Has globalisation 'peaked'? Trade and GDP growth in the post-crisis context

Is the ‘Global Trade Slowdown’ a signal that globalisation has structurally 'peaked', and thus we should expect a stagnation of trade growth also in t

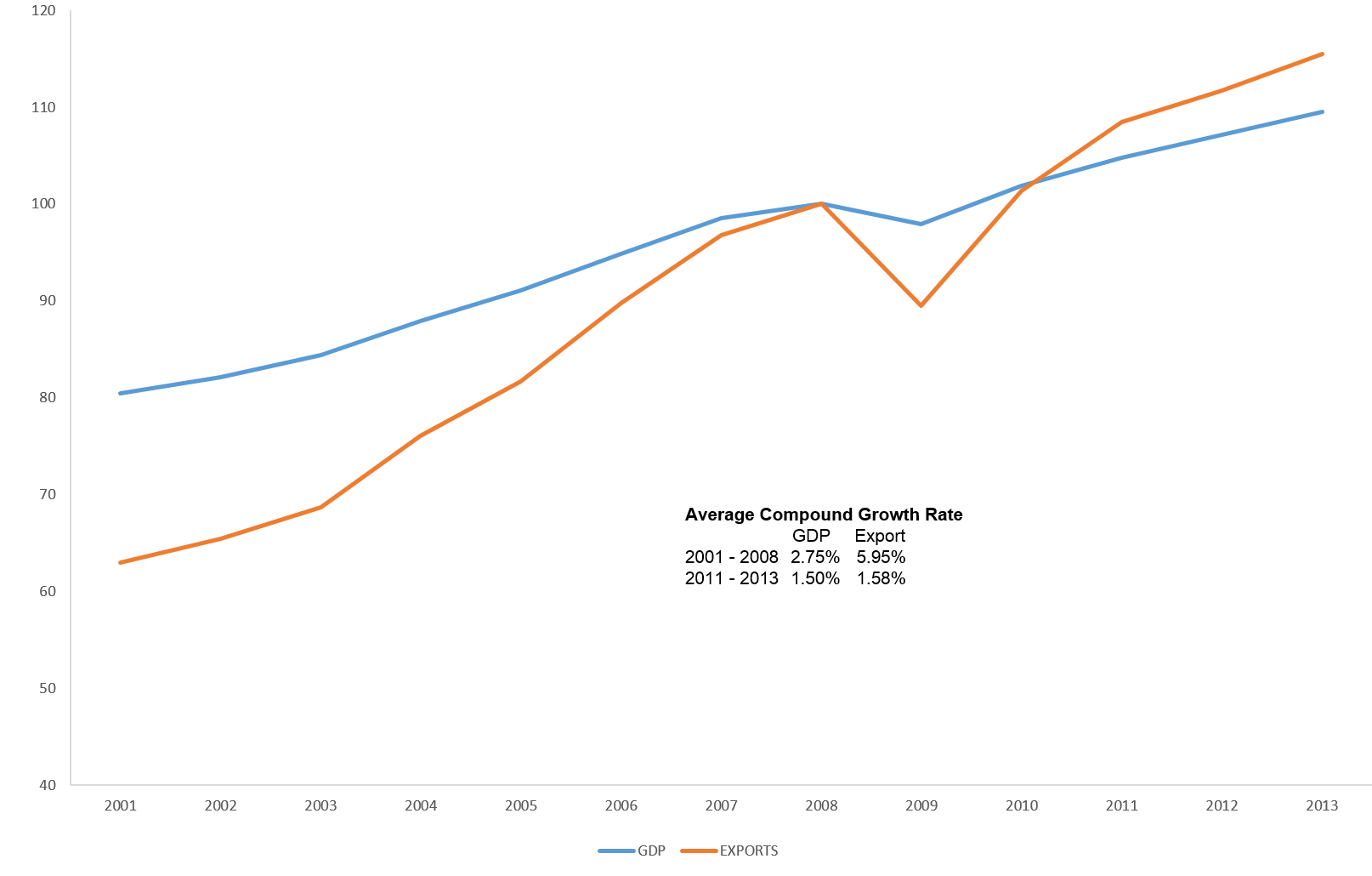

A decades-old rule of thumb has it that trade grows faster than GDP, mainly as a result of globalisation. And yet, since the crisis-induced ‘Great Trade Collapse’ of 2008/2009, followed by a brisk but brief recovery in 2010, international trade has been growing roughly in line with world GDP. This pace is markedly slower than in the previous fifteen years, in which yearly trade growth at times even doubled global GDP growth (Figure 1). In addition, the last spell of data shows that trade might have slowed down even more during the first part of 2015.

