The (not so) Unconventional Monetary Policy of the European Central Bank since 2008

This paper was prepared for the European Parliament's Montary Dialogue with the President of the European Central Bank Mario Draghi. Today, the ECB i

This paper is one in a series of nine documents prepared by Policy Department A for the Monetary Dialogue discussions in the Economic and Monetary Affairs Committee (ECON) of the European Parliament.

Abstract

The global financial and economic crisis forced major central banks to act swiftly and to innovate to avoid a free fall of their economies. This paper reviews in depth the measures adopted by the European Central Bank, and compares them with the ones adopted by the Federal Reserve and the Bank of England since 2008. The ECB has been very active since the beginning of the crisis and its actions helped the financial sector to avoid a complete meltdown. However, the ECB adopted measures that were mainly directed at ensuring the provision of liquidity and repairing the bank-lending channel, through changes to its usual framework for the implementation of monetary policy. By contrast, the Fed and the Bank of England quickly pursued unconventional monetary policies by implementing quantitative easing programmes that appeared to have a positive impact on financial variables and also on the real economy. Today, the ECB is confronted by inflation well below 2% and has reacted by implementing a broad package of fairly conventional measures. This analytical note pleads for the ECB to implement a large-scale asset-purchase programme and makes recommendations about the design of such a programme.

EXECUTIVE SUMMARY

- The global financial and economic crisis that started in 2008 forced major central banks around the globe to act swiftly and to innovate in order to avoid a complete meltdown of the financial sector, and to limit the consequences for the real economy.

- The ECB’s policy response to the crisis was mainly oriented towards ensuring the provision of liquidity and repairing the bank-lending channel. In order to do that, the ECB mainly modified its existing monetary policy tools. It increased the average maturity of its refinancing operations from months to years. It eased the collateral requirements to access those refinancing operations, and liquidity was allocated at a fixed rate and full-allotment basis. Retrospectively, those measures appear to have been a very appropriate and effective way to deal with the liquidity crisis of 2008-2012.

- The ECB also introduced more unconventional measures with the Securities Market Programme and the Covered Bonds Purchase Programme, which it used to buy particular assets – government bonds from troubled countries and covered bank bonds – in order to repair the monetary transmission channel in the euro area. However, the scope and impact of those measures was limited and short-lived. The ECB also announced the Outright Monetary Transactions programme, in order to purchase unlimited amounts of government bonds of member states subject to a European Stability Mechanism (ESM) programme. This measure has not been used, but its announcement had a significant impact on government bond yields of the EMU member states because it demonstrated the determination of the ECB to maintain the integrity of the euro area.

- The Federal Reserve (Fed) and the Bank of England chose a more radical and unconventional path in terms of monetary policy when they decided very quickly to implement large-scale asset-purchases programmes as their main response to the crisis. The sizes of these programmes were very significant (grossly equivalent to 20-25% of GDP) and, although it is very difficult to estimate their impact, there is a broad consensus in the literature that those measures had a positive impact on financial variables and also on GDP and inflation in the US and the UK.

- The liquidity crises that have plagued the euro area in the last few years seem to be behind us. The ECB’s main problem now is the continuous decline of inflation in the euro area to a level well below its definition of price stability of close but below 2%. In order to counteract this fall and to bring inflation back to 2% in the medium term, the ECB announced a broad package of measures at its June 2014 Governing Council meeting. However, although we welcome the fact that the ECB finally recognised that inflation will be too low for a too-long period and decided to act, we believe that the measures it proposes arrive too late, are too limited, and might be too “conventional” to solve the current problem. That is why we urge the ECB to implement a large-scale asset-purchase programme as soon as possible. To do that, we propose monthly purchases of €35bn of ESM/EFSF/EIB bonds, corporate bonds and asset-backed securities (ABS) in order to anchor inflation expectations and bring euro-area inflation back to 2% in the medium-term.

Introduction

Since 2008, the central banks of the main advanced economies have been very active in order to avoid the complete meltdown of their financial sectors and limit the adverse consequences for the real economy. However, central banks around the globe chose different paths to take action. The main aim of this paper is to compare these different paths since the beginning of the crisis and to assess the impact of those policies. Another goal of this paper is to determine what kind of unconventional policies the ECB should adopt today in order to fulfil its price stability mandate for the euro area.

In the first section of the paper, we will see that the ECB has mainly preferred to adapt its usual monetary policy framework to ensure the provision of liquidity to the banking sector and to repair the bank-lending channel to try to revive credit in the euro area, rather than to implement a more radical monetary policy. In the meantime, the Fed and the Bank of England embarked quickly on unconventional monetary policies by implementing quantitative easing programmes that seemed to have a positive impact on financial variables but also on the real economy through various channels.

The second section of this briefing paper essentially summarizes and updates the analysis and recommendations of Claeys et al (2014a and 2014b). It describes the main challenge faced by the ECB today, i.e. the current downward trend in inflation. During its June 2014 Governing Council, the ECB decided to react to this dangerous situation by implementing a broad package of measures. We will try to assess if these measures are enough to bring inflation back to 2% in the medium term, and we will see what kind of unconventional monetary policy could be implemented to achieve price stability in the medium term in the euro area.

1. Unconventional measures implemented by the ECB, the Fed and the Bank of England since 2008

1.1. ECB 2008-2013: saving the banking system, solving the liquidity crises

The ECB’s policy response to the crisis was mainly oriented towards ensuring the provision of the liquidity needed by the banking sector at a point at which the interbank market and other sources of short-term funding were almost frozen.

1.1.1 Modifications to the ECB’s refinancing operations

Together with the lowering of the policy rate from 4.25% to 1% between October 2008 and May 2009 (and later down to 0.15% from December 2011 to June 2014), the ECB introduced a number of measures to provide “enhanced credit support” to the economy.

Liquidity started to be allocated, through main refinancing operations (MRO) and long-term refinancing operations (LTRO), at a fixed rate and full-allotment basis, meaning de facto that banks had unlimited access to central bank liquidity, on the basis of the provision of adequate collateral.

