Addressing weak inflation: The ECB’s shopping list

In this blogpost, we summarize our recently published paper, in which we discuss in detail the dilemmas for the ECB and the need to act. Inflation for

See also policy contribution 'Adressing weak inflation: The European Central Bank's shopping list' and Ashoka Mody's comment 'The ECB must - and can - act

It was a mistake that the ECB did not act earlier. Conventional policy measures are unlikely to change inflation dynamics substantially. The ECB therefore needs to start buying assets. We propose to buy €35bn per months of a portfolio of ESM/EFSF/EU/EIB bonds, corporate bonds, and ASB. Buying international securities is not advisable as it would be against international commitments.

Inflation in the euro area has been falling since late 2011 and has been below 1% since October 2013. Core inflation, a measure that excludes volatile energy and food price developments has developed similarly. Low inflation in the euro area is particularly dangerous, given the high private and public debt levels in several euro-area countries and the need for relative price adjustment between the euro-area core and periphery.

Recent forecasts from the ECB revealed that average euro-area inflation is not expected to return to close to two percent in the medium term. The ECB’s commitments to its communicated objective of ‘below but close to two percent inflation in the medium term’ has therefore been undermined. At the same time, inflation expectations have also been falling since at least mid-2012 and, at the time-horizon relevant for the ECB, expectations have become disanchored.

In our view, it was a major mistake not to ease monetary conditions at the time the ECB’s own forecast signalled that inflation will not return to two percent in the medium term. To effectively address the risk of a persistently low inflation, the ECB should act and its action should be conducive to higher inflation, without undermining the major relative price adjustments necessary between the core and the periphery, nor the process of addressing weaknesses in the European banking system.

We are of the view that cutting ECB interest rates further and reducing the ECB’s deposit rate for banks below zero would help, but is unlikely to have a sizeable enough impact. Designing a new very long term (e.g. 3 years or longer) refinancing operation would not be very effective either, because liquidity conditions have normalized and banks have now a preference for paying back 3-year LTROs earlier. Stopping the sterilisation of the government bond holdings from the Securities Markets Programme (SMP) would be unwise, because that programme had a specific purpose with the stated feature of sterilisation. The best option for the ECB that has the potential to sizeably influence inflation and inflationary expectations is an asset purchase programme. Asset purchases can be motivated as a policy measure if interest rates reach the zero lower bound and refinancing operations do not promise to be effective. In a recent paper, we discuss the mechanisms and effects of different measures in detail.

Asset Purchases: Size and impact

Setting the appropriate size of asset purchases is far from easy. Some analysis considered the total amount asset purchases by the Bank of England and the Fed and suggested similar magnitudes for the euro area (20 to 25% of GDP, i.e. €1.9 to 2.4 trillion).

In our view, a more relevant benchmark is the amount of purchases by the Federal Reserve in its third round of quantitative easing (QE3), announced in light of the weak economic situation of the US economy at a time when the acute face of the financial crisis was over – a situation that has similarity to the current euro area situation. In September 2012, the Federal Reserve announced it would purchase $40 billion (€29 billion) agency mortgage-backed securities per month, an amount increased to $85 billion (€61 billion) in December 2012 (by adding $45 billion per month of Treasuries). Given that the euro area’s economy is about 30 percent smaller than the US economy, the same size, as a share of GDP, would be between €20 and €40bn per month in the euro area.

Asset Purchase: Design principles

In our view, the ECB will have to choose which assets to buy using five main criteria.

- the ECB should buy assets that lead to the most effective transmission on inflation.

- there should be sufficient amount of asset available, to ensure that the ECB can purchase appropriate quantities while not buying up whole markets.

- the ECB should try to minimize the impact on the private-sector allocation process. While QE by definition changes relative prices, the ECB should avoid buying in small markets distorting market pricing too much. The more the ECB becomes a player in a market, the more it can be subject to political and private sector pressures when it wants to reverse the purchases.

- the ECB should buy only on the secondary markets in order to allow the portfolio-rebalancing channel to work effectively. Purchasing on the primary market would imply the direct financing of entities, which should be avoided.

- the assets should only originate from the euro area and be denominated in euros, because of the February 2013 G7 agreement.