Is this ‘Global Trade Slowdown’ a signal that globalisation has structurally 'peaked', and thus we should expect a stagnation of trade growth also in the future? Or is the slowdown just the result of cyclical drivers, e.g. the fragile European recovery and slower growth in China?

Figure 1: World GDP and exports in volumes - index 2008=100

{kind=link}

Source: World Bank – World Development Indicators

The ongoing debate, summarized in a previous Bruegel’s blogpost, acknowledges the fact that, besides the well-known cyclical explanations, a more structural reason behind the trade slowdown might be associated to the role of Global Value Chains (GVCs), i.e. the break-up of production processes into ever-narrower discreet activities and tasks, combined with the international dispersion of these activities and tasks across countries.

The development of GVCs has been one of the key factors behind the fast trade growth recorded since the 90s, and it has somehow changed the very nature of international trade. In fact, trade has increasingly involved multiple flows of inputs and semi-finished products across borders, as different production steps were moved to different countries. This in turn has led to trade growing much faster than GDP, also as a result of the so-called ‘double counting’ in gross trade figures. This GVCs expansion process seems to have now levelled off, especially for China and the US, leading to a structural reduction in the elasticity of trade with respect to GDP in the 2000s, starting already before the crisis.

Still, in this blog-post we show that cyclical factors can be at play also in the adjustment of global value chains to the post-crisis context. In other words, there is reason to believe that some components of trade, as generated by the fragmentation of production across borders, have yet to fully overcome the trade collapse shock of 2008/09 (potentially amplified by specific events such as the Japanese earthquake of 2011). Therefore, even within a GVCs-related explanation of the trade slowdown, we risk to be identifying as 'structural' (and thus permanent) a phenomenon that might still reflect cyclical factors, and may thus partly revert back in the near future.

The empirical analysis

In a world characterized by global value chains, gross exports from country A to country B do not only include domestic value added generated in A, but also foreign value added generated in any other country (C, D, E…). Being able to decompose gross export flows in their different value added components is key for our analysis, as we want to understand how each component of trade has been behaving over the crisis. For doing so, we exploit a new dataset by Wang et al. (2013) based on WIOD data, covering 40 countries between 1995 and 2011. This allows us to decompose each trade flow in several value added terms. In particular, we focus on the following three main components:

- Domestic value added (DVA): it is the value added generated in the exporting home country which is finally absorbed abroad. This accounts on average for 77% of gross exports.

- Foreign value added (FVA): it is the foreign value added embodied in domestic exports, both in final goods and in intermediates. This makes up on average 16% of gross exports.

- Pure double counting (PDC): it is the portion of gross exports accounted for by intermediates crossing borders several times before being finally absorbed. PDC may include value added generated both in the home country and abroad, and can be considered as a sort of indicator for the extent of production sharing across countries (Wang et al., 2013). PDC accounts on average for 6% of gross exports.[1]

FVA and PDC are the two components of exports most directly related to the participation of a country in global value chains, while DVA represents somehow a more traditional component of exports. Investigating the dynamics of these different terms separately allows us to shed new light on the role of GVCs with respect to the trade collapse and the subsequent slowdown.