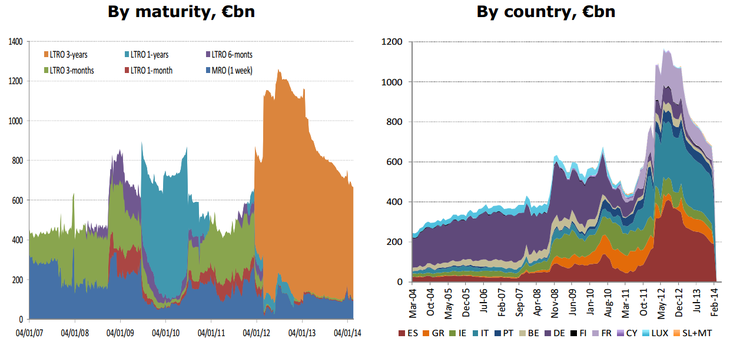

Collateral requirements were in turn eased a number of times, and on top of that, the maturity of LTROs – originally of 3 months only – was lengthened, introducing operations with maturity of, first, 6 months, then 1 year and eventually by conducting two massive very long-term refinancing operations (VLTROs) with a maturity of 3 years (in December 2011 and February 2012). The cumulative take-up of these two operations exceeded €1 trillion (although part of it substituted the borrowing through other maturities). As a consequence, the maturity of the ECB’s balance sheet has lengthened. Figure 1 shows that about 80% of all the liquidity provided to the banks – which constitutes the biggest component on the asset side of the Eurosystem’s consolidated balance sheet – has now a maturity of 3 years.

Not surprisingly, the use of the LTRO facility has been skewed towards certain countries, with banks in Spain, Italy, Greece, Ireland and Portugal accounting for 70 to 80% of the total borrowing since 2010. Symmetrically, banks from the North – which had benefited from inflows of capital in search of safety – reduced their reliance on the ECB operations to minimum levels. The VLTROs was constructed as a euro area-wide policy – i.e. open and directed to all banks in the euro area, but banks from the South of the euro area ended up using it more than the others because they were the most affected by the liquidity crisis taking place at the time in the European banking sector.

Figure 1: Eurosystem refinancing operations

Source: ECB

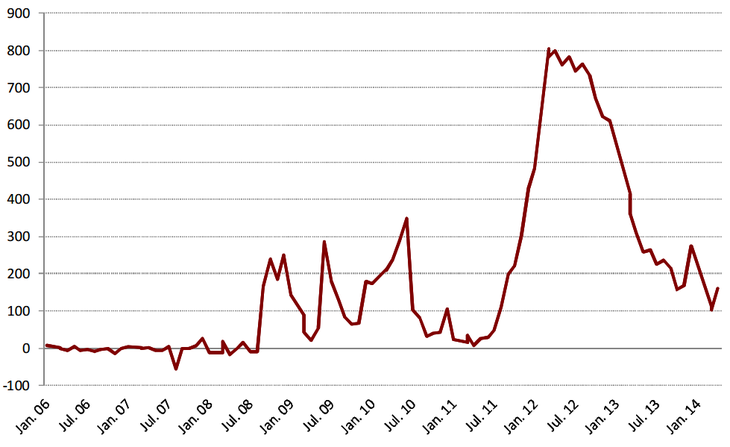

Since January 2013, the ECB has allowed banks to repay the funds borrowed under the three-year LTRO, earlier than on maturity date. Banks have been using this opportunity quite sensibly, especially in Spain, where the reliance on the Eurosystem facility was previously the largest. As a consequence of frontloaded reimbursements, the amount of liquidity in the euro area has started to fall rapidly. Figure 2 shows that the excess liquidity in the euro area[1] has dropped significantly since the beginning of 2013 and is now almost completely re-absorbed.

Figure 2: Excess liquidity – euro area, in €bn

Source: ECB

The empirical literature analysing LTROs suggest that those operations were very useful in improving monetary conditions at the height of the crisis[2]. While LTROs were a very appropriate and effective measure to deal with the liquidity crisis of 2011-12, these operations did little to trigger additional lending to the private sector (even though they might have helped to prevent the collapse of existing lending). To a great extent, banks either deposited the cheap central bank funding at the ECB for rainy days, or purchased higher yielding government bonds. Thereby, the LTROs in effect supported liquidity, ensured stable long-term (three-year) financing of banks, subsidised the banking system and helped to restore its profitability, and temporarily supported distressed government bond markets. Considering the alternative of a potentially escalating financial crisis, these developments were beneficial.

1.1.2 The Securities Market Programme (SMP), Outright Monetary Transactions (OMT) and the Covered Bonds Purchase Programme (CBPP)

Under the SMP, initiated in May 2010, the ECB bought around €220 billion of Greek, Irish, Portuguese, Italian and Spanish government bonds. At the time, the ECB announced that the bonds would be held to maturity and that the purchases are entirely sterilised. The intervention was justified in light of the severe tensions in certain market segments that were hampering the transmission of the ECB’s monetary policy. At present there are €175.5bn of SMP bonds left, the maturities of which are not publicly disclosed by the ECB. The empirical literature[3] has tried to assess the impact of SMP and concludes that it had a positive but short-lived effect on market functioning by reducing liquidity premia and reducing the level as well as the volatility of European government bond yields.

However, the programme was stopped in September 2012, when the ECB introduced the new Outright Monetary Transactions (OMT), the announcement of which had a remarkable effect on European bond yields even without the programme having ever been used. The programme allows the ECB to purchase essentially unlimited amounts of government bonds of member states that are already subject to a European Stability Mechanism (ESM) programme, as long as the member states in question respect the conditions of the ESM programme. The ECB contends that this policy could be necessary on monetary policy grounds, namely to safeguard “an appropriate monetary policy transmission and the singleness of the monetary policy”[4].

The ECB also introduced in 2009 a Covered Bonds Purchase Programme (CBPP), which was not sterilised and aimed at reviving the covered bond market, which plays an important role for the financing of banks. The ECB initially bought covered securities such as Pfandbriefe worth an aggregate volume of €60 billion within a one-year period. In November 2011, the ECB launched a second CBPP with a total volume of €40 billion, but it decided to interrupt it in October 2012, after covered bonds totalling €16.4 billion had been purchased.

1.1.3 Introduction of a Forward Guidance strategy

In July 2013, the ECB formally introduced forward guidance as a new monetary policy tool when President Draghi announced during the introductory statement of the press conference that “the Governing Council expects the key ECB interest rates to remain at present or lower levels for an extended period of time”[5].

