Restructuring in the US currency union

On June 28, the governor of the Commonwealth territory announced that it would not be able to repay its debt. Puerto Rico has since asked Congress to

What’s at stake: On June 28, the governor of the Commonwealth territory announced that it would not be able to repay its debt. Puerto Rico has since asked Congress to change the law to make the tools that U.S. municipalities can use to restructure their debt through Chapter 9 available to its territory.

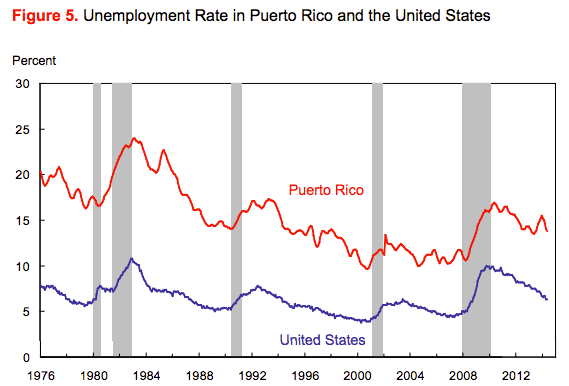

Barry Eichengreen writes that the United States now has its own version of Greece in Puerto Rico. The territory's debts are unsustainable. Public employment and pensions are swollen. Work in the underground economy, where taxes are evaded, is rife. Modern infrastructure is lacking. The commonwealth exports little for an economy of its size. Many of the best and brightest have decamped in search of better opportunities.

Source: NY Fed

Max Ehrenfreund writes that the Commonwealth of Puerto Rico is not a state, but it's been under the control of the United States since the Spanish-American war in 1898. Nick Timiraos writes that Puerto Rico’s problems date to the end of the Cold War, when the U.S. began closing military bases on the island, whose residents have American citizenship but don’t pay federal tax on their local income. The expiration of corporate tax breaks in 2006 prompted an exodus of businesses, throwing the island into a recession. Matt O’Brien writes that Puerto Rico was soon stuck in a vicious circle where the bad economy made people move to the mainland in search of work, the shrinking population left the government with a shrinking tax base to pay for the same amount of spending, and, after borrowing to cover this up, they eventually had to try to close their budget hole with austerity measures—which only made the economy even worse and made even more people leave.

Sovereign default, exit fears and sideshows

Barry Eichengreen writes that, in contrast with Europe, Puerto Rico will be at most a sideshow. One should not underestimate the ability of US politicians to get it wrong. But Puerto Rico will remain only a minor distraction. The US Congress will pass legislation giving Puerto Rico access to American bankruptcy courts. Its debt will be restructured, and all those reckless enough to have lent it money will see their claims radically written down. Once the island's government, relieved of its crushing debt burden, responds with reforms, the US will provide further aid.

Gillian Tett writes that, in theory, as Lawrence Summers says, one resolution would be for the International Monetary Fund to intervene. But it will not, since Puerto Rico is not a sovereign state. Washington could play an IMF-style role if it chose, since Puerto Rico, as a territory, is part of the federal system. But the Obama administration has made it clear it does not wish to intervene. That suggests that the least bad remaining option is to find a third party legal referee to oversee an economic plan that forces the creditors into a compromise. America does have one existing model for this: a Chapter 9 framework that offers bankruptcy protection for public entities. This was used to restructure Detroit’s $18bn debt pile. But since Puerto Rico is a territory, not a city, it is not allowed to use Chapter 9 without a change in US law.

Matt O’Brien writes that Greece and Puerto Rico both borrowed more than they could pay back, both are stuck in deep recessions, but both aren't at risk of getting forced out of their currency unions. Only Greece is. That's because the euro zone doesn't have a banking union yet, so a debt crisis can morph into a financial crisis and then a currency crisis. John Cochrane writes that in a currency union, sovereign debt must be able to default, without shutting down the banks, just as corporations default.

The Krueger report’s mix of reforms, fiscal adjustment and restructuring

Robin Wigglesworth writes that the Krueger report suggests even restructuring the “General Obligation” debt of the Puerto Rican government itself, and no US state has restructured in living memory. The island’s constitution enshrines creditors’ rights to be paid even ahead of pensioners, and hedge funds that make up a big part of Puerto Rico’s bondholders are not going to roll over.

Anne Krueger, Ranjit Teja and Andrew Wolfe write that Puerto Rico needs a comprehensive approach as its problems are interdependent. Fiscal adjustment alone might strengthen confidence in long-term public finances and thereby support demand. But too much fiscal tightening could also depress demand in the near-term and would do nothing to address the supply side problems at the root of Puerto Rico’s growth problem. Similarly, structural reforms alone would still leave large fiscal financing gaps. Hence the need for complementary debt restructuring to avoid an economically harsh and politically unviable cut in the fiscal deficit. A combination of structural reforms, fiscal adjustment, and debt restructuring ensures that all problems are addressed. And, importantly, it shares the costs and benefits of adjustment across all stakeholders.

Anne Krueger, Ranjit Teja and Andrew Wolfe write that debt relief could be obtained through a voluntary exchange of old bonds for new ones with a later/lower debt service profile. To agree to it, bondholders would need to be convinced that the specific reforms on the table are indeed a best use of debt relief, and that – by keeping the government functioning as it phases in organizationally and politically difficult measures – the reform program will increase the expected value of their claims. Negotiations with creditors will doubtlessly be challenging: there is no US precedent for anything of this scale and scope, and there is the added complication of extensive pledging of specific revenue streams to specific debts. But difficult or not, the projections are clear that the issue can no longer be avoided.

Restructuring idiosyncrasies

Nick Timiraos writes that as a commonwealth, it lacks the tools available to U.S. municipalities to restructure their debt through Chapter 9 of the bankruptcy code. A bill introduced in Congress last year would grant the island the ability to allow its public authorities to access Chapter 9 protections, but the bill hasn’t moved anywhere amid resistance from some creditors and conservative Republican lawmakers.

Dara Lind writes that, in 2014, the government of Puerto Rico passed a law allowing public corporations to declare bankruptcy. Creditors were not pleased, and earlier this year, a judge struck down the law because it was trumped by federal law. So without action from Congress, Puerto Rico could end up in a messy situation where individual creditors could sue to get their money back, which could prevent Puerto Rican public sector employees from getting their paychecks. Max Ehrenfreund writes that the laws determining who would get paid first if the island goes bankrupt are ambiguous. That $72 billion includes debts owed to retirees with public pensions as well as to firms on Wall Street that have loaned their client's money to the commonwealth.

Gillian Tett writes that the island’s debt structure is staggeringly complex, since the bonds have been issued by numerous different entities, with varying types of guarantees. These creditors show no desire to co-ordinate; instead, they are threatening to sue each other and the island. Thus the nightmare scenario that now haunts Puerto Rico is not so much that of Greece but Argentina: years of legal limbo, shut out of the capital markets.