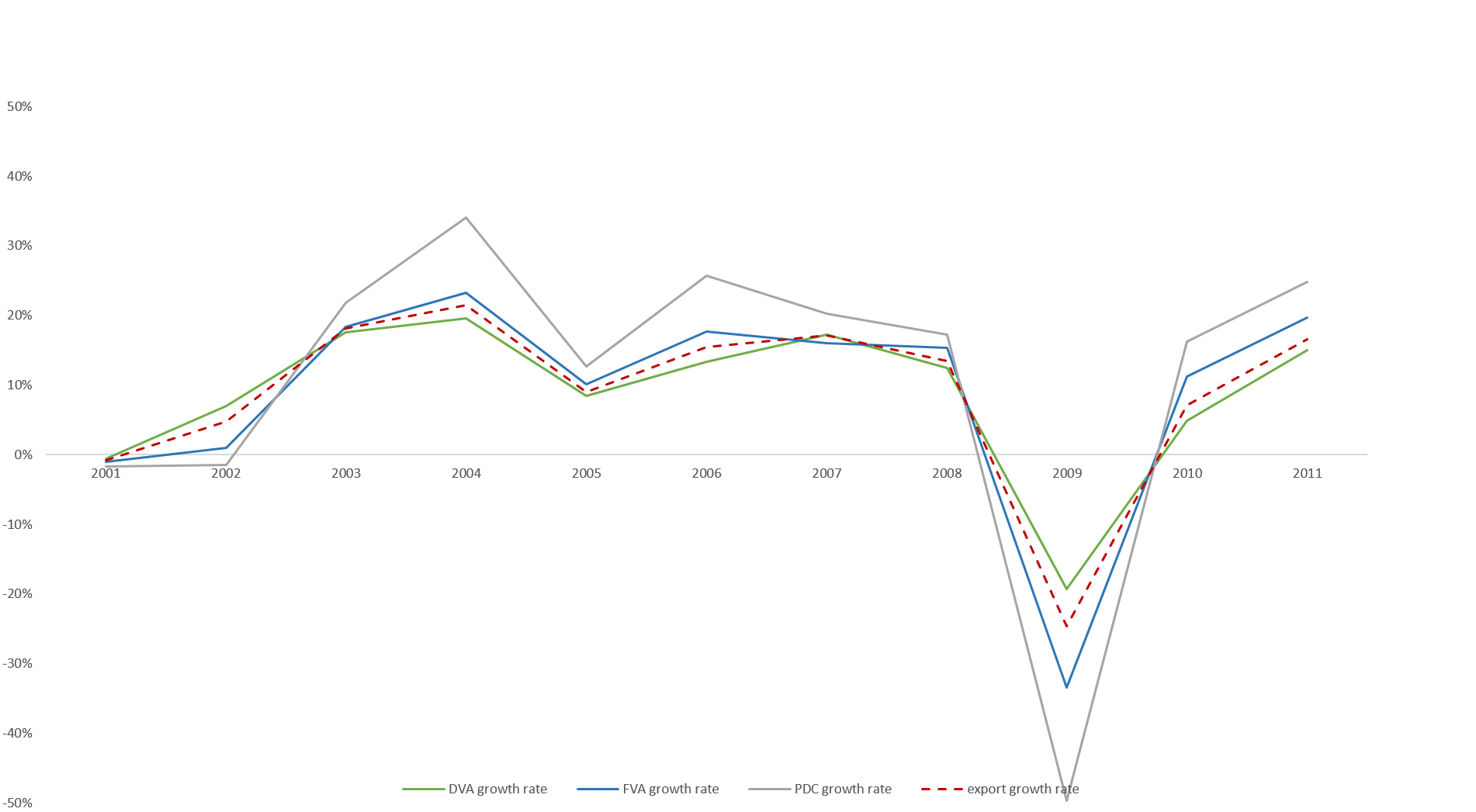

Figure 2 shows the growth of gross export and its components between 2001 and 2011. In 2009, as already discussed, trade experienced a sudden drop, and indeed all its components exhibited substantial negative growth rates in that year. However, FVA and PDC witnessed a much larger reduction than DVA. In particular, while DVA dropped by 19%, FVA dropped by 32%, and PDC by a striking 50%. In other words, the components of exports that are most directly related to GVCs were the ones most affected by the crisis.

Figure 2: Export components growth

{kind=link}

Source: Authors’ elaboration on Wang et al. (2013) data.

Starting from this novel descriptive evidence, we investigate whether the different components of exports display different speeds of adjustment to income shocks. In particular, we want to understand whether the GVCs-related components of trade, which have been most hardly hit by the crisis, are also experiencing a slower recovery. That would in fact provide an additional cyclical explanation for the recent trade slowdown. We perform this analysis by estimating an Error Correction Model (ECM), separately for gross export and each of its terms.[2]

First of all, our results seem to support the idea that, over time, the growth of global exports, and each of its components, should revert back to its long-run equilibrium relationship with GDP growth. In particular, the magnitude of our estimated long-run elasticity of gross exports to GDP is 1.3, very similar to what Constantinescu et al. (2015) have found for the period 2001-2013. Clearly though, the crisis may have induced a structural change in the trade-GDP relationship, which would imply that the very same long-run equilibrium elasticity has changed. This cannot be excluded at this moment, although it is too early to evaluate given the limited amount of data points available after 2009.