Initially, the main idea behind forward guidance, introduced by Krugman (1998) when analysing the deflation and liquidity trap problem of Japan in the 1990s, was that central banks could gain traction on the economy at the zero lower bound if they manage to convince the public that they will pursue a more inflationary policy than previously expected after the economy recovers, what Krugman calls a “credible promise to be irresponsible”. This policy should indeed result in low short-term rates for an extended period of time and an increase in inflation expectations, which should both have a negative effect on real long-term rates today and should therefore boost investment and consumption.

However, the main problem of forward guidance is time-inconsistency. Central bankers do not want to commit themselves to future policy decisions and they will always have an incentive to raise rates when inflation returns to preserve their credibility to fulfil their price stability mandate. But if forward guidance is not time consistent, it is not credible and agents anticipate that rates will be raised earlier and it will therefore not be effective. To be credible it is possible that forward guidance needs a commitment or a time-consistency device to work better, a role that a massive asset purchase programme could play, given the potential delays resulting from a gradual and ordered exit strategy (as demonstrated by the current slow US QE tapering process).

Contrarily to what was advocated in the theoretical academic literature, the ECB clarified[6] quickly its forward guidance strategy by saying that it did not promise either “irresponsibility” or a suspension – even temporarily – of its usual strategy. The ECB considers only forward guidance as a new way to communicate its strategy in order to better anchor expectations about the future path of interest rates, and not at all as a commitment to keep rates lower longer than necessary in order to have a more significant immediate impact of monetary policy. This may have therefore reduced the effectiveness of the measure.

1.2. Unconventional measures adopted by the FED and the BoE: the quantitative easing experience

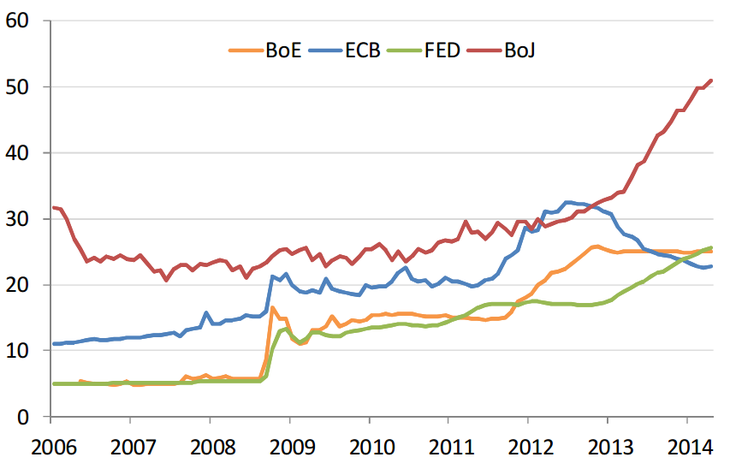

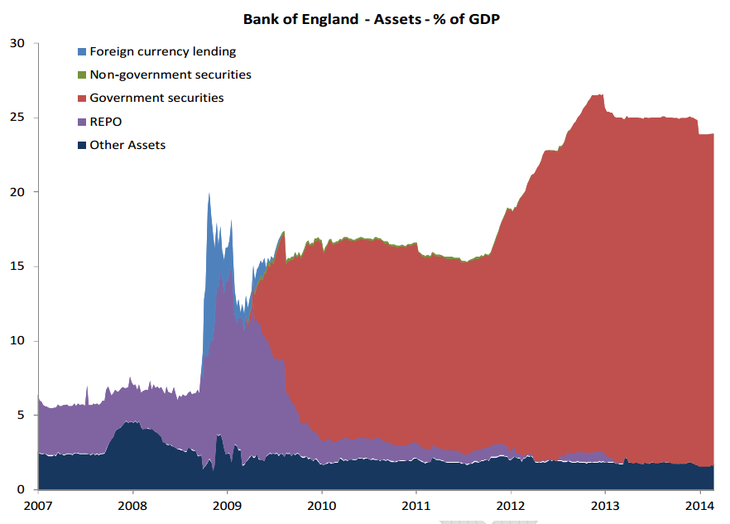

In response to the global financial and economic crisis, the Federal Reserve (Fed) and the Bank of England engaged in large-scale asset purchase programmes, or quantitative easing (QE)[7]. From the beginning of 2009 to March 2014, the Federal Reserve purchased $1.9 trillion (11.9 percent of US GDP) of US long-term Treasury bonds and $1.6 trillion (9.6 percent of US GDP) of mortgage-backed securities. Between January 2009 and November 2012, the Bank of England purchased £375 billion (24 percent of GDP) of mostly medium- and long-term government bonds. In addition to such asset purchases, these central banks also implemented programmes to support liquidity in various markets. All those measures resulted in a significant expansion of the central banks’ balance sheets (see Figure 3). Unlike the two other major central banks, the ECB has made few asset purchases so far but reacted to the crisis by providing liquidity to the banking system as we have seen before.

Figure 3: Size of balance sheets of various central banks, in % of GDP

Source: FRED, IMF.

1.2.1 Unconventional monetary policy in the US

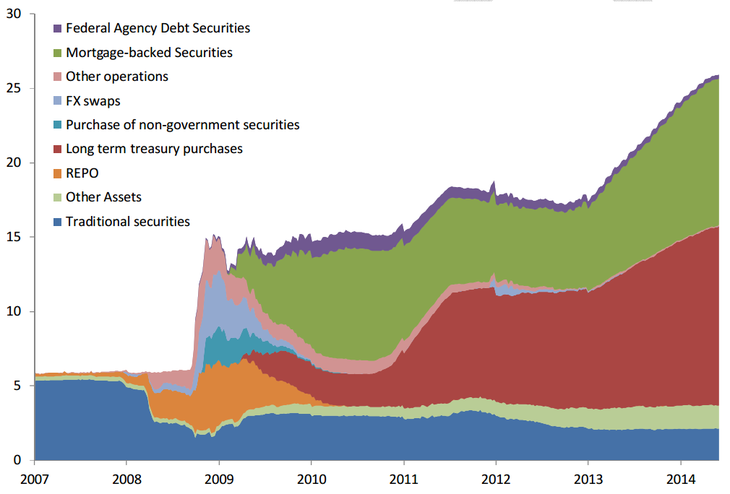

In the US, quantitative easing (QE) began immediately in November 2008 and is on-going. In total, it has expanded its balance sheet from $860 billion at the beginning of 2007 to $4.2 trillion today. The Fed announced in December 2013 a ‘tapering’ of its programme, and has reduced gradually its monthly purchases from $85 billion to $35 billion.

