Improving the role of equity crowdfunding in Europe's capital markets

Crowdfunding is a growing phenomenon that encompasses several different models of financing for business or other ventures. We assess the potential ro

Summary

Crowdfunding is a growing phenomenon that encompasses several different models of financing for business or other ventures. Despite the hype, equity crowdfunding is still the smallest part of the crowdfunding market. Because of its legal framework, Europe has been at the forefront of equity crowdfunding market development.

Equity crowdfunding is more complex than other forms of crowdfunding and requires proper checks and balances if it is to provide a viable channel for financial intermediation in the seed and early-stage market in Europe. It is important to explore this new channel of funding for young and innovative firms given the critical role these start-ups can play job creation and economic growth in Europe.

We assess the potential role of equity crowdfunding in the overall seed and early-stage financing market and highlight the potential risks of equity crowdfunding. We describe the current state of play in this nascent industry, considering both the innovations introduced by market operators and existing regulation. Currently in Europe there is a patchwork of national legal frameworks related to equity crowdfunding and this should be addressed in a harmonised way.

Introduction

Crowdfunding is increasingly attracting attention, most recently for its potential to provide equity funding to start-ups. Providing funding to young and innovative firms is particularly relevant given their importance for job creation and economic growth (OECD, 2013; Haltiwangner et al, 2011; Stangler and Litan, 2009). In addition, at a time when banking intermediation is under pressure (Sapir and Wolff, 2013), it is important for European Union policymakers to further explore alternative forms of financial intermediation. But questions remain about the appropriateness of crowdfunding for providing seed and early stage equity finance to new ventures and how this market could be developed and regulated.

While there is growing hype around crowdfunding, there are also many wrong perceptions. The bulk of crowdfunding is for philanthropic projects (in the form of donations), consumer products often for creative ventures such as music and film (in the form of pre-funding orders) and lending. Equity crowdfunding, sometimes called crowdinvesting is relatively new and currently comprises the smallest part of the crowdfunding market. However, it is currently more active in Europe than in other regions.

Growth of crowdfunding

Crowdfunding can be defined as the collection of funds, usually through a web platform, from a large pool of backers to fund an initiative. Two fundamental elements underpin this model and both have been enabled by the development of the internet. First, by substantially reducing transaction costs, the internet makes it possible to collect small sums from a large pool of funders: the crowd. The aggregation of many small contributions can result in considerable amounts of capital. Second, the internet makes it possible to directly connect funders with those seeking funding, without an active intermediary. Crowdfunding platforms assume the role of facilitators of the match.

While people tend to talk about crowdfunding in general, the crowdfunding phenomenon encompasses quite heterogeneous financing models. There are four main types:

- Donation-based, in which funders donate to causes that they want to support with no expected compensation (ie philanthropic or sponsorship-based incentive).

- Reward-based, in which funders’ objective for funding is to gain a non-financial reward such as a token gift or a product, such as a first edition release.

- Lending-based (crowd lending), in which funders receive fixed periodic income and expect repayment of the original principal investment.

- Equity-based (usually defined as crowdinvesting), in which funders receive compensation in the form of fundraiser’s equity-based revenue or profit-share arrangements. In other words, the entrepreneur decides how much money he or she would like to raise in exchange for a percentage of equity and each crowdfunder receives a pro-rata share (usually ordinary shares) of the company depending on the fraction of the target amount they decide to commit. For example, if a start-up is trying to raise €50,000 in exchange for 20 percent of its equity and each crowdfunder provides €500 (1 percent of €50,000), the crowdfunder will receive 0.20 percent (1 percent of 20 percent) of the company’s equity.

The four models vary in terms of complexity and level of uncertainty. The donation-based model is the simplest. Legally the transaction takes the form of a donation. The risk is that the project does not achieve its declared goals, but the backer does not expect any material or financial return from the transaction. Equity crowdfunding is the most complex. From a legal standpoint, the funder buys a stake in the company, the value of which must be estimated. Moreover, the level of uncertainty in equity crowdfunding is much greater compared to the other models because it concerns the entrepreneur’s ability to generate equity value in the company, which is extremely difficult to assess. Overall, these complexities pose problems that are distinct and more fundamental than those of the other crowdfunding models. These complexities require special attention from policymakers, as this Policy Contribution will discuss.

