A tale of floods and dams

A lot of debate has recently focused on the management of the fiscal crisis in Greece and whether or not the speed of adjustment has been too fast or

“Fortune can be compared to a river that floods, destroying everything in its way. But when the weather is good, people can prepare dams and dikes to control the flood. If Italy [read Greece] had such preparations, she would not have suffered so much in the present floods.”

Machiavelli – The Prince

A lot of debate has recently focused on the management of the fiscal crisis in Greece and whether or not the speed of adjustment has been too fast or too slow (see for example Anders Aslund, Simon Wren-Lewis or this VoxEu piece by the German Sachverständigenrat). In this blog I want to focus instead on the pre-crisis management before turning to the crisis period. I take the road of comparing Greece with its immediate neighbour Bulgaria. I start from their comparable current account developments, which led to crisis in one country but not in the other. The question is why this is the case. Like Machiavelli in his Prince, I would argue that once the flood is coming, it is very difficult to stop it. Once the flood has arrived, the debate really becomes one of second and third best alternatives, so ideally policy makers should build the necessary dams in advance.

Greece and Bulgaria share many similarities. Bulgaria has a fixed exchange rate with the euro thanks to a currency board which has been in place since 1997, while Greece entered the fixed exchange rate mechanism in 1999 to join the euro in 2001. Both countries are quite similar in terms of institutional quality and the structural features of their economies. In terms of the World Bank “Ease of Doing Business” indicator, Greece is ranked 61st while Bulgaria is ranked 38th (and Greece’s ranking was much worse at the beginning of the programme). Both countries are at the bottom of the European PISA education rankings, and public perceptions of corruption are at similar levels according to the World Governance Indicators. Both countries thus have a fixed exchange rate (Greece being in a monetary union) and weak institutions. Greece is in a severe crisis, while Bulgaria has not had a major crisis.

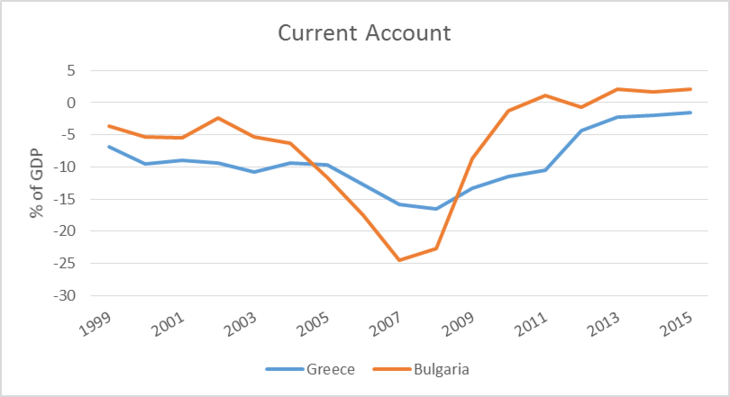

Large current account deficits

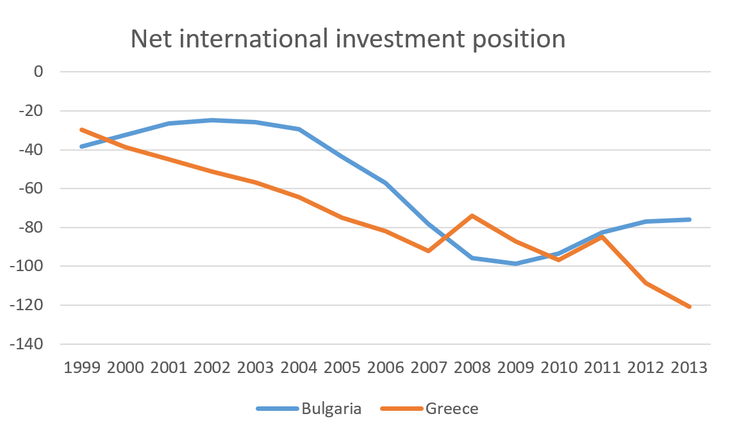

Bulgaria and Greece both ran significant current account deficits before the crisis erupted. In fact, Bulgaria’s current account deficit was more significant than Greece’s right before the onset of the crisis. The deterioration in the net external liabilities of both countries was quite comparable up until this time. Since then, the Bulgarian net external liabilities decreased as a percentage of GDP while in the case of Greece net external liabilities have increased to a staggering 120% of GDP.

