The ECB must - and can - act

If market perceptions again turn adverse, and the ECB is called on to do “whatever it takes” through its Outright Monetary Transactions program, the m

See also Zsolt Darvas, Grégory Claeys, Silvia Merler and Guntram B. Wolff comment and policy contribution 'Addressing weak inflation: The ECB’s Shopping List'

By coyly debating the definition and likelihood of deflation, while hoping for a renewal of inflation, the ECB is ignoring increasing risks, especially the growing cracks in the Italian fault line. Throughout the crisis, the ECB has been slow to act, failing to provide monetary stimulus to the weakening eurozone economies even as the member governments of the euro area undertook large fiscal consolidation and households and businesses deleveraged, further dampening demand. The apparent tranquility of the eurozone economies could well prove to be a temporary calm. There is a simple solution, as suggested by Harvard Professor Jeffrey Frankel: the ECB must undertake a long-delayed Quantitative Easing (QE) Program by buying US Treasuries. This will require coordination with the US and other G7 authorities not just because the norms require it but because the action is in the global interest.

Monetary Policy: Federal Reserve and the ECB

Those who bet on inflation expect that, a year from now, the annual inflation rate in the United States will be about 2 percent. In the euro area, the expected inflation rate is about 1 percent. But despite its much weaker inflation outlook, the eurozone monetary policy is much tighter, and has been so since mid-2008.

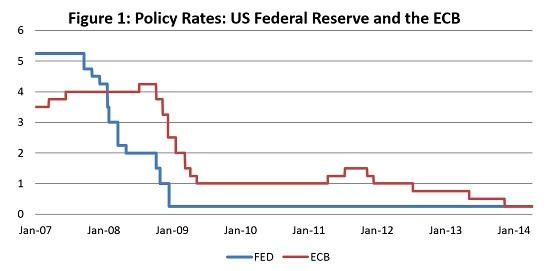

In January 2008, the policy rates were 4 percent in both the US and the euro area (Figure 1). Alan Blinder (2013) is critical of the Federal Reserve for having kept rates so high for so long after the start of the subprime crisis in the second half of 2007. Over the next year, however, the Federal Reserve moved at blazing speed, lowering the discount rate rapidly to 0.25 percent. Over that year, the ECB brought its rate down to 2.5 percent, having raised it once in between. Thereafter, the ECB’s policy rate continued to decline only slowly—with upward moves in April and July 2011 when the euro area economy was about to fall into another swoon, exerting a sizeable drag on the global economy. The ECB policy rate reached 0.25 percent in November 2013, five years after the US Federal Reserve had reached that milestone.

Sources: Federal Reserve Bank of New York, "Federal Funds Data Historical Search." European Central Bank, History of all ECB open market operations, "Main Refinancing Operations."

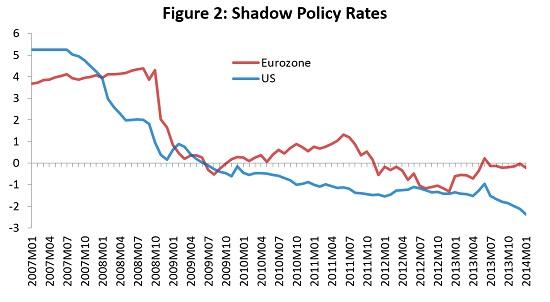

After its policy rate virtually touched the zero lower bound in December 2008, the Federal Reserve immediately began its QE via large-scale asset purchases. Researchers Cynthia Wu and Fan Xia find that by July 2009, the QE had depressed the effective policy rate into negative territory (Figure 2). This so-called shadow rate—estimated using a method proposed by Fischer Black in 1995—is derived from forward rates, the rates that investors expect in the future. Through successive QEs, the US shadow rate has steadily fallen and at the end of January 2014, it stood at -2.3 percent (and has fallen further since then to -2.6 percent).

Source: Xia, Fan Dora, University of California, San Diego, Economics.

The ECB also increased its assets, but in a very different context. Markets were increasingly unwilling to fund the operations of euro area banks, who then turned to the ECB for support. The consequent increase in the ECB’s balance sheet was, however, a way for banks in creditor countries to lend to banks in the debtor economies with the ECB interface effectively protecting the creditors from default risk. While this support was essential to prevent a meltdown of banks in the debtor economies, it did not have a stimulative effect.