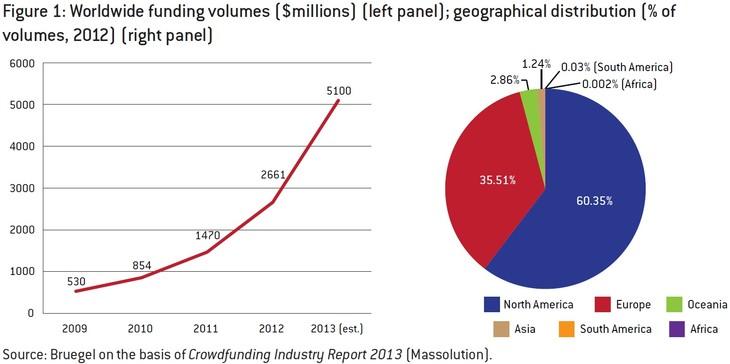

In general, crowdfunding is experiencing exponential growth globally. In the period 2009-13, the compound annual growth rate (CAGR) of the funding volumes was about 76 percent with an estimated total funding volume of $5.1bn in 2013. In terms of geography, the biggest market has been North America (and mostly the US where the concept of crowdfunding started) with 60 percent of the market volume, followed by Europe, which has 36 percent.

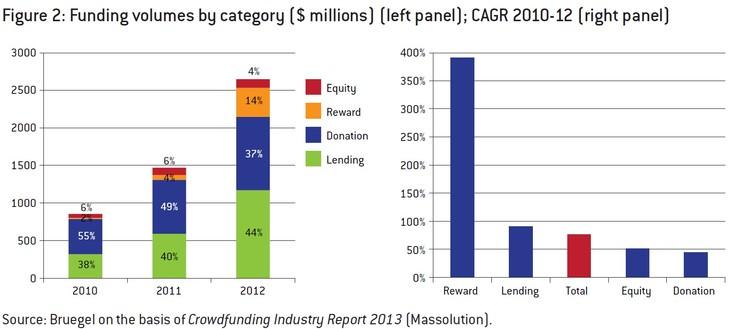

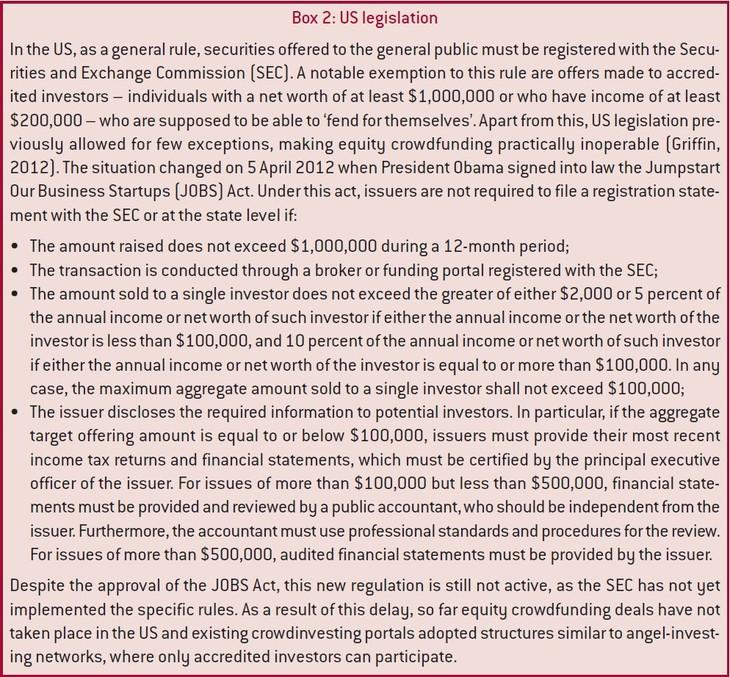

Equity crowdfunding is the smallest category of the overall industry and had a CAGR of about 50 percent from 2010 to 2012. Most of that growth was through European crowdfunding platforms because legal barriers currently prevent the development of equity crowdfunding in the US (see Box 2). As a result, Europe is currently the leading market for this financing model (see further discussion in section 4).

While in Europe equity crowdfunding is growing, the understanding of its risks and opportunities is still limited. We first assess the potential role of equity crowdfunding in the overall seed and early-stage financing market. Second, we point out the potential risks of equity crowdfunding. Third, we describe the state of this nascent industry considering both the innovations introduced by market players and existing regulation. Finally, we discuss the implications of our analysis for policy.

The seed and early-stage financing market

Equity crowdfunding is receiving attention from policymakers as a potential source of funds for start-ups, a segment of the economy that has limited access to finance. Young firms have no track record and often lack assets to be used as guarantees for bank loans. In addition, information asymmetries make it difficult for investors to identify and evaluate the potential of these firms.