Source: AMECO February 2015

Source: AMECO February 2015

So looking at the external accounts superficially would suggest that both Greece and Bulgaria could have had a severe balance of payments crisis leading to a financial assistance programme combined with GDP declines and severe adjustment problems.

So are the two current account deficits comparable? In fact, they are not. In Bulgaria, foreign direct investment inflows drove the current account deficits. As an economy that had just left the communist period behind and had a low capital stock, investment opportunities were still significant despite the weak institutions. In contrast, in Greece, reckless borrowing by the government was the main driver of capital imports. FDI inflows were negligible, probably reflecting the already relatively high capital levels and the weak institutions, including in the area of property rights.

Different fiscal starting positions

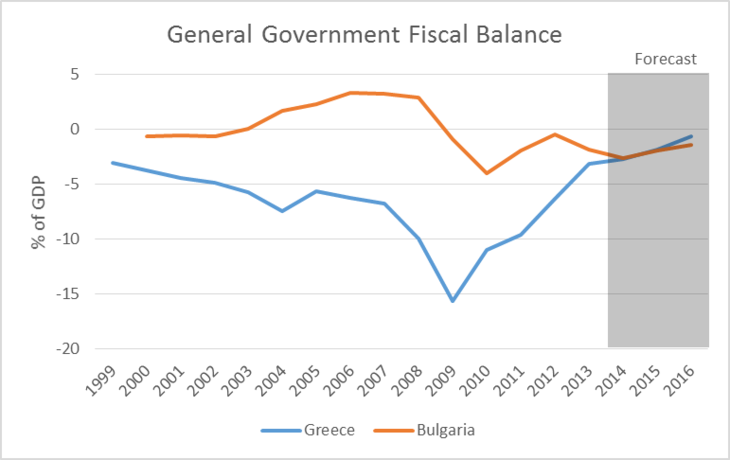

Bulgaria ran an average fiscal surplus of 1.3% during 2000-2008 while Greece ran a deficit of 6.1%. Bulgaria thus exercised fiscal prudence before the crisis. In contrast, the Greek fiscal situation deteriorated throughout the good years of 1999-2008. These high deficits were not put to good use, but rather gave support to a weak state suffering from corruption and bad governance.

Source: IMF World Economic Outlook October 2014, Eurostat data not available for Greece before 2006.

Accordingly, the fiscal management during the crisis was different. When the crisis hit, both countries experienced a significant deterioration of their fiscal balances. In 2009, Greece increased its deficit by 5.7% while Bulgaria increased it by 3.8%, followed by another stimulus of 3.1% in 2010, so a cumulated 6.9%. Bulgaria then adjusted its fiscal deficit from 4% in 2010 to close to zero (0.5%) in 2012, while Greece had to consolidate from 15.6% in 2009 to a forecast 2.7% in 2014 to achieve a primary balance. Both countries enacted a similar fiscal stimulus when the crisis hit, yet Greece had to do a much more significant fiscal adjustment because its starting position was so much worse.

What is the counterfactual of crisis management?

Could the fiscal adjustment of 15% have been done in a less painful way? Simon Wren-Lewis replies to a VoxEU piece by the Sachverständigenrat and argues that the real issue has been that fiscal consolidation has been too quick. He does admit, however, that “In a monetary union … a period of unemployment is inevitable to restore competitiveness.” The problem with both, Wren-Lewis and the Sachverständigenrat is that they fail to specify a proper counterfactual.

Had the fiscal adjustment been lower, how much larger would the size of the financial assistance programme had to have been? Would it really have been possible to agree on a programme even larger than the current one that was already more than 100% of GDP? Would it have been possible to agree on transfers? Would it really have been possible to get a much larger contribution to the fiscal adjustment from earlier debt restructuring?