On top of its QE policy the Fed also introduced some short-term liquidity measures, such as the Commercial Paper Funding Facility, which purchased 3-month unsecured and asset-backed commercial paper with top tier credit rating, to support the commercial paper market and reduce the rollover risk. Another programme, initiated in November 2008, was the TALF (Term Asset Backed Securities). This was aimed at addressing the funding liquidity problem in the securitisation markets for consumer and business ABS (Asset-Backed Securities) and CMBS (Collateralised Mortgage-Backed Securities). Under this programme, the Federal Reserve extended term loans collateralised by securities to buyers of certain high-quality ABS and CMBS, with the intent of reopening the new-issue ABS market. The programme provided both liquidity and capital to the consumer and small business loan asset-backed securities markets: the Fed lent money against asset-backed securities while the Treasury Department provided $100 billion in credit protection from its Troubled Asset Relief Program (TARP) to the TALF (as a cushion against losses on the ABS collateral). On top of this asset-buying programmes, the Fed also introduced a number of facilities aimed at helping the banks to meet their liquidity needs, such as the Term-Auction Facility (TAF) that was intended to provide liquidity with a maturity of one month against the same kind of collateral that could be used to borrow overnight at the Fed’s discount window, but without the ‘stigma effect’ that was associated with the use of the discount window.

Figure 4: Size of asset side of the Fed’s balance sheet, in % of GDP

Source: FED

As noted in Joyce et al (2012), there is a broad consensus in studies estimating the impact of QE on financial markets that it has been successful in reducing government bonds rates. More precisely, Gagnon et al (2011) shows that the Fed’s QE1 between December 2008 and March 2010 had significant and long-lasting effects on longer-term interest rates on a variety of securities, including Treasuries', agency mortgage-backed securities and corporate bonds. Estimations suggest a fall in 10-year term premium by somewhere between 30 and 100 basis points overall[8] and substantial effects on international long-term rates and the spot value of the dollar. Concerning the MBS purchase programme, Hancock and Passmore (2011) focus specifically on whether it has lowered mortgage rates, and conclude that the programme’s announcement reduced mortgage rates by about 85 basis points in the month following the announcement, and that it contributed an additional 50 basis points towards lowering risk premiums once the programme had started.

As far as liquidity measures are concerned, Ashcraft et al (2009) assess the effectiveness of the TALF by observing volumes and patterns of ABS and CMBS issuance as well as liquidity conditions in these markets. Overall, they find that improvement in market conditions and liquidity in the term ABS and CMBS markets in 2009 was dramatic, particularly in view of the lower-than-expected volume of lending through TALF. A total of $71.1 billion in TALF loans was requested and the volume of outstanding loans peaked in March 2010 at $48.2 billion, although the programme was authorised to reach $200 billion and at one point up to $1 trillion in loan volume was envisioned. Through the TALF programme, the Federal Reserve seems to have been able to prevent the shutdown of lending to consumers and small businesses, while limiting the public sector’s risk.

Estimating the macro impact of QE poses a number of difficult challenges given other potential factors that could also have influenced the economic developments of the period in which QE has been implemented. Therefore, the various results found in the literature have a higher variance. That’s why we would recommend focusing on the sign of the effect more than on its size. According to Chung et al (2012), the combination of QE1 and QE2 raised the level of real GDP relative to baseline by 3%, and inflation is 1% higher than if the Federal Reserve had not carried out the programme. They calculate that this would be equivalent to a cut in the federal funds rate of around 300 basis points from early 2009 to 2012. In contrast, Chen et al (2012) find that QE2 policy increased GDP growth by 0.4% on impact and has a minimal impact on inflation (equivalent to an effect of a 50-basis point cut in the federal funds rate). These findings show that QE has been effective (even though the effect can appear to be quite small in comparison to size of the asset purchases in terms of GDP). In terms of choice of the asset to buy, some papers such as Woodford (2012) and Krishnamurthy and Vissing-Jorgensen (2013) suggest that QE is much more effective when it takes the form of credit easing, i.e. when private assets are bought.

1.2.2 Unconventional monetary policy in the UK

The Bank of England began its quantitative easing programme in January 2009 and purchased £200 billion worth of mostly medium- and long-term government bonds from the non-bank private sector by January 2010. It made further purchases in 2011 and 2012, which took the total amount to £375 billion.

Figure 5: Size of asset side of the BoE’s balance sheet, in % of GDP

Source: BoE

There is also a broad consensus in the empirical literature that the Bank of England’s quantitative easing had significant effects on gilt yields but also on corporate bond rates and on the sterling exchange rate[9]. As in the US, conclusions on the impact on GDP and inflation in the UK differ in magnitude, but all research papers report positive impacts. For instance, in a recent paper Weale and Wieladek (2014) estimated that asset purchases equivalent to one percent of GDP led, respectively in the US and the UK, to a 0.36 and 0.18 percentage-point increase in real GDP and to a 0.38 and 0.3 percentage-point increase in CPI after five to eight quarters.

2. 2014: Addressing weak inflation in the euro area

2.1 What is the current problem to solve in the euro area?

The ECB’s current situation is very different from the one it faced in the immediate aftermath of the financial crisis. The liquidity crises in the banking sector and in the periphery’s sovereign markets seem to be fading as speculation about the break-up of the euro area has clearly receded. The interbank market has been revived and European sovereign yields are now at very low levels, including for periphery countries, since uncertainty about the integrity of the euro area was dissipated by President Draghi’s commitment to do “whatever it takes” to preserve it, when he announced the OMT programme in September 2012. On top of that, the structural weaknesses of the European banking sector are gradually being mended thanks to the ECB’s Comprehensive Assessment currently taking place.

The main problem for the ECB at the moment is that inflation in the euro area has been falling since late 2011 and has been below one percent since October 2013. Core inflation, a measure that excludes volatile energy and food price developments, has developed similarly. Five of the 18 euro-area member countries (Cyprus, Greece, Portugal, Slovakia and Spain) have experienced negative rate of inflation in the last few months. Even in the countries that are not in a recession, such as Belgium, France and Germany, inflation rates are well below the euro-area target of close to but below two percent. More worryingly, the ECB’s forecast suggests that inflation will not return to close to two percent in the medium term.