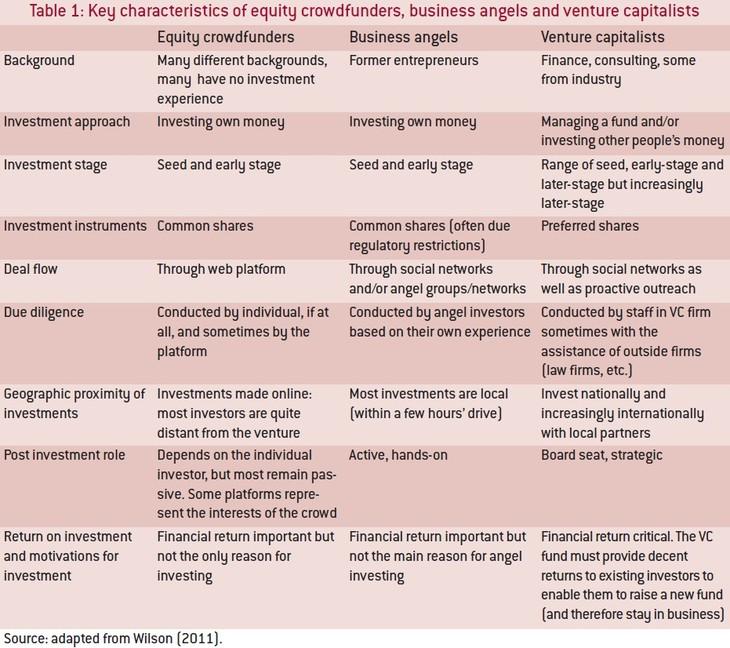

Traditionally there have been three sources of equity funding for young innovative firms: founders, family and friends; angel investors; and venture capitalists.

- The most common source of funding for new ventures is the founders’ own capital, even if that is funded through credit cards. Family and friends sometimes also provide finance to the entrepreneur in the first phases of development of the start-up (seed stage).

- Angel investors are experienced entrepreneurs or business people that choose to invest their own funds into a new venture. They typically invest in seed and early stage ventures with amounts ranging from $25,000 to $500,000. Angels invest not only for the potential financial return, but in many cases to give back by helping other entrepreneurs.

- Venture capital is considered ‘professional’ equity, in the form of a fund run by general partners, and aims at investments in firms in early to expansion stages. The source of capital pooled into venture capital funds is predominately institutional investors. Venture capital firms typically invest around $3m and $5m per round in a company.

The contributions of angel investors and venture capital firms are not limited to the provision of finance. They are actively involved in monitoring the companies in which they invest and often provide critical resources such as industry expertise and a valuable network of contacts (Gorman and Sahlman, 1989; Baum and Silverman, 2004; Hsu, 2004).

The importance of angel investors has increased in recent years given the difficulties young innovative firms face in securing finance from other channels (Wilson, 2011). As a result of the financial crisis, banks are even more reluctant to fund young firms because of their perceived riskiness and lack of collateral (Wilson and Silva, 2013). Meanwhile, venture capital firms are focusing more on later-stage investments and have left a significant funding gap at the seed and early stage. Angel investors, particularly those investing through groups or syndicates, are active in this investment segment and thus help to fill this increasing financing gap.

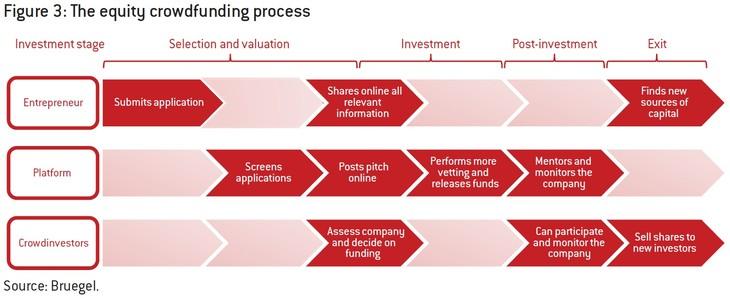

Equity crowdfunding departs from the models of traditional angel investors and venture capital firms because transactions are intermediated by an online platform. Some platforms play a more active role in screening and evaluating companies than others (see section 4). Also, their role during the investment and post-investment stages can vary dramatically. While there is a great deal of variation among the approaches adopted by the different platforms (Collins and Pierrakis, 2012), equity crowdfunding platforms generally follow the phases described in Figure 3.

Platforms usually charge companies a fee, typically 5-10 percent of the amount raised, plus sometimes a fixed up-front fee. Some platforms also charge fees to investors that are either fixed or a percentage of the amount invested or a percentage of the profit for investment. For example, Crowdcube charges entrepreneurs 5 percent plus a £1,750 fee for successful fund raising. Symbid charges entrepreneurs a €250 registration fee plus 5 percent of the amount raised and charges investors 2.5 percent of the amount invested. Seedrs charges entrepreneurs 7.5 percent of the amounts raised and charges investors 7.5 percent of the profits from the investment.

To understand how equity crowdfunding can complement the market incumbents in seed and early-stage finance, we have to consider characteristics such as investment size, investment motives, the risk/return profile, the investment model and investor characteristics.