The Treaty gives a mandate to the ECB to maintain price stability, not to protect its balance sheet. Some criteria on riskiness should be adopted, but we recommend a reasonable low threshold for credit risk, such as restricting asset purchases only to the eligible collateral (without any additional eligibility criterion).

Asset Purchase: composition

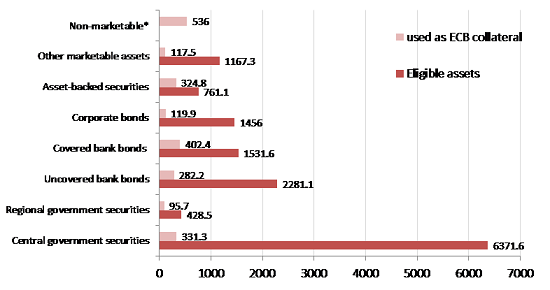

According to the ECB, total marketable assets eligible as collateral represented almost €14 trillion at the end of 2013, equivalent to 146 percent of euro-area GDP. About half of the Eurosystem’s eligible collateral pool at the end of 2013 consisted of government bonds, while the other half was split between uncovered bank bonds, covered bank bonds, corporate bonds, Asset Backed Securities and other marketable assets (which include the debts of EU rescue funds and the European Investment Bank).

A natural starting point for an ECB asset purchase programme would be euro-area wide government bonds, which do not exist. The closest proxy would be the bonds of European debt such as bonds issued by the European Financial Stability Facility (EFSF), the European Stability Mechanism (ESM), the European Union and the European Investment Bank (EIB). The total available euro-denominated pool of these bonds is around €490bn (230 for EFSF/ESM, 60 for EU, 200 for EIB). Buying such pan-European assets would not affect the relative yields of euro area sovereign debts and would not distort the market allocation process within the private sector.

Figure 1. Eligible assets and assets used as ECB collateral (EUR bns)

Source: ECB

Note: Eligible assets are in nominal values; assets used as ECB collateral are after haircuts and valuation issues. Latest data available: 2013 Q4

National sovereign debt would be a natural step as the bond market is very large and the positive effects of such a QE would be significant, via portfolio rebalancing, as well as the exchange rate, wealth and signalling channels. However, the purchase of national government debt is more complicated for the ECB as a supranational institution without a supranational Eurozone treasury as a counterpart than it has been for the Fed or the Bank of England. First, with 18 different sovereign debt markets, the ECB would have to decide, which sovereign debt to buy. The purchase would alter the spreads between countries and change the relative price of sovereign debts, which may expose the ECB to political pressure and lead to moral hazard. Second, the treaty prohibits the monetary financing of government debt, and since the goal of asset purchase will be to meet the ECB’s primary objective of price stability, purchase of government bonds would be allowed if the risk of monetary financing could be excluded. Experience proves that all ECB bond-buying programmes are controversial in this respect. Third, the ECB has a well-defined sovereign bond purchase programme, the so-called OMT, which is a tool to improve monetary policy transmission in countries under financial assistance. It is debatable whether a QE programme based on capital keys of the ECB would undermine the logic of the OMT programme, but this could be a risk and it should be avoided.

The second largest asset class is bank bonds, with €3.8 trillion available in eligible covered and uncovered bonds. Among the other effects, the reduction in market yields would also reduce the yields on newly issued bank bonds, thereby allowing banks to obtain non-ECB financing at a lower cost. This would improve bank profitability and may improve the willingness of banks to lend. However, bank bonds should be excluded from the ECB asset purchase programme until the ECB’s Comprehensive Assessment is concluded. Until then, ECB purchases would lead to serious conflicts of interest at the ECB and would make a proper assessment by the ECB more difficult. Moreover, those banks, for which the outcome of the Assessment will be unsatisfactory, should continue to be excluded from the ECB’s asset purchases until they have implemented all the required changes in their balance sheets. The latter may take several months after the completion of the Comprehensive Assessment.