In the current European circumstances, low overall euro-area inflation implies that in some euro-area member states inflation has to be very low or even negative in order to regain competitiveness relative to the core. The lower the overall inflation rate, the more periphery inflation rates will have to fall in order to achieve the same competitiveness gains. Given that wages are often sticky and rarely decline, significant unemployment increases can result from the adjustment process. In addition, lower-than-anticipated inflation undermines the sustainability of public and private debt if the debt contracts are long-term nominal contracts. For governments, falling inflation rates often mean that nominal tax revenues fall, which makes the servicing or repayment of debt more difficult.

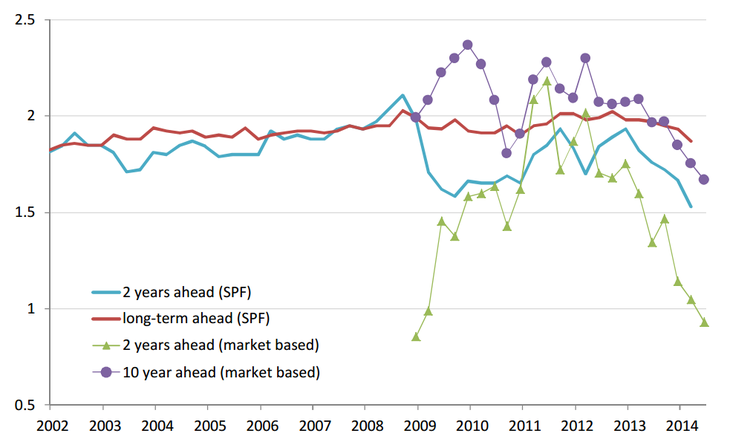

More worryingly for the ECB, inflation expectations have been falling since at least mid-2012. Figure 6 presents expectations from two sources (an ECB survey and a market-based indicator) and for two maturities. The two-year-ahead expectations are significantly below two percent and even below one percent according to the market-based indicator. In the period relevant for the ECB, inflation expectations have thus become de-anchored from 2 percent. Lack of ECB action when the ECB’s own medium-term inflation forecasts fell below the two percent threshold was a signal to markets that probably resulted in the downward revision of longer-term inflation expectations. The ECB is now less effective in anchoring longer-term expectations to, or close to, the 2 percent level.

Figure 6: Inflation expectations: ECB’s survey of professional forecasters (SPF) and market-based inflationary expectations in the euro area, 2002Q1-2014Q2

Source: ECB’s Survey of Professional Forecasters and Datastream. Note: In the ECB’s survey the horizon of “Long term” is not specified. Market-based expectations refer to overnight inflation swaps (OIS), which can be used as a market based proxy for future inflation expectations. The 2014Q2 values of market-based expectations are the average during 1-23 April 2014, while the latest available values for the SPF are end of March 2014.

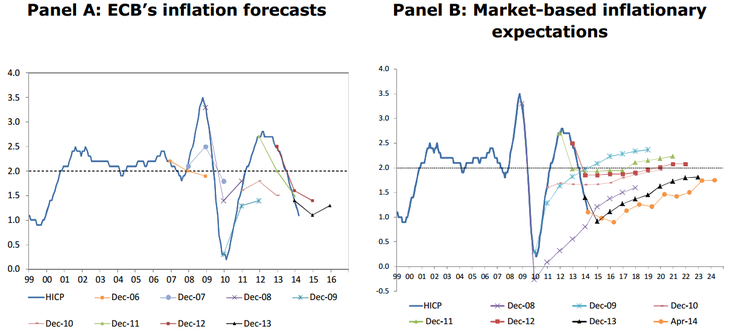

There are two other reasons that suggest that the ECB should have adopted additional monetary stimulus since the beginning of 2014. First, at a low level of inflation, the costs of deviation from the ECB’s forecast inflation are highly asymmetric. If inflation is higher than forecast, it would mean that inflation would be closer to the two percent threshold – a benign development. But if inflation is lower than forecast, then countries in the euro-area periphery would have to maintain even lower inflation or higher deflation, with risks for the sustainability of public and private debt. Second, the ECB’s inflation forecasts and market expectations have been unable to predict significant deviations from the two percent threshold (Figure 6). When there was a sizeable deviation, ECB forecasts and market expectations both predicted a gradual return to two percent, which happened in some cases (see, for example, the December 2011 forecast of the ECB), but most of the time did not.

Figure 7: Inflation forecasts/expectations and actual inflation in the euro area

Source: Datastream, ECB. Note: The HICP is defined as a 12-month average rate of change; in panel A, the ECB Staff projections indicate a range referred to as „the projected average annual percentage changes” (see https://www.ecb.europa.eu/mopo/strategy/ecana/html/table.en.html). For simplicity, we take the average of the given range. In panel B, market-based expectations refer to overnight inflation swaps (OIS), which can be used as a proxy for future inflation expectations.

Overall, inflation has been falling significantly and so have inflation expectations. Inflation forecasts have proved consistently too optimistic about the return of inflation to the two percent threshold in the euro area. The ECB’s own forecast suggests that euro-area inflation will not return to close to two percent in the medium term, and we see a substantial risk that it will not return to this level even in the longer term.

2.2 Will the new measures announced in June by the ECB be enough to bring back inflation to the 2% threshold in the medium term?

As previously explained in Claeys et al (2014b), the ECB announced during its June 2014 press conference a broad package of measures to try to tackle the low inflation problem. The package aims to (a) ease the monetary policy stance, (b) enhance transmission to the real economy, (c) reaffirm the ECB's determination to use unconventional instruments if needed.

In our assessment, the package really aims to tackle (a) and (b) but it is not a serious attempt to change inflationary dynamics with quantitative easing. We expect that the bundle of measures will have an effect on inflation. However, it is not as aggressive as it may look at first sight and further measures will likely be needed later.

This package is really about a slight easing of monetary policy and about an attempt to improve monetary policy transmission by restoring the bank-lending channel. However, the small cut in interest rates (including putting the ECB deposit rate in negative territory) will have minor effects, while the effectiveness of the targeted longer term refinancing operation (TLTRO) will depend on whether banks will be ready to take up the liquidity. The problem with the euro area currently is, however, not the lack of liquidity but the lack of lending to the real economy. As explained earlier, banks actually pay back their previous LTROs. One of the main improvements of the TLTRO over the previous LTROs is that it will carry a fixed rate (current MRO rate + 10 basis points, i.e. 0.25% at the moment), and thereby a financial incentive to borrow from the ECB, as rates cannot go down further but instead can increase during the next four years. The other main improvement is that TLTRO is conditional on new lending to the real economy and to corporations in particular. However, all depends on the willingness of banks to use the TLTRO, but most importantly on whether there will be significant demand for credit coming from the corporate sector. In many countries, debt in the corporate sector is actually quite high and the sector is attempting to deleverage. So our take is that the TLTRO will help to reduce fragmentation but its effect on inflation may be less significant than hoped.