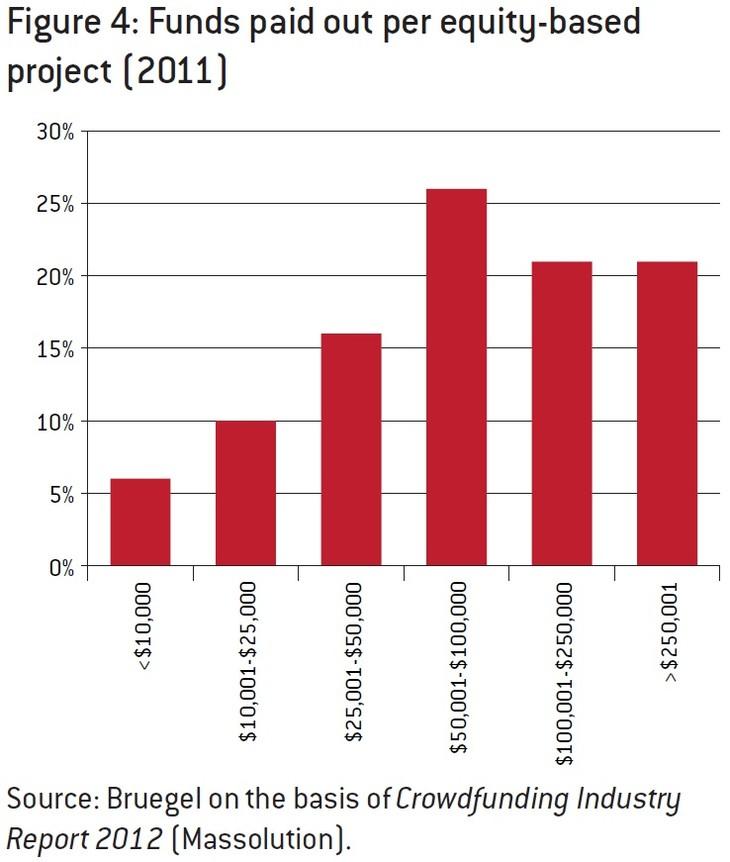

Figure 4 shows the funding per project in equity-based crowdfunding. Compared to the other sources of finance described above, we can see that equity crowdfunding mostly operates in the financing segment covered by angel investors1.

Another characteristic that equity crowdfunding has in common with angel investors is that financial return is not the sole motive for an investment. Crowdfunders might also derive social and emotional benefits from financing a company. In other words, they are likely to be motivated to provide funding to a company to be connected with an entrepreneurial venture that shares their own values, vision or interests. A survey of Seedrs2 users revealed that the three top motivations for investors to fund start-ups are the desire to help new businesses get off the ground, the ability to exploit tax reliefs3, and the hope of achieving meaningful financial returns (Seedrs, 2013).

In terms of investment preferences, venture capitals tend to concentrate on technology-based companies, which typically are high-risk/high-return investments. Angel investors tend to invest in a wider range of sectors and geographies, covering some investment segments in which venture capital typically would not invest (Wilson, 2011). Because the crowd might encompass quite heterogeneous investment motives, the investment spectrum of equity crowdfunding can be even broader. For example, Seedrs users have invested in sectors as diverse as food and drink, high-tech, art and music, fashion and apparel, real estate and many others (Seedrs, 2014). The fact that crowdinvestors derive also non-financial benefits from the investment implies that they might also be willing to accept higher risks or lower returns than an investor seeking to maximise financial returns (Collins and Pierrakis, 2012).

Unlike venture capital and angel investment, equity crowdfunding requires entrepreneurs to publicly disclose their business idea and strategy. This early information disclosure might be harmful for firms with an innovative business model that can be easily imitated (Hemer, 2011; Agrawal et al, 2013; Hornuf and Schwienbacher, 2014a). Therefore, crowdfunding might be most beneficial for start-ups that can protect their intellectual capital through means other than secrecy, or for start-ups whose business is not particularly innovative.

Another common element shared by business angels and crowdinvestors is that neither type of financing model necessarily involves an active financial intermediary that makes the investment decisions. Venture capital firms pool financial commitments from institutional investors into funds and then select a portfolio of companies over time in which they invest. For angel investors and crowdinvestors, the decision to finance a company is ultimately made by the individual investor. Some equity crowdfunding platforms pool the funds of the crowd into an investment vehicle and act towards the company as the representative of the interests of the crowd. However, even in this case the platform does not act as a financial intermediary in portfolio management for the crowd, and the decision to invest in a specific company is taken by the individual investor.

While angel investors are typically high net worth individuals who are sophisticated investors, crowdinvestors are individuals that might or might not have experience and knowledge of financial markets and early-stage financing. Moreover, while angel investors tend to invest locally, crowdinvestors might invest in start-ups that are quite distant from them. Agrawal et al (2011) show that the average distance between a revenue-sharing crowdfunding platform's entrepreneurs and investors was approximately 3,000 miles (4,828 km). According to their study, only 13.5 percent of the investors provided funds to entrepreneurs within 50 km.

Table 1 summarises the key characteristics of equity crowdfunders, angel investors and venture capitalists, highlighting their similarities and differences.

