Juncker’s investment plan: No risk – no return

President Juncker has presented the key features of the European Commission’s plan to boost investment in the EU. In this blog post we review the most

Five, still undecided, points are key for the success of the plan:

- The small public funds should serve as a first loss guarantee;

- The project selection committee needs to be able to identify projects that would not have happened without the guarantee;

- By choosing more risky projects, the committee would increase the likelihood that the guarantee actually contributes to additional investment instead of just funding investment which would have taken place anyway;

- The political economy of project selection is difficult. For true public infrastructure projects, public funds should be used directly;

- investment-friendly regulation and structural reforms can substantially increase private investment without public guarantee and are not subject to selection problems.

How much will/should be invested in the end?

The Juncker plan aims to increase private investment by approximatively €100bn per year. While it is difficult to estimate the precise shortfall in investment, the investment gap could actually be much larger than that. Our previous blog post suggests that yearly investment in the EU is currently around €280bn (or €170bn excluding construction) below its long-term trend.

In the end, the European Commission’s (EC) plan involves only €21bn of public money, which the EC aims to leverage by a factor of 15 so that €315bn of private investment is generated. The public resources come partly from a reshuffling of the EU budget (€16bn) and partly from the EIB (€5bn). The EC also encourages member states to provide additional funds by proposing to “treat favourably” such contribution in its assessment of the national budget under the Stability and Growth Pact.

What is the main idea behind the EFSI?

The exact structure of the new European Fund for Strategic Investment (EFSI) is not yet totally clear. The documents released on Wednesday suggest that the public money will essentially be used as a contribution to absorb risk. By taking on more risk on the public part of the investment, the EFSI aims to attract private investors. However, it is unclear, how much risk the public sector is ready to accept. In our understanding, the Commission does not think that the €21bn will be actually spent so that in fact the risk bearing capacity is less than €21bn. Nevertheless, the hope is that this risk absorption by the public sector would attract significant private investment.

It is a big question, whether a leverage factor of 15 is feasible. The EIB often leverages itself by a factor of 6 before attracting enough private investors to co-fund its projects to increase investment by a factor of 3 leading to an overall multiplier of 18. Is this a feasible proposition for the new Juncker investment plan? And will the plan really generate €315bn in new investments instead of replacing the financing structure of already planned investment projects?

The idea behind the European Commission’s plan is to use public money as a buffer to absorb some of the potential losses of the projects. This way, some investment previously considered not lucrative enough and too risky might become profitable to private investors. The first and undecided issue is whether the public resources will really serve as a first loss guarantee or whether they are only part of the risk sharing.

Second, if it is to serve as a first loss tranche, then the question is whether a 6.7% (i.e. 1/15) guarantee on a project will be enough of an incentive to attract fresh investors. A 6.7% first loss guarantee can significantly improve the expected return of private investors.

The gains from benefitting from a loss guarantee in a world where there is no risk aversion can be simply written as:

1 + r* = (1 + ri)(1 - πi) + (1 + ri) πi (1 - τi)

where r* is the risk free interest rate (the yield on German 10-year bund, currently at 0.7%), ri is the return of the newly planned investment project, πi is the probability of default of project i, τi is the expected percentage that will be lost on investment in project i in case of default. This equation holds because investors should be indifferent from holding a safe asset or a risky asset with a higher interest rate compensating for the risk.