The decision to suspend the sterilisation of the liquidity injected under the Securities Markets Programme (SMP) is questionable. The SMP had a particular goal: to address the malfunctioning of securities markets and to restore an appropriate monetary policy transmission mechanism, while not affecting the stance of monetary policy. With this decision, its aim is now changed to affect the stance of monetary policy. Such a change of a key parameter of an ECB decision undermines the reliability of other ECB commitments, which in turn introduces uncertainty about the parameters of other longer-term ECB commitments. If the ECB wanted to inject €175 billion liquidity into euro-area money markets (the current amount of SMP holdings), it would have been preferable to announce a new asset purchase programme to this end.

In our view, the announcement of preparatory work for an ECB ABS purchase programme is more significant (even though the ECB has not provided any details about the size or the timing of those purchases). We expect this to lead to the emergence of a larger ABS market. However, the ABS market is currently very small, and the ECB intends to focus on ABS based on real loans to corporations (and not on complex derivatives, which is a good thing) and to exclude the ABS for residential mortgage-backed securities (RMBS), which is by far the largest ABS market in the euro area (as explained in the next section). So in fact, if the ECB was to decide to buy, it would very quickly buy up the entire current market. Consequently, the ECB's asset-purchase programme might be quite limited in scope. Of course, one could hope that the market will increase if the ECB starts buying, but it needs to be seen if the market can develop sufficiently quickly, as there are some regulatory barriers. The effect of this measure is again going to be mostly via better credit conditions. It will not substantially operate through a portfolio re-balancing effect. In the absence of a large-scale ABS purchase programme and with subdued demand for credit, the impact on the exchange rate could be quite limited.

The element that is still missing in the package is a monetary policy measure that would substantially kick-start inflation in the core euro-area countries. A significant QE programme would have effects on core-euro area inflation as well as periphery inflation. The current package might not do that. Even though we welcome that the ECB has finally acted with a broad package, we think that further measure will likely be needed. We continue to believe that a more aggressive quantitative easing programme would anchor inflation expectations more significantly.

2.3 Towards a large-scale asset purchase programme?

As explained in detail in Claeys et al (2014a), we believe that the only option left for the ECB to be able to bring back inflation to the 2% thresholds as soon as possible is to follow the path of the Fed and the BoE and the adopt a quantitative easing strategy. However, given the differences between the euro area and the US or the UK, asset purchase will have to take a different form than in these countries. The following section summarises our recommendations on how a significant ECB asset-purchase programme should be designed to be effective and to bring back inflation and inflation expectations towards the 2% threshold in the euro area in the medium term.

2.3.1 Asset purchase: size of the programme

Setting the appropriate size of asset purchases is far from easy. Some analysis considered the total amount of asset purchases by the Bank of England and the Fed and suggested similar magnitudes for the euro area (20 to 25% of GDP, i.e. €1.9 to 2.4 trillion).

In our view, a more relevant benchmark is the amount of purchases by the Federal Reserve in its third round of quantitative easing (QE3), announced in light of the weak economic situation of the US economy at a time when the acute face of the financial crisis was over – a situation that has similarity to the current euro-area situation. In September 2012, the Federal Reserve announced it would purchase $40 billion (€29 billion) agency mortgage-backed securities per month, an amount increased to $85 billion (€61 billion) in December 2012 (by adding $45 billion per month of Treasuries). Given that the euro area’s economy is about 30 percent smaller than the US economy, the same size, as a share of GDP, would be between €20 and €40bn per month in the euro area.

2.3.2 Asset purchase: design principles

In our view, the ECB will have to choose which assets to buy using five main criteria.

- First, the ECB should buy assets that lead to the most effective transmission to inflation.

- Second, there should be sufficient volume of the asset available, to ensure that the ECB can purchase appropriate quantities while not buying up whole markets.

- Third, the ECB should try to minimise the impact on the private-sector allocation process. While QE by definition changes relative prices, the ECB should avoid buying in small markets and distorting market pricing too much. The more the ECB becomes a player in a market, the more it can be subject to political and private-sector pressures when it wants to reverse the purchases.

- Fourth, the ECB should buy only on the secondary markets in order to allow the portfolio-rebalancing channel to work effectively. Purchasing on the primary market would imply the direct financing of entities, which should be avoided.

- Fifth, the assets should only originate from the euro area and be denominated in euros, because of the February 2013 G7 agreement.

The Treaty gives a mandate to the ECB to maintain price stability, not to protect its balance sheet. Some criteria on riskiness should be adopted, but we recommend a reasonable low threshold for credit risk, such as restricting asset purchases only to the eligible collateral (without any additional eligibility criterion).

2.3.3 Asset purchase: composition

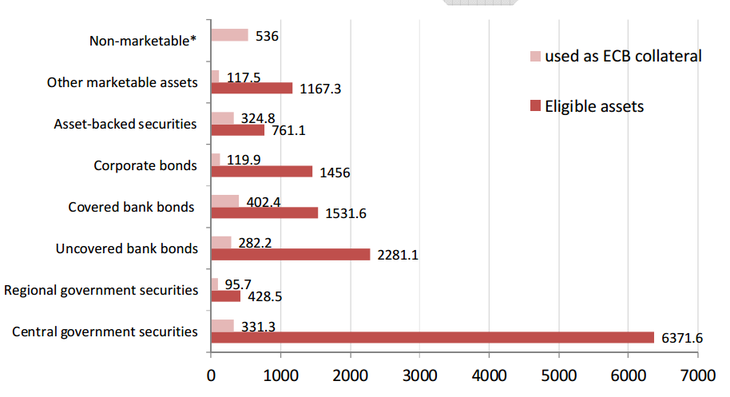

According to the ECB, total marketable assets eligible as collateral represented almost €14 trillion at the end of 2013 (Figure 8), equivalent to 146 percent of euro-area GDP[10]. About half of the Eurosystem’s eligible collateral pool at the end of 2013 consisted of government bonds, while the other half was split between uncovered bank bonds, covered bank bonds, corporate bonds, Asset Backed Securities and other marketable assets (which include the debts of EU rescue funds and the European Investment Bank).

