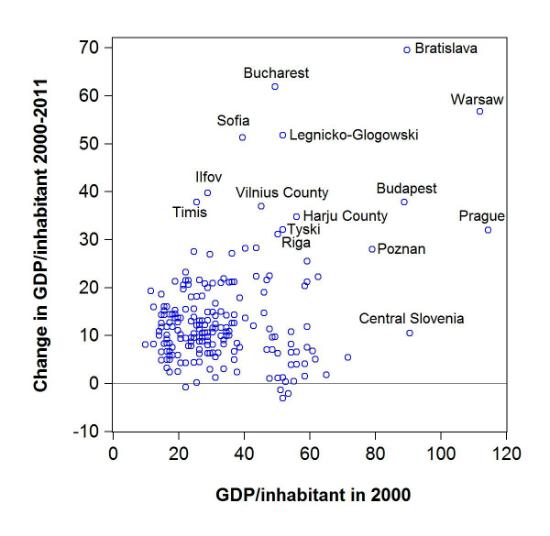

However, regional differences within countries widened. The rapid rise of the capitals and a few other regions characterised by an efficient concentration of economic activities was not mirrored in most other regions. A few regions did not converge to the average of core EU countries at all and several regions converged only little (Figure 2). In particular, regions that were poorer in 2000 have tended to converge less, contrary to the prediction of standard convergence theory. Such divergence raises major questions about the goals and efficiency of Europe’s cohesion policy as well as on the regional strategies of the anniversary EU member states.

Figure 2: GDP per inhabitant in purchasing power standards in 211 regions (EU core = 100), 2000 vs. the change between 2000-2011

Source: author’s calculations using Eurostat’s GDP by NUTS 3 regions database.

Note: the dots indicate 211 NUTS 3 regions of the central and eastern European countries that joined the EU in 2004/2007. See the definition of EU core in the note to Figure 1.

About the authors

Related content

European Union cohesion project characteristics and regional economic growth

A new approach, which estimates 'unexplained economic growth', provides insights into the types of European Union cohesion projects that produce bette

Cross-border, but not national, EU interregional development projects are associated with higher growth

Our calculations reveal that places where EU regional development projects bind together participants from different countries experience higher econo

The role of Cohesion policy in the fight against COVID-19 with Elisa Ferreira

How can cohesion funds help the National, regional and local communities that are on the frontline in countering the coronavirus and the resulting eco

Deep Focus: Making a success of EU cohesion policy

Bruegel senior fellow Zsolt Darvas talks to Sean Gibson in this Deep Focus podcast about how the EU can improve its cohesion policy, citing the best e