Belarus at a crossroads

Despite the slow pace of market reforms, the Belarusian economy recorded quite impressive growth until recently. However the Belarus growth ‘miracle’

Since the collapse of the Soviet Union in 1991, Belarus has maintained a largely non-market economic system. This did not prevent rapid growth of its economy over a sustained period up to 2011. However, the period of economic growth in Belarus seems to be over. The factors that underpinned Belarus’s growth, mainly the beneficial external environment, have gradually disappeared. As a result, the country is confronted by the need to start the far-reaching programme of market-oriented economic reforms and macroeconomic stabilisation which it tried to avoid for so long. Reform will not be easy, economically and politically.

The potential hardship facing Belarus could be at least partly cushioned by external assistance, in the first instance from the International Monetary Fund and the World Bank. However, the IMF has relatively fresh memories of the failure of its 2009-10 Stand-By Arrangement (SBA) with Belarus, which provided substantial balance-of-payments support, but which was derailed by its too-narrow focus on monetary and fiscal quantitative performance criteria, and by insufficient reform commitment on the Belarusian side. Other donors, such as the European Union, might be reluctant to offer assistance as long as Belarus does not improve its poor human rights record and start some political reforms.

In this analysis, we describe the characteristics of Belarus’s economic model, explain how the Belarus growth ‘miracle’ was possible, why it cannot be continued, the reforms that are needed and why they might be difficult to implement and, finally, what the chances are, and what the conditions might be, under which Belarus could obtain external support.