A natural starting point for an ECB asset purchase programme would be euro-area wide government bonds, which do not exist. The closest proxy would be the bonds of European debt such as bonds issued by the European Financial Stability Facility (EFSF), the European Stability Mechanism (ESM), the European Union and the European Investment Bank (EIB). The total available euro-denominated pool of these bonds is around €490bn (€230bn for EFSF/ESM, €60bn for EU, €200bn for EIB). Buying such pan-European assets would not affect the relative yields of euro-area sovereign debts and would not distort the market allocation process within the private sector.

Figure 8: Eligible assets and assets used as ECB collateral (€ bns)

Source: ECB;

Note: Eligible assets are in nominal values; assets used as ECB collateral are after haircuts and valuation issues. Latest data available: 2013 Q4

National sovereign debt would be a natural step as the bond market is very large and the positive effects of such a QE would be significant, via portfolio rebalancing, as well as the exchange rate, wealth and signalling channels. However, the purchase of national government debt is more complicated for the ECB as a supranational institution without a supranational euro-area treasury as a counterpart, than it was for the Fed or the Bank of England. First, with 18 different sovereign debt markets, the ECB would have to decide, which sovereign debt to buy. The purchase would alter the spreads between countries and change the relative price of sovereign debts, which may expose the ECB to political pressure and lead to moral hazard. Second, the treaty prohibits the monetary financing of government debt, and since the goal of asset purchase will be to meet the ECB’s primary objective of price stability, purchase of government bonds would be allowed if the risk of monetary financing could be excluded. Experience proves that all ECB bond-buying programmes are controversial and politically sensitive in this respect. Third, the ECB has a well-defined sovereign bond purchase programme, the OMT, which is a tool to improve monetary policy transmission in countries under financial assistance. It is debatable whether a QE programme based on capital keys of the ECB would undermine the logic of the OMT programme, but this could be a risk and it should be avoided.

The second largest asset class is bank bonds, with €3.8 trillion available in eligible covered and uncovered bonds. Among the other effects, the reduction in market yields would also reduce the yields on newly issued bank bonds, thereby allowing banks to obtain non-ECB financing at a lower cost. This would improve bank profitability and could improve the willingness of banks to lend. However, bank bonds should be excluded from the ECB asset purchase programme until the ECB’s Comprehensive Assessment is concluded. Until then, ECB purchases would lead to serious conflicts of interest at the ECB and would make a proper assessment by the ECB more difficult. Moreover, those banks, for which the outcome of the Assessment is unsatisfactory, should continue to be excluded from the ECB’s asset purchases until they have implemented all the required changes to their balance sheets. This might take several months after the completion of the Comprehensive Assessment.

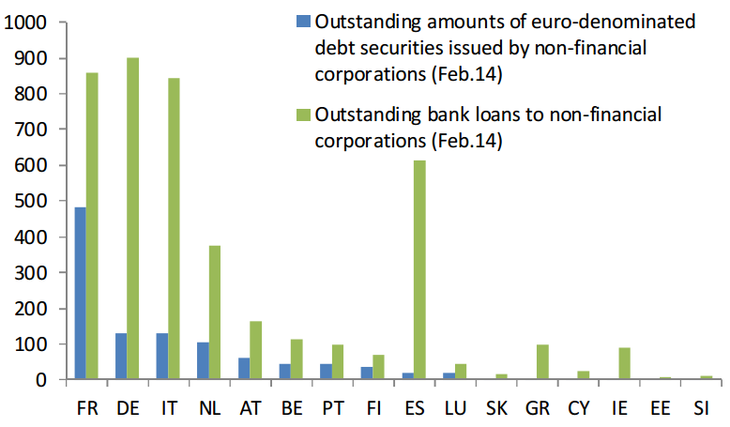

While there is no precise data on their magnitude, we estimate that the lower bound of eligible euro-area corporate bonds would be €900 billion. In addition, the supply of corporate bonds in the euro area has been growing considerably since 2009. The euro-area corporate bond market is highly concentrated (figure 9), with the main issuers of corporate bonds being French companies. However, for portfolio rebalancing to work, the origin of the corporate bonds is of less importance. The beneficial effect would come from the fact that the current owners of the corporate bonds would sell their bonds and use the cash for different purposes throughout the euro area. The purchases would encourage new issuance of corporate bonds everywhere and lead to a diversification of the sources of funding. Lower funding costs for corporations should induce more corporate investment.

Figure 9: Bonds vs. loans – financing of EU non-financial corporations (€ bns)

Source: ECB. Note: The difference between the amount reported in this figure and the total eligible corporate bonds shown on Figure 10 comes from the fact that here we only consider corporate bonds issued by euro zone corporations, whereas eligible collateral include corporate bonds issued in the whole European Economic Area (EU countries and Iceland, Liechtenstein and Norway); see here:

Another class of assets that could be bought by the ECB is asset backed securities (ABS). Yearly securitisation issuance – which peaked in 2008 – is much lower than in the US and has been decreasing since 2008. The total outstanding stock of securitised products has been stagnating at around €1.06 trillion for the euro area compared to €2.5 trillion in the US (AFME, 2014). Products eligible as collateral for the ECB amount to about €761 billion, but some of them originate from outside the euro area. We estimate that the lower bound of eligible euro-area ABS would be €330 billion. It is worth highlighting that defaults on ABS in Europe have ranged between 0.6-1.5 percent on average, against 9.3-18.4 percent for US securitisations since the start of the 2007-08 financial crisis[11]. The regulatory landscape for securitised products has also changed considerably since the crisis and made the products safer and more transparent[12].

Considering the total amount of European ABS, more than half (€612 billion) is based on residential mortgages, while SME ABS constitute a smaller part (€116 billion). That is why we think that ECB should be buying also RMBS as they represent the biggest pool of ABS and would allow the ECB to have a more significant programme without buying the whole market. As shown in Wolff (2014), the ECB should not be afraid of a potential housing bubble in Germany given that the current price increase is not financed by a rise in the volumes of mortgages in Germany.