In the case in which there is a guarantee covering partly potential losses, the equation becomes:

1 + r* = (1 + rig)(1 - πi) + (1 + rig) πi (1 - max(τi - g,0))

where g is the reduction of the loss because of the guarantee and rig is the interest of the investment project when a guarantee is given. Solving the two equations for ri respectively rig and taking the differences between the two implied interest rates gives us the reduction of the return rate asked by investors if there exists a guarantee:

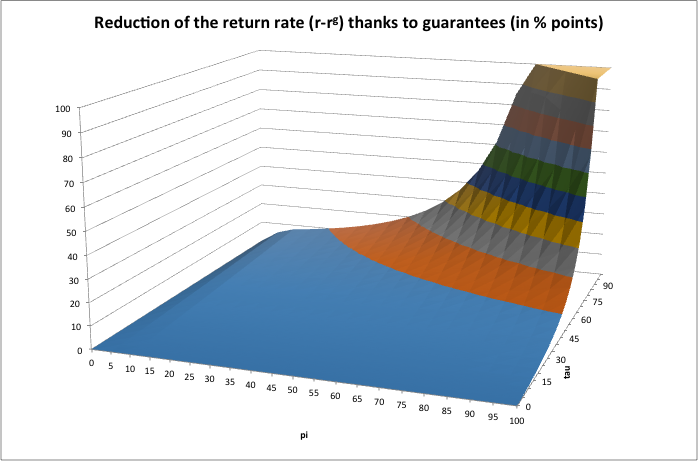

ri - rig = (1 + r*) / (1 - πiτi) - (1 + r*) / (1 - πi . max (τi - g, 0))

For instance if a project has a default probability of 10% and an expected loss of 60% in case of default, the guarantee is equivalent to a reduction of 75 basis points in the return rate demanded by investors to participate to this risky project instead of investing in safe assets. The chart below depicts the gains in terms of interest rates for all possible values of τi and πi. Basically, it shows that the more risky the projects are (with high values of τi and πi) the more the guarantee will reduce the additional return an investor demands to invest in it instead of investing in the safe asset.

How many new investments can be triggered by this scheme depends therefore on the ability of the selection committee to identify new projects that would not have happened without the subsidy. Our little analysis suggests that the EFSI should in fact target very risky projects because they are probably the ones that are not financed at the moment but also because they are the ones on which a guarantee should have a larger effect

How to structure the governance of this scheme?

A risk with the scheme is that it may not increase the total amount of private investment in the EU but rather simply provide a windfall gain to those already planning to invest. The governance of the EFSI is therefore of central importance. How can one ensure that new projects get selected instead of seeing a crowding out of existing private projects? The key will be that the selection committee is able to identify projects that add to existing investment. This is a big challenge for economic policy making and experience shows that such publicly run committees often select politically motivated projects rather than projects that add to existing ones. One criterion that could be used is the fact that a project is risky and therefore there is no private appetite to do it.

More fundamentally, there is the question as regards the political economy of project selection. The more projects are of a private sector nature, the more questionable it becomes whether the public sector can select the right projects and how the subsidies would represent competitive distortions. Conversely, for pure public good investment, countries with fiscal space could use their ability to borrow to invest in public infrastructure. This should generate also some private investment to the extent that public investment is productive.

In addition, the public sector can relatively easily generate private investment by offering the right regulatory framework and other framework conditions. For example, it is not difficult to find private investors to fund useful highways when the process of getting the necessary permits is facilitated and the right to collect road tolls granted. Initiatives to harmonize regulation and create a single market for services should also provide for substantial incentives for new investment.

The EC plans to invest in two types of projects at the moment. First, it intends to invest in SMEs and mid cap companies through loans but also through equity and venture capital. Second, the EC wants to target “strategic” long-term investment with a particular focus on energy, transport, broadband, R&D and education. The fact that most of these strategic investments are at least partly public infrastructures that are either profitable because they will generate their own revenue streams in the future or that may not have revenue stream but that will raise European potential growth also raises some important questions. If these projects are really profitable, given the current low interest rates it would be legitimate to have proper public investment financed by debt that will pay for itself in the long run.

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

EU savers need a single-market place to invest

Proposals to leverage the single market to boost retail investment could lead to a product citizens will trust

Key factors likely to shape the EU’s trade agenda in the next five-year term

Using the financial system to enforce export controls

Russian imports of battlefield goods that are subject to export controls, including from Western producers, have surged since mid-2022