Overall, equity crowdfunding can provide a complementary channel through which start-ups can obtain finance. In addition, equity crowdfunding can provide some advantages by fully exploiting the potential of the internet.

For example, crowdfunding allows a start-up to gain online visibility in the first phases of its development. As crowdinvestors are also potential consumers, an entrepreneur can benefit from crowdfunding through early advertisement of its products and by obtaining information on potential market demand and product preferences (Agrawal et al, 2013; Hornuf and Schwienbacher, 2014a). This early assessment of demand could help to reduce inefficient investments in start-ups with weak business potential.

Compared with traditional angel investing transactions that rely mostly on word-of-mouth, crowdfunding can improve the efficiency of the market by enabling faster and better investor-company matches. Moreover, geographical factors that might affect traditional forms of seed and early-stage financing might be less important in crowdfunding (Mollick, 2013a; Agrawal et al, 2011 and 2013).

Finally, the crowdfunding industry is well-positioned to benefit from the so-called 'big data' paradigm (Agrawal et al, 2013). Being online-based, crowdfunding deals leave data trails on investors, entrepreneurs, companies and deals, unlike angel investment and even most venture capital transactions. Through time, the analysis of this data could enable crowdfunding platforms to provide better matches between investors and companies and maximise the correlation between the crowd and product demand.

Risks in equity crowdfunding

Seed and early-stage financing can be high risk but with the hope of a high return. Eurostat data4 show that in EU the one-year survival rate for all enterprises created in 2009 was 81 percent, while the five-year survival rate of all enterprises started in 2005 was only 46 percent. Despite the expertise of professional investors, the risk of investing in start-ups remains high. Shikhar Ghosh, senior lecturer at Harvard Business School, analysed data from more than 2,000 US companies that received venture financing and found that about 30-40 percent of them fail, while more than 95 percent fail to generate the expected return on investment (WSJ, 2012). There is a misconception about success rates and returns on investment in start-ups (Shane, 2008) and the average individual is not aware of the risks.

The characteristics of crowdfunding can make investments in seed and early-stage companies even riskier. Information asymmetry problems common to seed and early-stage financing are exacerbated in equity crowdfunding. Below we describe some of the issues that might arise in each phase of the investment.

Selection and valuation

Before investing in a company, business angels and venture capitalists routinely perform due diligence to assess the potential value of the firm. This can be costly in terms of time and resources. However, evidence shows that due diligence is a major determinant in achieving returns on the investment (Wiltbanks and Boeker, 2007). This expense is often justified in light of the considerable size of such investments. Because their investments are relatively small, crowdinvestors have less incentive to perform due diligence. Moreover, individual investors have the possibility of free-riding on the investment decisions of others. This implies that the crowdfunding community may systematically underinvest in due diligence (Agrawal et al, 2013).

Crowdfunders also likely lack the expertise and skills to perform adequate due diligence. Since everyone is able to join, the crowd often includes non-professional investors, who do not have the knowledge or capabilities to properly estimate the value of a company.

Finally, company valuation performed by a crowd might be affected by social biases and herding behaviour5. Evidence suggests that a crowdfunder’s investment decision might be affected by those of the other investors (Agrawal et al, 2011; Kuppuswamy and Bayus, 2013). Moreover, different studies have found that both the crowd and entrepreneurs are typically initially overoptimistic about potential outcomes (Mollick, 2013b; Agrawal et al, 2013).

Investment

Equity crowdfunding often relies on standardised contracts that are provided by the portal. However, equity investment into seed and early-stage firms often requires tailored contracts to align the interests of the entrepreneur to those of the investor. For example, venture capital and business angels use various covenants in their contracts, such as anti-dilution provisions that protect against down-rounds6, tag-along rights7 that facilitate exit opportunities, and liquidation preferences that secure higher priority in the distribution of value (Hornuf and Schwienbacher, 2014a). Moreover, in order to reduce risk exposure and increase control over the entrepreneur’s behaviour, seed and early-stage investors often split their investments into tranches that are conditional on the attainment of defined milestones. All of these mechanisms are difficult to replicate in the crowdfunding setting.

Another strategy applied by venture capitalists and business angels is to invest in a portfolio of companies in order to diversify their risk. Equity crowdfunders might be able to replicate this strategy given that crowdfunding platforms expose them to a variety of projects. However, non-professional investors might not be aware of the importance of this strategy and could potentially concentrate all their investments in a single venture. For example, Seedrs statistics show that 41 percent of investors hold only one company in their portfolio (Seedrs, 2014).

Moreover, crowdfunders might not be able to participate in follow-on investment rounds. The failure to do so might mean that the investor’s shares get diluted, thus reducing their chances to attain a positive return from the investment.