The ABS stock outstanding is unequally distributed across countries[13], with the main issuers being different from the main issuers of corporate bonds. ABS purchases would be concentrated on the Netherlands, Spain and Italy and could therefore be a good geographical complement to corporate bond purchases, which would be concentrated in France, Germany and Italy. An ECB purchase could promote the development of securitisation in the euro area. The potential for securitisation is relevant, as many loans would qualify for securitisation and in March 2014 the outstanding amount of loans to non-financial corporation stood at €4.2 trillion and to household at 5.2 trillion in the EU[14]. From a monetary policy perspective, it would be very beneficial to create ABS that are based on a portfolio of European assets. Ideally, the credit risk should be pooled at the level of the private sector, thereby deepening cross-border financial integration. However, the ECB should not wait for developments in the ABS market to start buying securitised products.

REFERENCES

- Chen, Han; Cúrdia, Vasco and Ferrero, Andrea (2012) ‘The macroeconomic effects of large-scale asset purchase programs’, The Economic Journal, vol. 122(564), pp. F289–315, November

- Chung, Hess; Laforte, Jean-Philippe; Reifschneider, David and Williams, John C. (2012), ‘Estimating the macroeconomic effect of the FED’s asset purchases’, FRBSF Economic Letter 2001/03, January

- Claeys G., Z. Darvas, S. Merler and G. Wolff (2014a), ‘Addressing weak inflation. The European Central Bank's shopping list’, Bruegel Policy Contribution, 2014/05 May

- Claeys G., Z. Darvas, and G. Wolff (2014b), ‘ECB shows activism but falls short of true QE’, Bruegel Blog, June 5

- Darvas, Zsolt (2013), ‘Banking system soundness is key to more SME’s financing’, Bruegel Policy contribution 2013/10, July

- Gagnon, Joseph; Raskin, Matthew; Remache Julie and Brian Sack (2011), ‘The Financial Market Effects of the Federal Reserve’s Large- Scale Asset Purchases’. International Journal of Central Banking 7, no. 1: 3–44.

- Hancock, Diana and Wayne Passmore (2011), ‘Did the Federal Reserve’s MBS purchase program lower mortgage rates?’, Journal of Monetary Economics, vol.58 no.5, pp.498-514

- Krishnamurthy, Arvind and Annette Vissing-Jorgensen (2013) ‘The Ins and Outs of LSAPs’

- Krugman, P. (1998). ‘It's baaack: Japan's slump and the return of the liquidity trap’. Brookings Papers on Economic Activity, 137-205.

- Joyce, M., D. Miles, A. Scott, and D. Vajanos (2012), ‘Quantitative easing and unconventional monetary policy – an introduction’ The Economic Journal, 122, pp. F271-288, November

- Meier (2009) ‘Panacea, Curse, or Nonevent?’ Unconventional Monetary Policy in the United Kingdom.’ IMF Working Paper 09/163, August

- Papadia, Francesco (2013) ‘Should the European Central Bank do more and go negative?’, Blog post: Money matters? Perspectives on Monetary Policy

- Sapir, André and Wolff, Guntram B. (2013), ‘The neglected side of banking union: reshaping Europe’s financial system’, Note presented at the informal ECOFIN, September

- Weale, Martin and Tomasz Wieladek (2014), ‘What are the macroeconomic effects of asset purchases?’, Bank of England, External MPC Unit, Discussion Paper no. 42, April

- Wolff, Guntram (2013), ‘The ECB’s OMT programme and German constitutional concerns’, in Brookings, The G20 and Central Banks in the new world of unconventional monetary policy

- Wolff, Guntram (2014), ‘Easier monetary policy should be no worry to Germany’, Bruegel Blog, June 4

[1] Excess liquidity can be computed as (current account + deposit facility – minimum reserves) or as (MRO + LTRO + Marginal Lending – Autonomous Factors – minimum reserves)

[2] ee Angelini et al. (2011); Lenza et al. (2010); Darracq Pariès and De Santis (2013); Abbassi and Linzert (2011)

[3] See Manganelli (2012); De Pooter et al. (2012); Ghysels et al. (2012)

[4] European Central Bank, 2012. “6 September 2012 - Technical features of Outright Monetary Transactions.” Available at http://www.ecb.europa.eu/press/pr/date/2012/html/pr120906_1.en.html

[5] European Central Bank, 2013. “Introductory statement to the press conference (with Q&A)” available at http://www.ecb.europa.eu/press/pressconf/2013/html/is130704.en.html

[6] Praet P. (2013). “Forward guidance at the ECB”, http://www.voxeu.org/article/forward-guidance-and-ecb

[7] The expression credit easing is also used when private sector securities are purchased.

[8] Other papers suggest similar results: D’Amico and King (2010), Krishnamurthy and Vissing-Jorgensen (2011), Neely (2012) and Hamilton and Wu (2012).

[9] For instance Meier (2009) shows that initial QE announcements reduced gilt yields at least by 35–60 basis points whereas Joyce et al. (2011) estimated that medium-to- long-term gilt yields fell by 100 basis points overall, summing up the two-day reactions to the first round of the MPC’s announcements on QE purchases during 2009–10. They also found that similar falls occurred in corporate bond yields and that there were also announcement effects on the sterling exchange rate, therefore validating the existence of a portfolio rebalancing channel and exchange rate channel of QE.

[10] In the permanent collateral framework, only euro-denominated securities are accepted, but under the temporary collateral framework introduced during the crisis, also assets denominated in USD, JPY and GBP are accepted. See: http://www.ecb.europa.eu/pub/pdf/other/collateralframeworksen.pdf

[11] http://www.bis.org/review/r140407a.htm

[12] Retention requirements – which should induce seller of ABS to monitor carefully the underlying collateral – have been introduced in the context of the EU Capital Requirements Directive, and the EBA is working on the technical details (i.e. 5% retention requirement):

https://www.eba.europa.eu/-/eba-publishes-final-draft-technical-standards-on-securitisation-retention-rules

[13] See details in Claeys et al. (2014a)

[14] According to the calculation in Darvas (2013), out of these €4.2 trillion, the stock of SME loans in the EU in 2010 represents approximately €1.7 trillion and the largest stocks of SME loans were in Spain (€356bn), followed by Germany (€270bn), Italy (€206bn) and France (€201bn).

Related content

What will it cost the European Union to pay its economic recovery debt?

Servicing the EU debt until 2058 seems feasible, despite increased borrowing costs, but member countries must make choices about budget funding

Inflation inequality in the European Union and its drivers

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition