Europhoria once again

The Europhoria before the crisis was due to a collective failure to see the looming crisis. The reaction once the crisis started was over-the-top and

Europhoria was rampant in the euro’s first decade. Just before the onset of the crisis, the yields paid by the soon-to-be distressed Greek, Irish, and Portuguese sovereigns were almost indistinguishable from the yields paid by the German sovereign. Then it all flipped. At the height of the crisis, in mid-2011, the premium (risk spread) over German yields paid by the distressed sovereigns was above 10 percentage points, and the spreads paid by Spain and Italy threatened to run out of control until the September 2012. Since then, there has been another flip. Europhoria has returned. Spreads have compressed again. And while they are larger than just before the crisis, with interest rate levels generally lower, the yields paid are near historical lows.

One perspective is to blame myopic markets. Acting as a herd, market participants have been a source of instability. The Europhoria before the crisis was due to a collective failure to see the looming crisis. The reaction once the crisis started was over-the-top and risked pushing otherwise-solvent sovereigns into a self-fulfilling prophecy of distress. Should we then view the recent fall in spreads and yields as a sign of confidence, as some policymakers are doing, or as another overreaction?

An alternative perspective is that the markets get it right: they do not overreact, they merely respond to the incentives set by the policy framework. The pre-crisis yield compression was fostered by a widespread belief that, despite protestations to the contrary, private creditors would be protected. When growth plummeted and debt-ratios skyrocketed, the commitment to protect creditors was discounted, and risk premiums rose. But following a set of new policy initiatives, the commitment to bailout has been bolstered and markets have calmed down. Private creditors to sovereigns have, in effect, been promised that, barring exceptional circumstances, they have no reason to fear a default.

This note traces the evolution of the new bailout policy. It warns that we should not be surprised if markets flip again. The new commitment to impose no losses on private creditors comes at a time when debt ratios are high and still rising. Economic growth is likely to remain weak. The bailout commitment has not been accompanied by a pooling of sizeable, centralized fiscal resources. Instead, the policy such as it is, offers the promise of official lending supplemented by good fiscal behavior. How credible can this commitment be?

To the contrary, the new bailout safeguard comes with its own fragility. The use of official lending (or purchase of sovereign bonds) implies that sovereign debt levels will not be reduced. Instead, official lenders will—in principle, temporarily—take on some of the repayment risk. Where the distressed sovereign is insolvent, the risks borne by the official lenders will be significant: the process of forgiveness-in-driblets of Greek official debt illustrates the pressures. If the distressed sovereign in the future is larger than Greece, the costs imposed on the official creditors would be correspondingly larger. Both the economic resources and the political willingness to deliver on this promise can thus come into question, not least because this policy has essentially arisen as a bureaucratic response without seeking a political mandate. Indeed, the reason for not seeking the political mandate was precisely that it would be rejected.

Preventing Default

Despite mounting evidence of unsustainability of Greek debt through 2010 and the first half of 2011, European and IMF policy on sovereign debt restructuring was to deny its need (Cottarelli et al. 2010). The fear was that restructuring Greek debt would precipitate Europe’s “Lehman” moment, triggering uncontrollable contagion and financial meltdown. But despite unprecedentedly-high official lending and deep fiscal austerity, private creditors were not reassured: by mid-2011, contagion threatened to spin out of control.

The lack of a let up in market pressure was a direct consequence of the policy pursued. In the countries that had received official financial support—Greece, Ireland, and Portugal—the official credit had been used to repay private creditors. But because this meant that public debt-to-GDP ratios had not fallen—indeed, they were rising relentlessly—the private creditors who had not yet been repaid now faced greater risks. The presumption was that the official debts would be repaid first, rendering private creditors “junior” to official creditors. The yields on Irish and Portuguese sovereign bonds rose rapidly. And, as panic spread, Italian sovereign yields crossed the 6 percent mark on July 18, 2011.

The clamor for action was palpable. Larry Summers (2011) was among the first to call for urgent action to deal with Europe’s “dangerous new phase.” He proposed reducing interest rates on the official debt of program countries (Greece, Ireland, and Portugal) to the level at which European authorities, using their collective credit, could borrow. He also emphasized that default on private debt should not be permitted because that could cause a systemic crisis. The International Monetary Fund (IMF, 2011) similarly called for enhancing official support to the beleaguered countries by bolstering official resources to recapitalize banks and by purchasing sovereign debt on the secondary market.

In their meeting on July 21, 2011, the Heads of State of the Euro Area member countries straddled two conflicting pressures (Council of the European Union, 2011). The fiction that Greece would fully repay its private creditors needed to be abandoned. And, for this reason, private creditors needed fresh, more credible assurances of protection. The Council resolved this dilemma by communicating that Greece was exceptional and that if other sovereign debts became unsustainable, the official component would be restructured.

The official restructuring began right away since it was clear that Greece, even with its privately-held debt restructured, could not possibly repay its official creditors on the terms originally agreed. Easing those terms was the leading edge to the new approach to protecting private creditors. The easier terms were extended to Ireland and Portugal. The interest rate on the debt owed to the official creditors was reduced from 5.5 to 3.5 percent and the repayment period extended from 7 to 15 years. By preemptively restructuring official debt owed by Ireland and Portugal, official creditors ceded their “seniority,” the claim to being paid before private creditors.

Some might argue that the more favorable terms on official loans were only a correction of excessively onerous terms earlier. That is a matter of judgment: the original terms were no more onerous than IMF terms. What we do know is that a signal was sent that where sovereign debt became unmanageable, private creditors would be bailed out until all other options were exhausted. The markets were right to read the signal that way, as subsequent official debt forgiveness on Greece confirmed.

How Official Debt Became Junior

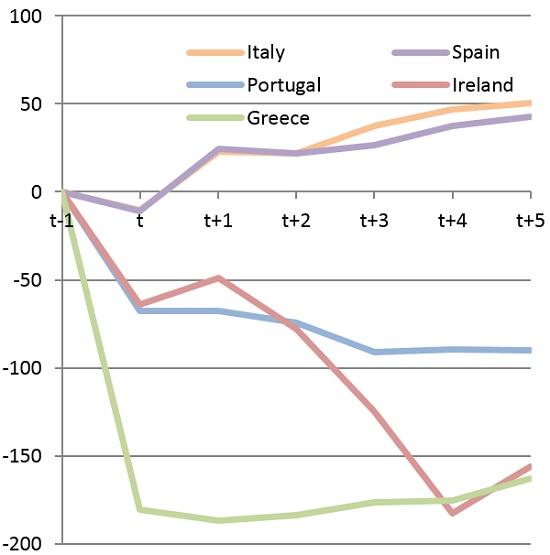

Figure 1 shows the changes in the momentum of sovereign risk spreads (the bond yields above the German sovereign yield) of the three program countries, as well as Italy and Spain. The figure plots the “abnormal” cumulative change in spread, defined as the change relative to the benchmark of persistence of the average change in spreads over the past 20 market days. The date “t-1” is July 21.

Figure 1: “Abnormal” Changes in Sovereign Spreads Following the July 21, 2011 Announcement of Easing of Terms on Official Loans (basis points)

Greek spreads fell sharply relative to their trend, but so did Portuguese and, importantly, Irish spreads. Five days after the announcement, Irish spreads were about 150 basis points lower than what they would have been if the pre-announcement trend had continued. Italian and Spanish spreads pulled back on the day after the announcement but crept back up in the days that followed.

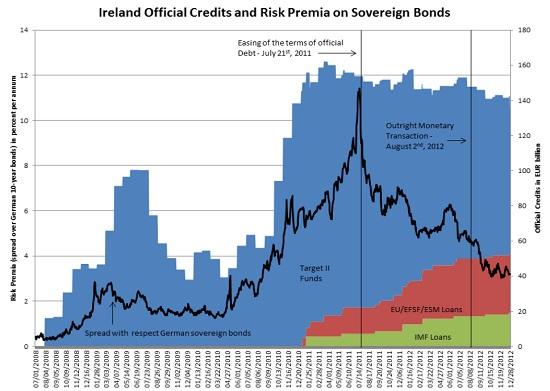

A closer look at Ireland clarifies the significance of the change in status of official debt (Figure 2). Until December 2010, the main source of Ireland’s official financing was the Eurosystem’s Target II mechanism, which replaced funds in the banking system when private creditors withdrew. These Eurosystem funds were de jure or de facto Irish government liabilities. The part through the Emergency Liquidity Assistance channel was an explicit contingent liability of the Irish sovereign; the government was more loosely on the hook for the rest. With the rise in these official Eurosystem obligations, which presumably took priority over repayment to its existing bondholders, spreads on Irish sovereign bonds rose relentlessly, especially after April 2010, as Steinkamp and Westermann (2013) also conclude. Thus, one set of private creditors—those who had loaned money to the banks—were being repaid with official credit, another set—private creditors to the sovereign—were apparently being pushed lower in the hierarchy of repayments.

Figure 2: Irish Sovereign Spread Movements around July 21, 2011 (percentages)

In December 2010, official credit became available through the European-IMF program. And, although the overall official credit levels did not rise noticeably, the more established seniority of the IMF and the claimed seniority of official European credit continued to push spreads up.

Irish spreads started falling on July 18th, the day the drumbeat of calls for official debt relief began. News reports suggest that Franklin Templeton began buying Irish sovereign debt around this time (Walsh, 2012). The expectation that interest rates on Irish official credit would be lowered and the maturities would be extended was validated on July 21st. From that moment, Irish spreads were set on a strong downward course. Over the next year, the Target II balances to the Eurosystem were drawn down while the European official credits steadily increased. The fall in Irish spreads and the rise in official European credits match strikingly. Since the signal was that the terms on these new official credits could be eased, the market was right in interpreting that its risk had been lowered. Subsequent actions validated that expectation as further concessions were made: in April 2013, the terms of repayment on Ireland’s Promissory notes were eased.

The ECB’s Outright Monetary Transactions

Notice that by August 2, 2012, the date on which the European Central Bank announced its Outright Monetary Transactions (OMT) Program, the fall in Irish spreads was a well-established tendency. The ECB’s deep pockets were required to tame the uncontrolled rise of Spanish and Italian spreads that once again threatened the integrity of the euro area.

Some have viewed the OMT as the instrument by which the ECB performs its lender-of-last-resort function. The OMT, however, is not a lender-of-last resort instrument. It is an IMF-style conditional lending program. The ECB promise is to support conditional lending to a particular country by the European Stability Mechanism. Forrest Capie (2002) writes that a lender-of-last resort’s function is “to provide the market with liquidity in times of need, and not to rescue individual institutions. Such rescues involve too much moral hazard.” International institutions, such as the IMF, he says, “are invariably focused on one “customer”– a country in difficulties – and so violate this rule of the lender-of-last-resort.”

For this reason, as Fisher (1999) and Rogoff (1999) emphasize, IMF lending must be accompanied by a clear and credible strategy for ensuring that private creditors share the burden. Else, private creditors would have every reason to lend with reckless abandon. Bottom line: insolvency requires default (or centralized fiscal resources and eurobonds) and illiquidity requires a lender-of-last resort. The OMT conflates solvency and liquidity. And, it thereby adds to the moral hazard being fostered by the policy of bailing out private creditors while easing the terms of official debt.

These tendencies are the consequence of recent European and IMF decisions to vigorously raise the thresholds of debt sustainability to avoid sovereign debt default. The presumption is that sovereign distress arises primarily from a liquidity crisis and the threat of financial contagion requires that private creditors remain whole. Schadler (2012) argues that this emerging practice violated IMF norms and the IMF’s participation in the Greek program on this basis set an unfortunate precedent. As it turned out, the costly delays in the Greek restructuring only served to illustrate that default on privately-held debts must be an integral element of crisis management. The IMF has since sought to retrace its steps and its current views on the matter diverge from the new European orthodoxy.

Moreover, unlike the ECB’s OMT, the IMF’s lending is still based on the presumption of preferred creditor status, to be repaid before all others—in the Greek case, the IMF has encouraged easing of terms charged by official European lenders while being itself repaid in full. In contrast, bond purchases under the OMT program would place the ECB on equal terms with private creditors, who are thereby being promised further protection. Altogether, the current rescue efforts are sowing the seeds of a future build-up of debt. As Buchheit and Gulati (2012) warn, the sense of calm and confidence can quickly turn. Speculators may “mercilessly” test the ECB’s resolve in buying unlimited quantities of a distressed sovereign’s bonds. Buchheit and Gulati also note that if the ECB ultimately were to achieve de facto seniority vis-à-vis private creditors, the market disruption could be even worse.