Post-investment support and monitoring

As we have described, business angels and venture capitalists not only provide finance to start-ups, but are also actively involved in increasing the value of the company. While the crowd could potentially provide active support to the venture, there are reasons to believe that this support can be less valuable than that provided by traditional seed and early-stage financiers. Given their typical small level of investment, crowdfunders have less incentive to provide active support to the company because the return for their action is lower (Agrawal et al, 2013). However, if too many investors choose to become active, it could be excessively costly for a small firm to manage a crowd of investors that want to participate. This is particularly relevant considering that the venture has limited ability to select its crowdinvestors.

Moreover, high information asymmetry also characterises the post-investment phase, thus limiting the monitoring potential of the crowd. One of the elements contributing to the increase in information asymmetry is geographical distance between funders and the entrepreneur. While this characteristic enables backers to attain access to a wider pool of entrepreneurs (and visa-versa), it also entails higher monitoring costs. Literature suggests that distance increases the costs that an investor must bear in order to monitor the venture (Grote and Umber, 2007). This is in line with the observation that venture capital funds invest predominantly in firms close to them (Lerner, 1995).

Finally, the lack of repeated interactions reduces the potential of reputation as a mechanism to incentivise the entrepreneur to behave in line with the interests of the investor (Agrawal et al, 2013). In other online marketplaces, such as eBay, participants have a low incentive to misbehave because, if they do, they might, in effect, be prevented from participating in the market in the future because of the feedback and ratings mechanisms. Since sourcing equity finance through the internet is often a one-time event for an entrepreneur, the incentives for behaving correctly are lower, which can lead to potential fraud. More active crowdfunding platforms screen companies. However, not all platforms have the same standards.

Exit

The lack of adequate monitoring is particularly worrisome in a setting in which investments often take 5-10 years or more to produce a return, if any. Crowd investors might not appreciate that long periods are necessary for these investments to either succeed or fail, or that most of these investments are unlikely to yield any return. Moreover, equity investments are mostly long-term illiquid assets. Therefore, it is important that non-professional investors are adequately informed about the illiquid characteristics of this asset class.

For equity investments to provide a return to investors, a positive 'exit' must take place at some point. This can be through an initial public offering (IPO) or, as more often the case, through a merger or acquisition (M&A). Unfortunately, these positive exits became increasingly rare during the financial crisis. In Europe, EVCA data (2013) shows that only 15 percent of venture capital exits in 2012 (in terms of number of companies) were through trade sales, and even fewer, 5 percent, were IPOs. These numbers are clearly lower than pre-crisis (2007) figures that pointed to 22 percent of exits through trade sales and 8 percent through IPOs.

For angel investments and equity crowdfunding investments, the path to a positive exit can be longer and even less likely. IPOs and M&As do not happen by chance. Venture capitalists and the firms themselves often have an exit strategy in mind from the beginning and proactively work towards making it a reality over a long period (Wilson and Silva, 2013).

In conclusion, the lack of adequate pre-investment screening and due diligence, weaker investment contracts and poorer post-investment support and monitoring can make the risk associated with equity crowdfunding significantly higher than the risk usually borne by business angels and venture capitals. Moreover, while the potential for fraud is exacerbated in the equity crowdfunding setting, information asymmetry makes investments in the start-ups of even well-intentioned entrepreneurs riskier, since the competence of the entrepreneur and the quality of the business plan cannot be properly assessed.

While there are some successful equity crowdfunding cases (such as the biotech start-up Antabio8 in France, which succeeded in producing a positive return for its investors) and failure cases (such as the liquidation of betandsleep9 or sporTrade10 in Germany), the industry still lacks a sufficient track record to assess its ability to create value for both investors and entrepreneurs.

Crowdfunding platforms and the regulatory environment

The issues we have raised demonstrate the greater exposure that equity crowdfunding market has compared to other forms of seed and early-stage investment. In particular, adverse selection problems could increase the cost of capital up to the point at which only low-quality ventures will eventually choose to seek financing through crowdfunding, while high-quality ventures will continue to secure venture capital or angel investor financing (Agrawal et al, 2013). Competition between platforms and between the crowdfunding industry and traditional financing is pushing platforms to design innovative solutions to avoid the unintended consequence of creating a ‘market for lemons’.

Overall, the main limitation of equity crowdfunding is that it allows a non-professional investor, who might lack the incentive and/or capabilities to adequately assess and monitor a start-up, to make an investment. Efforts to address this limitation to date have included the introduction of an intermediary between the crowd and the company that is able to perform these tasks, or the reduction of the crowd to only qualified investors.

The first approach involves the provision of an active intermediary that could act as a representative of the interests of the crowd in performing due diligence and monitoring start-ups. Following this trend, many platforms are active in performing due diligence, while others operate a nominee and management system in which they represent the interests of investors with the crowdfunded business (eg Seedrs). Another example is provided by platforms such as MyMicroInvest in Belgium, which allows investors to co-invest with an experienced business angel. In this case, the crowd benefits from the financial contracting skills and from the post-investment monitoring of an experienced active investor. While this approach provides some benefits, it also entails some risks: by leveraging the investment decisions of a business angel, this mechanism may increase the risk propensity of the angel, thus biasing his or her investment decisions.