By running the Error Correction Model separately on the different components of trade, we find that FVA and PDC display a significantly lower speed of adjustment after a shock with respect to DVA. In particular, the estimated coefficients suggest that it takes around six years for FVA and PDC to converge after a shock, ceteris paribus, against slightly more than four years for DVA. Considering that FVA and PDC have dropped by more than DVA in 2009, such evidence of a slower adjustment sheds light on a new, GVCs-related cyclical explanation for the trade slowdown, as the hardest hit components of trade are also the slowest to recover.

Overall, our results suggest that the trade slowdown is likely to be partly re-absorbed over the coming years, at least to the extent that GVCs dynamics are responsible for it.

Policy implications

Our results have two main implications for policy. First, it is important that policy measures are undertaken in order to smooth the recovery process of trade after the initial collapse. This entails exerting more policy efforts on multilateral negotiations within the Doha round, but also on bilateral agreements such as the TTIP between the US and the EU. These agreements are in fact instrumental to trade facilitation, and to the reduction of non-tariff barriers. Thus, they are crucial for smoothing the operations of Global Value Chains across countries.

A second implication is related to the fact that GVCs are known to be relatively more important in some industries (e.g. automotive or chemicals) than in others (e.g. food). Therefore, country-specific patterns of the trade-GDP relationship are likely to depend on each country’s industry specialization. In particular, our analysis suggests that those countries that are relatively more specialized in GVCs-intensive industries (e.g. France or Germany) may expect their export slowdown to be less structural than thought so far. In fact, while part of the slowdown is certainly likely to depend on the deceleration of GVCs expansion, there seems to be also a GVC-induced cyclical component of the slowdown that is likely to be re-absorbed over time. By same token, countries in which GVCs play a relatively lesser role (e.g. Portugal or Finland) may expect to experience a relatively more persistent trade slowdown.

References

Amador, Joao, and Filippo di Mauro. "The Age of Global Value Chains: Maps and Policy Issues." VoxEU eBook, Centre for Economic Policy Research, 2015.

Baldwin, Richard E., ed. "The great trade collapse: Causes, Consequences and Prospects." Centre for Economic Policy Research, 2009.

Constantinescu, Cristina, Aaditya Mattoo, and Michele Ruta. "The global trade slowdown: cyclical or structural?" World Bank Policy Research Working Paper, WPS 7158, 2015.

Hoekman, Bernard. "The Global Trade Slowdown: A New Normal?" VoxEU eBook, Centre for Economic Policy Research, 2015.

Koopman, Robert, Zhi Wang, and Shang-Jin Wei. "Tracing Value-Added and Double Counting in Gross Exports." American Economic Review, 104(2) (2014): 459-94.

Wang, Zhi, Shang-Jin Wei, and Kunfu Zhu. Quantifying international production sharing at the bilateral and sector levels. No. w19677. National Bureau of Economic Research, 2013.

[1] A fourth component of gross exports is the “domestic value added which is first exported but eventually returned home” (RDV). This includes the export of intermediates that are processed abroad and return home, both as final as well as intermediate goods. We disregard this component in our analysis, as it makes up only 0.4% of exports on average.

[2] Our methodological approach follows earlier studies in the literature, for instance the recent paper by Constantinescu et al. (2015). Essentially, an ECM analysis of exports and GDP produces three interesting results: (1) an estimate of the long-run elasticity of exports to GDP, i.e. their long-term relationship; (2) an estimate of the short-run elasticity of exports to GDP, i.e. their immediate responsiveness after an income shock; (3) an estimate of the speed of adjustment of exports back to their long-term relationship after an income shock, i.e. how much time it takes for exports to converge again to the equilibrium, ceteris paribus.

About the authors

Related content

COVID-19 financial aid and productivity: has support been well spent?

In the EU, this support has prevented the emergence of unemployment and has kept average employment high.

EU recovery plans should fund the COVID-19 battles to come; not be used to nurse old wounds

In its proposed Recovery Fund, the European Commission uses allocation criteria mainly linked to infection rates and past economic performance. To fos

Remaking Europe: the new manufacturing as an engine for growth

Europe needs to know how it can realise the potential for industrial rejuvenation. How well are European firms responding to the new opportunities for

The knowns and unknowns of the European competitiveness debate

Micro-economic features of economic systems can have a major impact on national performance. Policymakers should therefore reconfigure their scoreboar