Conclusions

The emergency actions taken on July 21st brought the intended calm, although the OMT reinforcement was eventually required for Spain and Italy. The principle of “no bailout” was abandoned, fundamentally undermining the architecture of the euro area (Mody, 2013). The game plan now presumes that the scars of the recent crisis will induce prudent fiscal behavior and the ad hoc technical fixes will prevent the next threat from spiraling out of control. But this flies in the face of history. The lessons from a crisis are quickly erased and, as Rogoff (2002) has discussed in the context of the IMF, potentially open-ended official support is the touchstone of moral hazard.

Today, the economic conditions in the euro area are manifestly worse than before the crisis. The public debt-to-GDP ratios are much larger—and while the pace at which debt is increasing has slowed, debt ratios are projected to continue rising before a sustained decline begins. Moreover, growth prospects—especially of nominal GDP, the relevant measure for debt sustainability—are markedly weaker. Private balance sheets are also much more stressed.

Thus, a reading of the recent fall in risk spreads as a vote of confidence in the distressed economies relies on the assumption that they will thread the eye of the needle. But despite the brave talk, more relief on official Greek debt is imminent. Portugal may not be far behind, and the threat of Italy perpetually looms. Bondholders have come to expect that they will be bailed out and, as such, lending is virtually risk free. The authorities’ resolve to avoid default will continue to be tested. And with weaker economic conditions the next time around, the delays in facing reality could have far reaching costs.

References

Buchheit, Lee and Mitu Gulati, 2012, “The Eurozone Debt Crisis—the Options Now,” Electronic copy available at: http://ssrn.com/abstract=2158850.

Capie, Forrest, 2002, “Can there be an International Lender-of-Last-Resort?” International Finance 1(2): 311–325.

Cottarelli, Carlo, Lorenzo Forni, Jan Gottschalk, and Paolo Mauro, 2010, “Default in Today’s Advanced Economies: Unnecessary, Undesirable, and Unlikely,” Fiscal Affairs Department, International Monetary Fund, Washington D.C.

Council of the European Union, 2011, “Statement by the Heads of State or Government of the Euro Area and EU Institutions,” Brussels. http://www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/123978.pdf

Fischer, Stanley, 2009, “On the Need for an International Lender of Last Resort,” The Journal of Economic Perspectives, 13(4): 85-104.

International Monetary Fund, 2011, “IMF Executive Board Concludes Article IV Consultation on Euro Area Policies,” Public Information Notice (PIN) No. 11/91, July 19, 2011, http://www.imf.org/external/np/sec/pn/2011/pn1191.htm.

Mody, Ashoka, 2013, “Sovereign Debt and its Restructuring Framework in the Euro Area,” Oxford Review of Economic Policy 29(4): 715–744.

Rogoff, Kenneth, 1999, “International Institutions for Reducing Global Financial Instability,” The Journal of Economic Perspectives, 13(4): 21-42.

Rogoff, Kenneth, 2002, “Moral Hazard in IMF Loans: How Big a Concern,” Finance and Development, September 39(2).

Schadler, Susan, 2012, “Unsustainable Debt and the Political Economy of Lending: Constraining the IMF’s Role In Sovereign Debt Crises,” CIGI Paper 19, Center for International Global Innovation, Waterloo, Canada.

Steinkamp, Sven and Frank Westerman, 2013, “The role of creditor seniority in Europe’s sovereign debt crisis,” Osnabrück University & CESifo.

Summers, Lawrence, 2011, “Europe’s Dangerous New Phase,” July 18, http://blogs.reuters.com/lawrencesummers/2011/07/18/europes-dangerous-new-phase/.

Walsh, John, 2012, “Franklin Templeton investment puts government debt in spotlight,” The Irish Examiner, September 4, 2012, www.irishexaminer.com/business/franklin-templeton-investment-puts-government-debt-in-spotlight-206349.html.

Read more from Ashoka Mody on Italy