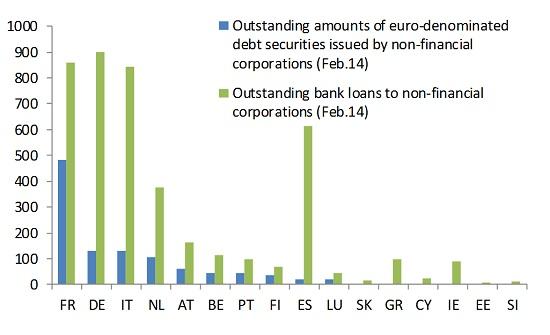

While there is no precise data on their magnitude, we estimate that the lower bound of eligible euro area corporate bonds would be €900 billion. In addition, the supply of corporate bonds in the euro area has been growing considerably since 2009. The euro area corporate bond market is highly concentrated (figure 3), with the main issuers of corporate bonds being French companies. However, for portfolio rebalancing to work, the origin of the corporate bonds is of less importance. The beneficial effect would come from the fact that the current owners of the corporate bonds would sell their bonds and use the cash for different purposes throughout the euro area. The purchases would encourage new issuance of corporate bonds everywhere and lead to a diversification of the sources of funding. Lower funding costs for corporations should induce more corporate investment.

Figure 2: Bonds vs. loans – financing of EU non-financial corporations (EUR bns)

Source: ECB

Note: The difference between the amount reported in this figure and the total eligible corporate bonds shown on Figure 2 comes from the fact that here we only consider corporate bonds issued by euro zone corporations, whereas eligible collateral include corporate bonds issued in the whole European Economic Area (EU countries and Iceland, Liechtenstein and Norway); see ECB

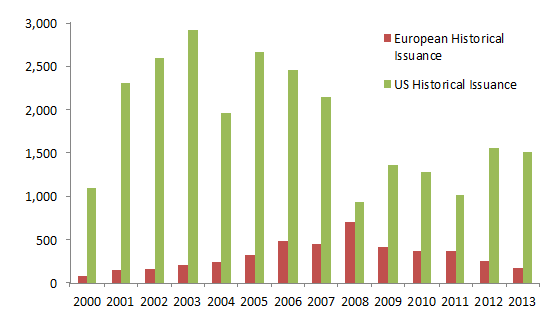

Another class of assets that could be bought by the ECB is asset backed securities (ABS). Yearly securitisation issuance – which peaked in 2008 – is much lower than in the US and has been decreasing since 2008. The total outstanding stock of securitised products has been stagnating at around €1.06 trillion for the Euro Area compared to €2.5 trillion in the US (AFME, 2014). Products eligible as collateral for the ECB amount to about €761 billion, but some of them originate from outside the euro area. We estimate that the lower bound of eligible euro area ABS would be €330 billion. It is worth highlighting that defaults on ABS in Europe have ranged between 0.6-1.5 percent on average, against 9.3-18.4 percent for US securitisations since the start of the 2007-08 financial crisis. The regulatory landscape for securitised products has also changed considerably since the crisis and made the products safer and more transparent.

Figure 3. European and US Historical Issuance of Securitised products (EUR bns)

Source: AFME - SIFMA

Considering the total amount of European ABSs, more than half (€612 billion) are based on residential mortgages, while SME ABSs constitute a smaller part (€116 billion). The ABS stock outstanding is unequally distributed across countries, with the main issuers being different from the main issuers of corporate bonds. ABS purchases would be concentrated on the Netherlands, Spain and Italy and could therefore be a good geographical complement to corporate bond purchases, which would be concentrated in France, Germany and Italy.

An ECB purchase could promote the development of securitisation in the euro area. The potential for securitisation is relevant, as many loans would qualify for securitisation ad in March 2014 the outstanding amount of loans to non-financial corporation stood at €4.2 trillion and to household at 5.2 trillion in the EU[4]. From a monetary policy perspective, it would be very beneficial to create ABS that are based on a portfolio of European assets. Ideally, the credit risk should be pooled at the level of the private sector, thereby deepening cross-border financial integration. However, the ECB should not wait for developments in the ABS market to start buying securitised products.