I doubt that a positive answer to any of the questions above would have been possible politically. The most realistic option would perhaps have been an earlier debt restructuring. Looking back at the debates in which I had been an advocate of earlier debt restructuring, I would argue that one could have gained some €20-30 billion, but the number just reflects a personal assessment of the politics at the time. Certainly the IMF and Germany could have countered the opposition (e.g. here) more forcefully. But the opposition to debt restructuring was - rightly or wrongly - huge. With €20-30 billion, one could have allowed delaying fiscal consolidation by perhaps 2-3 years. The Wren-Lewis piece and the Sachverständigenrat piece also fail to contemplate the impact of high interest rates and the associated confidence effects, a point that Aslund in turn greatly emphasizes. Even in a counterfactual scenario of fiscal adjustment delayed by 2 years, the collapse of GDP would probably have remained substantial due to the prohibitive funding conditions.

Credibility in financial markets

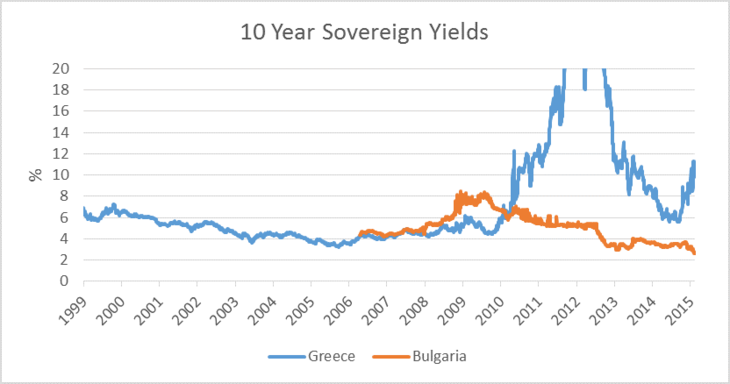

Differences in fiscal management and the substantial political turmoil, associated exit fears etc. led to a substantial difference in credibility in financial markets and Greece suffered greatly from this. Yields on Bulgarian debt have been consistently below Greek yields since the beginning of the crisis. Arguably, the higher yields driven by the lack of Greek credibility were an important factor behind the collapse of Greek GDP. Think of increased spreads like an increase in the central bank interest rate, with the corresponding negative effects on economic performance. It was therefore good news that these spreads came down substantially before the election of the new Greek government. The more recent increase in interest rates and the corresponding loss in confidence makes me pessimistic with regard to the overall economic performance of the Greek economy in 2015. The effect of the reduced austerity may be more than offset by the interest rate hike and the worsening investment climate.

Source: Benchmark Yields from Thomson Reuters

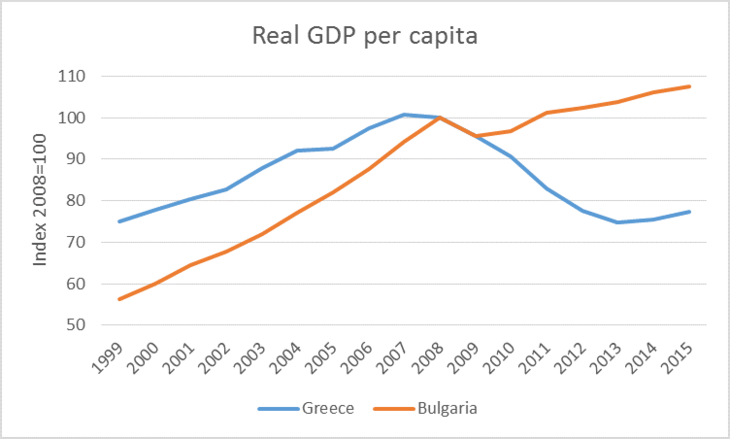

Overall, differences in particular in the pre-crisis fiscal management in particular left their mark on GDP: Greece’s GDP per capita is now back to where it was in 1999 after a 25% collapse since the beginning of the crisis. In contrast, Bulgaria now stands some 8 percentage points above the 2008 level and its income per capita has doubled since 1999. Greece would have hugely benefited from better fiscal management prior to the crisis, as also argued by Martin and Philippon (2014). It is easy to postulate a better crisis management but much more difficult to propose a credible and realistic counterfactual. Containing a crisis when the flood has arrived is always difficult.