A second approach is to reduce the crowd, by limiting the investment to a restricted group of people, possibly accredited investors, each contributing more capital than the average crowd investor. In this case, crowdinvesting would more closely resemble angel investor groups than the typical crowdfunding model. Examples of this model are CircleUp and FundersClub in the US or Seedups based in Ireland, whose offers are restricted to accredited investors. Other examples are platforms that impose high investment minimums, thus reducing the crowd to a few investors. Finally, some platforms (such as Seedrs and Crowdcube in the UK) require crowdinvestors to pass a test before investing in a company, to certify that they are sufficiently aware of the investment risk.

The efficacy of these measures needs to be evaluated and appropriate policies should take into account these assessments. Moreover, while the market gives incentives to platforms to adopt the best practice, some platforms could deviate from the best practices because of lack of long-term vision, incompetence or other hidden interests (Griffin, 2012). The financial crisis showed that leaving the financial market to self-regulate can be costly. Many of these crowdinvestors could lose their money before the market has time to self-correct and force out inadequate platform models.

Crowdfunding platforms have an incentive to build a good reputation by securing attractive deals for their crowds, since in the long run reputation results in market-share gains. Apart from this reputational incentive, platforms differ in the structure of fees they derive from the deals. As described in section 2, most of the platforms derive revenues as a percentage of the amount raised, while only a few (eg Seedrs) derive monetary benefit from a successful exit by imposing a fee as a percentage of investor’s profits. This typical fee structure implies that platforms derive monetary incentive to close deals while there are only reputational incentives to provide successful deals in the long run. If long-run reputational incentives are lower than short-term monetary incentives, conflicts of interest could arise and platforms might downplay investment risk to the crowd in order to secure deals. In light of this potential conflict of interest, a supervisory body for crowdfunding platforms is probably desirable.

From a legal standpoint, equity crowdfunding is currently possible in some jurisdictions by exploiting exemptions to existing securities regulations (Hornuf and Schwienbacher, 2014b). Securities laws generally require an issuer to register with the national securities authority and to comply with strict reporting standards in order to gain access to the general public. These requirements are prohibitively expensive for small firms, which are the typical beneficiaries of crowdfunding.

In the EU, exemptions as defined in national regulations pertaining to prospectus and registration requirements, allow start-ups to gain access to the general public through equity crowdfunding (Hornuf and Schwienbacher, 2014b). Exemptions include the maximum amount that can be offered to the public, the maximum number of investors to whom the offer is made, the minimum contribution imposed on investors and whether the offer is made to ‘qualified’ or ‘accredited’ investors. While these exemptions to existing securities legislation allow small firms access to the general public for financing, they also imply weaker protections for investors.

EU member states have adopted different practices on whether the equity crowdfunding platform must register as an investment intermediary or obtain a bank license. For example, in Germany, crowdinvesting platforms explicitly stating that they do not provide any investment advice or brokerage service have no obligation to provide any documentation in terms of advisory records or to act in the interest of the investor (Dapp and Laskawi, 2014). As a result, most German platforms are not registered as investment intermediaries (ECN, 2013). In the UK, platforms are regulated by the Financial Conduct Authority (FCA) (ECN, 2013; Hornuf and Schwienbacher, 2014b). In France, equity crowdfunding platforms such as Wiseed, Anaxago, Finance Utile and SmartAngels are registered as financial investment advisers, since their activities consist of advice in providing financing (ECN, 2013; Hornuf and Schwienbacher, 2014b).

Finally, national corporate laws can also have an effect on equity crowdfunding (De Buysere et al, 2012; Hornuf and Schwienbacher, 2014b). For example, because they are relatively inexpensive in most countries, closely held company types (eg private limited liabilities companies) are the typical entity type chosen by start-ups. However, in many countries these company types have limitations or might be prohibited from offering equity to new investors. Even when allowed, equity transactions for these kinds of companies often require formalities, such as notarial intervention, which increases the costs for start-ups.

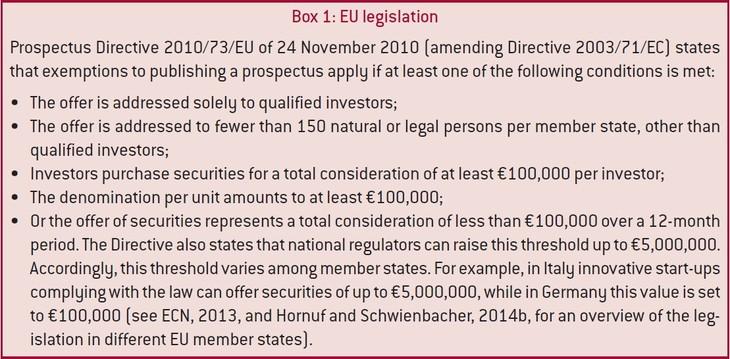

Despite the harmonising role played by Directive 2010/73/EU (Box 1), the EU remains a patchwork of different regulations. This lack of uniformity inhibits the development of a pan-European industry by making cross-border deals more difficult, and highlights the lack of consensus on whether equity crowdfunding could be welfare-enhancing or not.