Table 1: Securitisation in Europe, outstanding stock in 2013Q4 (€ bns)

| ABS | CDO | CMBS | RMBS | SME | WBS | TOTAL | |

| Austria | 0,3 | 0,2 | 1,8 | 2,3 | |||

| Belgium | 0,1 | 0,2 | 63,3 | 17,8 | 81,4 | ||

| Finland | 0,6 | 0,5 | 1,1 | ||||

| France | 22,6 | 2,0 | 10,2 | 1,9 | 0,5 | 37,3 | |

| Germany | 35,8 | 2,2 | 10,6 | 15,3 | 5,9 | 0,1 | 69,9 |

| Greece | 14,3 | 1,8 | 4,3 | 7,2 | 27,6 | ||

| Ireland | 0,3 | 0,2 | 0,4 | 37,6 | 38,5 | ||

| Italy | 50,5 | 3,5 | 10,1 | 85,6 | 28,2 | 0,9 | 178,9 |

| Netherlands | 2,3 | 0,9 | 2,5 | 249,7 | 8,0 | 263,5 | |

| Portugal | 4,2 | 26,2 | 5,3 | 35,7 | |||

| Spain | 27,0 | 0,5 | 0,4 | 118,0 | 37,7 | 0,0 | 183,6 |

| PanEurope1 | 2,0 | 33,9 | 13,0 | 0,2 | 3,2 | 0,2 | 52,4 |

| Multinational2 | 0,9 | 81,1 | 1,8 | 0,4 | 0,8 | 84,9 | |

| Selected Euro Area Total | 160,9 | 123,9 | 41,2 | 612,3 | 115,8 | 3,0 | 1057,2 |

Source: AMFE (2014)

Note: All volumes in Euro. ABS: asset-backed securities for which collateral types include auto loans, credit cards, loans (consumer and student loans) and other. CDO: Collateralised Debt Obligations denominated in a European currency, regardless of country of collateral. CMBS: Commercial Mortgage Backed Securities. RMBS: Residential Mortgage Backed Securities. SME: Securities backed by Small- and Medium- sized Enterprises. WBS: Whole Business Securitisation: a securitisation in which the cash flows derive from the whole operating revenues generated by an entire business or segmented part of a larger business. 1. Collateral from multiple European countries is categorised under 'PanEurope' unless collateral is predominantly (over 90 percent) from one country. 2. Multinational includes all deals in which assets originate from a variety of jurisdictions. This includes the majority of euro-denominated CDOs.

Conclusions

We recommend that the ECB starts an open-ended programme of €35bn per month of asset purchases and reviews this number after 3 months to see whether its size needs to be changed. Using empirical estimates from the literature and our assessment, a €35bn per month purchase during a year could lift inflation by 0.8-1.0 percentage points.

In terms of available assets, we recommend the ECB to purchase privately issued debt securities, EFSF, ESM, EU and EIB bonds, but not government bonds, which could be problematic if there is a solvency risk of governments and would be politically controversial. The combined stock of EFSF/ESM/EU/EIB bonds suitable for purchases is €490bn. For private debt instruments we advise to consider the whole range of assets that are eligible as collateral at the ECB, without further credit rating requirements. Of these, the preference should be given to corporate bonds (for which we estimate that at least €900 billion are suitable for purchases) and Asset backed Securities (ABS, at least €330 billion suitable for purchases), while bank bonds of sound banks could be considered only after the ECB’s comprehensive assessment of the banking system is over. We therefore recommend that before the completion of the comprehensive assessment, the ECB starts monthly purchases of €15 billon of corporate bonds, €8 billon of ABS and €12 billion of EFSF/ESM/EU/EIB bonds.

Given the relative size of the purchases compared to the total size of the respective markets, the mispricing of risk would be limited and the ECB may not take on board much risk if a sufficiently diversified portfolio of assets is purchased.

We also highlight that the ECB’s Treaty-based primary mandate is maintaining price stability and there is no prohibition of monetary operations that exposes the ECB to potential losses and profits. However, it is also clear that the ECB should avoid to be exposed to unchecked political and private sector pressures that could result in delaying the reversal of asset purchases that would undermine the price stability mandate.

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

Use the financial system to enforce export controls on Russia

Use the financial system to enforce export controls on Russia

Prohibition of Western tech exports to Russia is not working; rapid measures are needed to tighten up