Source: AMECO February 2015

Readers will tell me that things are not great in Bulgaria and that growth is disappointing. This is true, but at least per capita growth is positive. Further policy measures could focus on investment that increases economy-wide productivity. In contrast, pet-projects driven by corrupted institutions and funded by deficits need to be avoided. This is a significant challenge, which may explain why Bulgarian citizens have been sceptical about recent government proposals to increase the deficit.

Lessons

Let me draw a number of key lessons:

1) Greek fiscal imprudence prior to the crisis proved to be costly. Greece entered the crisis with a deficit that was already at an unsustainable level. The necessary adjustment was huge and had a substantial impact on unemployment and GDP. It is difficult to quantify how much a slower fiscal adjustment would have helped to restrain the decline in GDP. Arguably, to make the adjustment much slower one would have needed either politically unrealistic transfers or a debt restructuring of perhaps unrealistic size. The real issue is thus that it is difficult to build dams when the flood is coming. Prudent fiscal policy is essential in good times.

2) Large current account deficits are not a problem per se. Large net external liabilities do not necessarily lead to a sudden stop and exchange rate problems, as long as it reflects prior productive capital inflows. In contrast, if capital inflows are driven by reckless fiscal policy (or unsustainable private sector housing booms such as in Ireland and Spain) that are spent unproductively in a weak state, a balance of payments crisis can be the result. Substantial down-hill capital flows can work but only if put to a good use.

3) One can speculate as to whether the monetary union provided Greece with an incentive to run more irresponsible fiscal policy than Bulgaria, which was always aware that the currency board would only hold if the country was credible. This view would imply that Greece was of the opinion that being in the euro area removed the budget constraint and made transfers possible. This view would also imply that financial markets did not believe in the no-bail-out clause. Nevertheless, the reason for earlier fiscal irresponsibility is probably also related to the Greek political system, as Greece has a long history of high public deficits and to the failures of European fiscal surveillance. After entering the euro, the system did not realize that in a monetary union monetary financing and devaluation are not an option anymore.

4) Comparable fiscal consolidations in other countries proved to be less damaging than in Greece. The real lesson to draw is not to increase the speed of fiscal consolidation during adjustment. Instead, when institutions are weak you have to be particularly prudent in your macroeconomic management before a crisis hits you. Weak institutions mean lower potential growth and restrict the capacity to deal with crises. This is the case inside a monetary union as it is the case for a country with a currency peg like Bulgaria. It is a tale of fiscal prudence in good times.

In conclusion, it will come as no surprise that I believe that a solution to the current impasse will be difficult to find. The Eurogroup rightly agreed to Greece running lower primary surpluses in 2015, and they should ask for lower primary surpluses than they have before for the future years as well. In my calculations, a primary surplus of 2.5% is compatible with a declining debt ratio under a moderate growth scenario. A solution also needs to be found for the debt level. While the interest burden on the debt is negligible, the high levels do undermine trust of international investors and are a constant source of political tensions. Indexing debt to future GDP developments would bring trust and stability. All of these issues are painful in any creditor-debtor relation. They are particularly painful in a monetary union as they put to the test the credibility of its rules.

Excellent research assistance by Alvaro Leandro is gratefully acknowledged as are helpful comments by Gregory Claeys, Zsolt Darvas, Ashoka Mody, Andre Sapir on earlier versions of this blog.

About the authors

Related content

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and

What will it cost the European Union to pay its economic recovery debt?

Servicing the EU debt until 2058 seems feasible, despite increased borrowing costs, but member countries must make choices about budget funding

Discretion lets Croatia in but leaves Bulgaria out of the euro area in 2023

Crucial decisions about whether a country can join the euro area depend on questionable discretionary decisions.

With or without you: are central European countries ready for the euro?

The debate on euro adoption by central European EU countries has intensified in the last years. In this Policy Contribution the author does not review