Considerations for policymakers

Crowdfunding can be an additional tool for providing seed and early-stage equity finance to new ventures. However, policymakers should proceed with caution by carefully assessing the risks of this new financial intermediation tool. We argue that the challenges that equity crowdfunding poses are distinct and more complex than those posed by other forms of crowdfunding. As we have outlined, the risks also differ from other forms of seed and early-stage equity finance, such as angel investing and venture capital. Equity crowdfunding can open up additional channels for new ventures to access finance at a time when securing funding is difficult, but the risks, including those related to investor protection, need to be addressed.

These risks could result from potential fraudulent activities of start-ups or platforms or, more likely, poor investment decisions made by unsophisticated investors. The current legal framework mainly addresses this issue by reducing the exposure that individual investors can have to riskier assets. The goal is to make sure that the investor is able to bear a potential loss. However, as the equity crowdfunding volumes continue to grow, this solution does not prevent the potential loss of significant amounts of capital.

Overall, the legal framework should not allow a crowd of investors, who might lack the incentive and/or the expertise to invest in a start-up, to do so without adequate intermediation and protection. If the crowd is made up of non-qualified investors, we argue that there should be at least one participant that legally represents the interest of the crowd in the investment in a business. This participant could be the crowdfunding platform. The crowd could also be allowed to co-invest alongside professional investors. However, also in this case, the platform should take significant steps to protect the interests of the crowd from the misbehaviour of other investors. Finally, in order to monitor potential conflicts of interest of platforms, supervision by national security authorities is important.

Crowdfunding currently is a highly deregulated market with little legal protection provided to funders. In the EU, some member states have introduced ad-hoc legislation for crowdfunding, while some others will introduce new laws soon. The European Commission is currently studying equity crowdfunding, along with the other forms of crowdfunding, to assess its risks and opportunities. In this regard, the Commission started a public consultation late in 2013 and published a Communication in March 2014 (EC, 2014). At this stage, the Commission’s efforts are focused on increasing awareness of the opportunities and risks of crowdfunding, spreading best practice and improving the general understanding of this growing phenomenon. The Commission is also exploring the potential of a ‘quality label’ to spread good practice and build user confidence.

Being based online, equity crowdfunding has the potential to contribute to a pan-European seed and early-stage financial market to support European start-ups. However, in order to maximise this benefit, harmonised policies to address equity crowdfunding models should be adopted in common by all member states. This approach would maximise the benefits of equity crowdfunding and help to reduce the risks. We urge the Commission to work with member states to address the current patchwork of national legal frameworks, which constitute an obstacle to the development of this nascent model of funding across Europe.

Finally, legislators should take a holistic approach in assessing the regulatory burden on the industry. Corporate law in many countries imposes limitations or prohibits closely held company types – the typical legal form chosen by start-ups – from selling equity to new investors. These provisions are another significant obstacle to the development of equity crowdfunding. Corporate laws should be harmonised and should take into account this new financing channel for start-ups. In addition, other financial regulations which might interact with and have an impact on the market should be assessed.

In conclusion, all types of crowdfunding can provide significant and new sources of funding for many types of organisations, ranging from charities to companies. Equity crowdfunding, however, is more complex and requires the proper checks and balances if it is to provide a viable channel for financial intermediation in the seed and early-stage market in Europe.

Notes

1. Nevertheless, this distribution might not reflect simply the investment preferences of the crowd. Legal constraints currently provide upper limits to the capital that can be raised from nonqualified investors. See section 4.

2. Seedrs is an equity crowdfunding platform based in the United Kingdom. It allows users to invest as little as £10 into the start-ups. In the first 18 months since its launch in July 2012, Seedrs collected more than €6.8 million through 56 funded campaigns and counted more than 29,000 users.

3. In particular, the Seed Enterprise Investment Scheme (SEIS) launched by the UK government in April 2012.

REFERENCES

About the authors

Related content

From start-up to scale-up: examining public policies for the financing of high-growth ventures

What are the challenges of financing scale-ups, and how can long-term public policies support the creation of a better scale-up environment?

Innovation and sustainability of European healthcare systems

The EU health sector represents 10% of GDP, 15% of public expenditure and 8% of the workforce, and has high potential for innovation and growth. Impro

The comparison between the European and American innovation systems is hardly encouraging for Europe

Promoting STEM skills: a brief assessment of French individual learning accounts

French ILA successfully promotes basic digital skills but falls short of fostering more advanced capabilities.