Persistent Low Inflation in the Periphery

At end-January 2014 (the latest date reported), the shadow ECB policy rate was about -0.3 percent, about 2 percentage points above the US rate. The gap is even larger for the “real” shadow rate, which is about -4.5 percent in the United States and about -1.5% in the euro area, a difference of 3 percentage points. Thus, the US economy has, and continues to, benefit from much greater monetary stimulus.

More important, large differences exist in inflation rates across countries in the euro area; in comparison, differences across regions in the US are small. Hence, countries in the euro periphery, with significantly below-euro-area inflation rates, have much higher shadow real interest rates, in the range of 0.5 to -0.5 percent. Thus, the countries that need the most economic stimulus are getting the least. These are also the countries that are committed to a number of years of fiscal consolidation and private deleveraging.

This creates the risk of a Walters-style deepening divergence across the euro area. In 1986, Alan Walters had raised the concern that the wide inflation differentials within the euro area would tend to be naturally amplified. Given the same short-term nominal interest rate across countries, during boom periods, a rise in inflation in a country would lower its real interest rate, which would increase demand, push up inflation, and further reduce the real interest rate. Before the onset of the crisis, that process worked to maintain significantly lower interest rates in, for example, Spain than in German.

Now the process is working in the reverse. The relatively tight monetary policy creates the highest real interest rates in the periphery, which causes more downward pressure on prices in those countries, and hence the risk of persistently low inflation. This dynamic is a particularly severe liability in the context of private and public deleveraging.

The risks are serious to the euro area and to the world economy. The ECB has talked now for some months of doing QE. It has apparently waited in the expectation that the decline in inflation rates will be reversed without any policy action. Indeed, it would appear that the ECB is hopeful that the mere talk of QE will induce higher inflation. In the meantime, since it faces limits on the range of assets it can purchase, determining the most effective way of doing QE has also contributed to the delays.

The International Consequences of QE

The key to breaking this deadlock is turning the focus on the international implications of the US QE. Studies by the staff of the US Federal Reserve system show that QE significantly weakened the US dollar (Glick and Leduc, 2013 and Rosa and Tambalotti, 2014). These so-called event studies focus on a short time window around the QE announcement and find that the depreciation was significant; when the size of the QE is calibrated to an effective lowering of the policy rate, the quantitative consequences are surprisingly similar. Event studies are intended to identify causality—they help isolate the effect of the policy announcement from other influences. However, the effects of the QE have lasted well beyond the announcement.

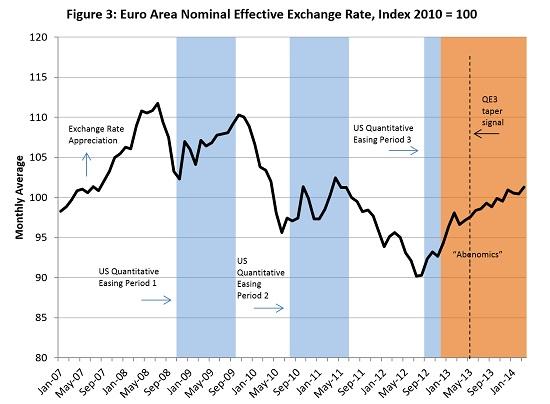

Early pressure from US QE was on both the yen and the euro. But with Japanese QE, so-called Abenomics in December 2012, the yen depreciated quickly.

The shaded areas in Figure 3 show that during periods of US QE and, more recently, of Abenomics, either the euro’s fall has been stopped or its effective exchange rate has appreciated. The only major currency without QE is euro. Hence, it has continued to face upward pressure, despite the eurozone’s weak growth potential. To reiterate, the problem is especially acute in the periphery where growth potential is particularly hobbled by the legacy of the crisis or, as in Italy, by weak long-term growth potential.

Notes: *QE1 began November 25 2008, with tapering announced on September 23, 2009. *QE2 occurred from August 10 2010, to June 30, 2011. *QE3 began September 13 2012, and has continued to the present. Tapering was announced by Chairman Ben Bernanke on May 22, 2013. *"Abenomics" began December 2012, and has continued to the present.

Sources: Bank for International Settlements, Effective exchange rate indices, Narrow indices, Nominal. | Board of Governors of the Federal Reserve System, Press Releases: Nov 25th 2008, September 23rd 2009, August 10th 2010, June 22nd 2011, September 13th 2012. | Bernanke, Ben. 2013. "The Economic Outlook." Testimony before the Joint Economic Committee, U.S. Congress, Washington, DC, May 22. | Abe, Shinzo. 2013. "Press Conference by Prime Minister Shinzo Abe." Prime Minister of Japan and His Cabinet, January 4.

Euro Area QE through Purchase of US Treasuries

The analysis, therefore, leads to a simple solution. Professor Frankel recommends that the ECB should stop fretting about its limited options and start buying American securities. This will have the effect of weakening the euro. In a world of slow international trade growth, the only way for Italy—and the rest of the European periphery—to jump start growth is through a much weaker euro. A depreciated euro will also help raise inflation and reduce the real debt burden.

Such action will be seen as violating G7 norms, which frown upon measures that deliberately move exchange rates. Competitive devaluations and currency wars are real concerns. The US and Japanese QE have been legitimized by their focus on domestic growth objectives. But the evidence is clear: while not targeted to depreciating their exchange rates, they have had the effect of doing so. Thus, as the ECB has stood by, the euro has been strengthened, leaving the euro area with some of the most fragile economies among so-called “advanced” countries.

The world has an interest in helping the euro area regain the ground that it has lost. The eurozone’s problems in 2011 and 2012 dragged world trade down and imposed a large cost on the world. If the Italian fault line were to fracture, the international consequences could be far reaching. With the ECB seemingly at the limits of its conventional possibilities, the option of QE through the purchase of US Treasuries should be undertaken in a coordinated and collaborative manner.

To not act now would be irresponsible. With public debt at nearly 135 percent of GDP, Italy faces the prospect of nominal GDP growth of 2 percent or less. The IMF’s projections suggest that at that rate, Italy will need primary surpluses of about 5 percent of GDP for a number of years. The political capacity to deliver those surpluses is, at best, questionable according to the IMF’s own research (Ostry et al., 2010). Italy desperately needs growth and inflation—and it cannot achieve them on its own. Rather than doing “whatever it takes” after the fact, the ECB can act now.

The current strategy of “internal devaluation,” lowering of wages does not work: it increases the risk of deflation with no certainty of whether (or when) growth will resume. And it raises the risk of political disruption.

Is it Too Late?

The ECB may already have waited too late. Even if it were to finally act, its past delays may render its actions and resolve questionable (Odendhal, 2014). If market perceptions again turn adverse, and the ECB is called on to do “whatever it takes” through its Outright Monetary Transactions program, the market may ruthlessly test that commitment—not least because of the legal and political uncertainties underpinning the promise. For this reason, coordination among the key central banks is all the more important. There is too much at stake.

***

References

Black, Fischer, 1995, “Interest Rates as Options,” Journal of Finance, 50(5): 1371-1376.

Blinder, Alan, 2013, “After the Music Stopped,” London: Penguin.

Frankel, Jeffrey, 2014, “Why the ECB Should Buy American, Project Syndicate, March 13. http://www.project-syndicate.org/commentary/jeffrey-frankel-urges-the-ecb-to-buy-us-treasuries-to-expand-the-monetary-base.

Glick, Reuven and Sylvain Leduc, 2013, “The Effects of Unconventional and Conventional U.S. Monetary Policy on the Dollar,” Economic Research Department, Federal Reserve Bank of San Francisco.

Ostry, Jonathan D., Atish R. Ghosh, Jun I. Kim, Mahvash S. Qureshi, 2010, “Fiscal Space,” IMF Staff Position Note, SPN/10/11.

Odendahl, Christian, 2014, “Quantitative easing alone will not do the trick,” http://www.cer.org.uk/insights/quantitative-easing-alone-will-not-do-trick#sthash.YWU9YtaD.dpuf

Rosa, Carlo and Andrea Tambalotti, 2014, “How Unconventional Are Large-Scale Asset Purchases?” Liberty Street Economics, http://libertystreeteconomics.newyorkfed.org/2014/03/how-unconventional-are-large-scale-asset-purchases.html#.U1_YTPldVDC.

Walters, Alan, 1986, “Britain’s Economic Renaissance,” Oxford: Oxford University Press.

Wu, Jing Cynthia and Fan Dora Xia, 2014, Measuring the Macroeconomic Impact of Monetary Policy at the Zero Lower Bound,” University of Chicago and University of California at San Diego, http://econweb.ucsd.edu/~faxia/pdfs/JMP.pdf.

I am grateful to Ajai Chopra, Barry Eichengreen, Jeffrey Frankel, and Guntram Wolff for comments and to Arvind Ramesh for very helpful research assistance.