Europe’s last non-market economy

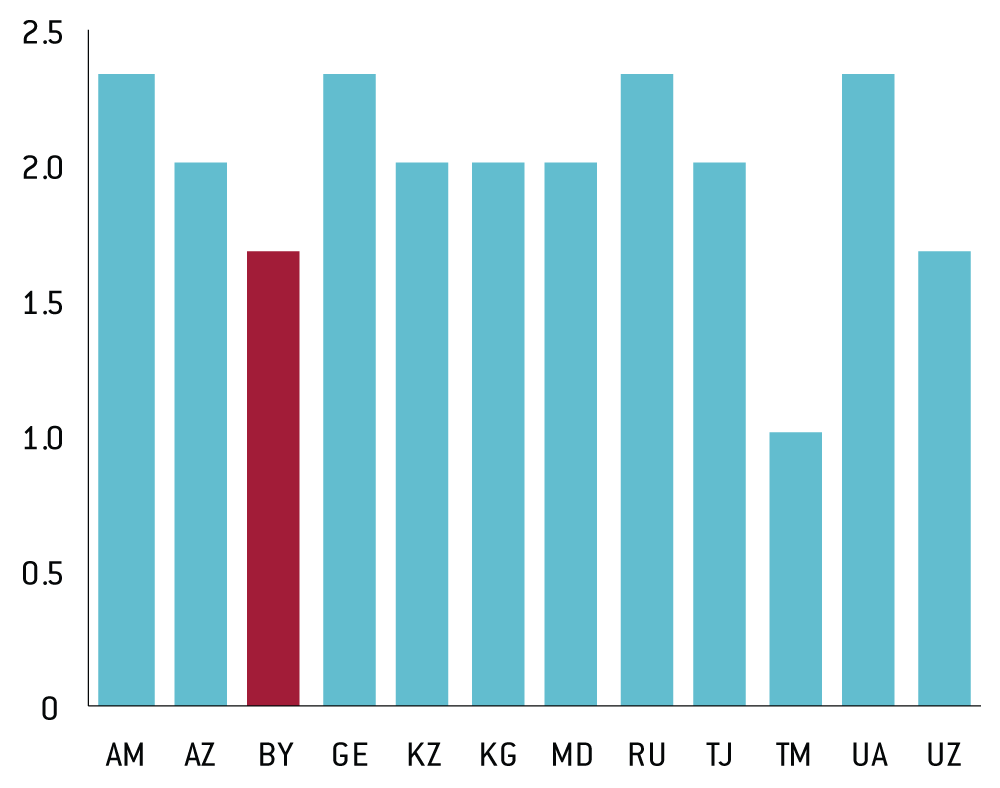

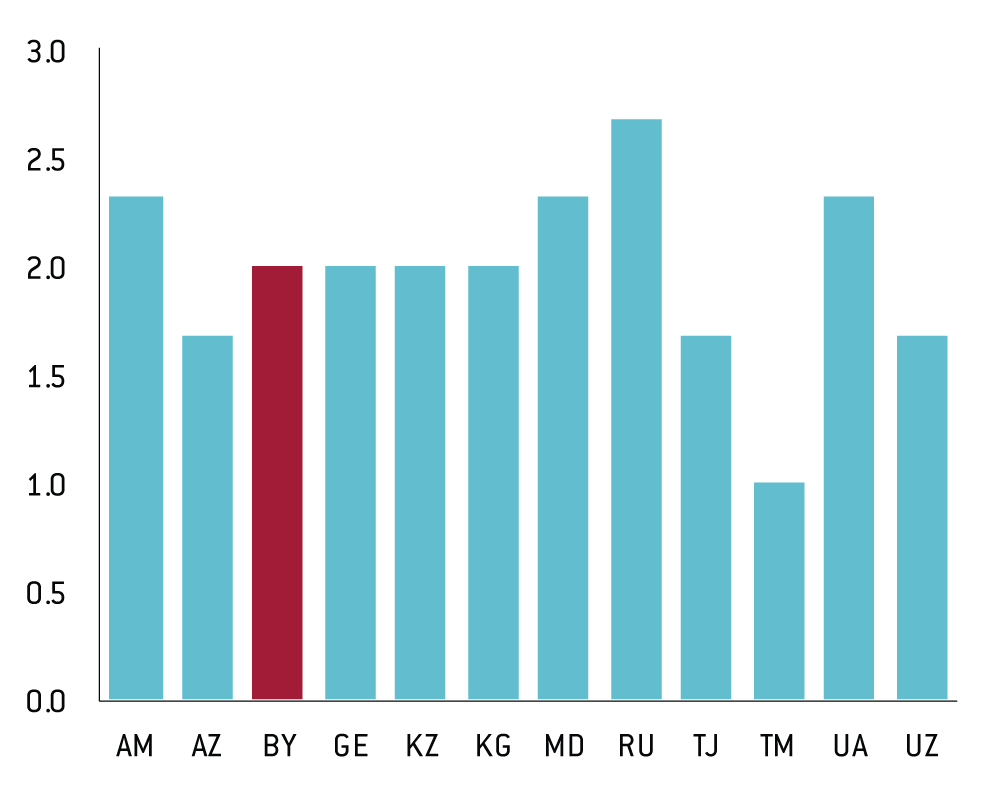

According to the European Bank for Reconstruction and Development’s (EBRD) transition indicators1 Belarus is among the least advanced of the former USSR’s successor states in building a market economy. It is one of three reform laggards, the others being Turkmenistan and Uzbekistan. This assessment relates to both ‘first generation’ reforms such as price, trade and foreign exchange liberalisation and small-scale privatisation (Figures 1-3), and to more sophisticated ‘second generation’ reforms such as large-scale privatisation, governance and enterprise restructuring, and competition policy (Figures 4-6). On average, all post-Soviet countries other than the Baltic states, lag behind central and eastern Europe in the implementation of ‘second generation’ reforms, which makes Belarus even less advanced than Figures 4-6 suggest.

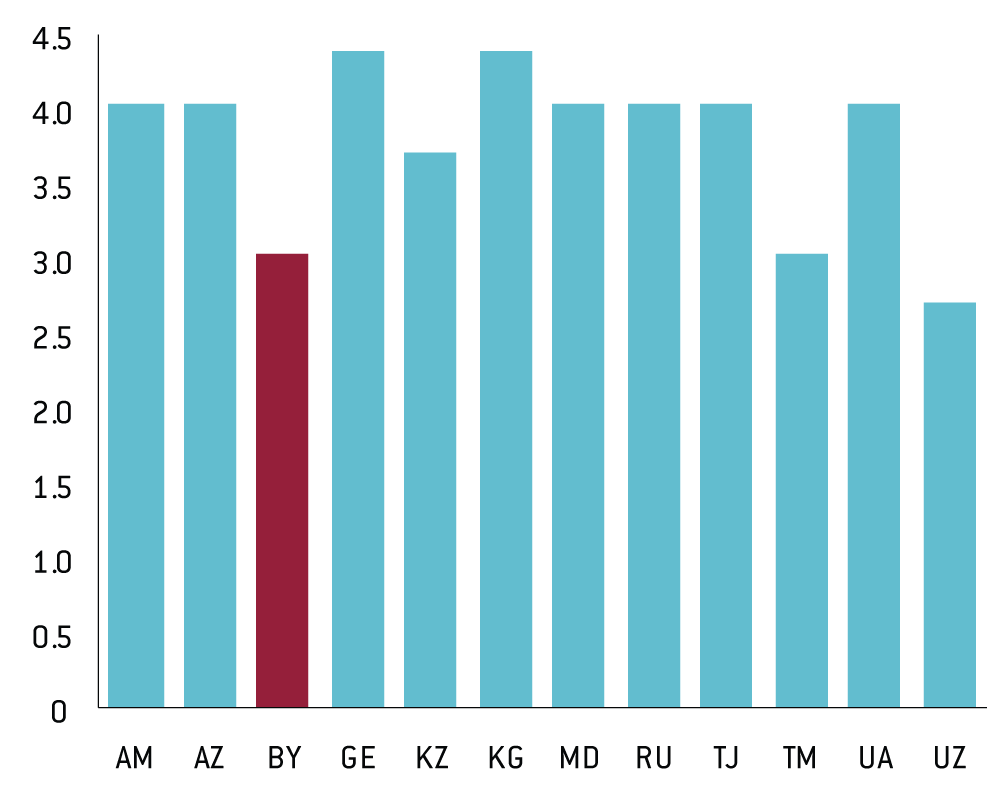

Price controls in Belarus have remained extensive, and have been reinforced with each macroeconomic crisis. For example, in 2011 after a major devaluation and its consequent pass-through to domestic prices, administrative price regulation of ‘socially important goods’ reached almost half (49 percent) of the consumer price index (CPI) basket. It subsequently went gradually down to 25 percent in 2014. However, after the devaluation of the Belarusian ruble (BYR) at the end of 2014, a temporary ban on all price increases was imposed (IMF, 2015a; IMF, 2015b) and stayed in force until April 20152.

Use of such broad price regulation has led to price distortions, which are particularly evident in the utility sector. Electricity tariffs remain, on average, at the level of about 50 percent of cost recovery. For natural gas, central heating and water supply, the situation is even worse, with tariffs converging to 20 percent of the cost recovery level in early 2015 (IMF, 2015a). It is worth remembering that Belarus is a net importer of energy resources (mainly from Russia) and excessive energy imports contribute to trade and current account deficits.

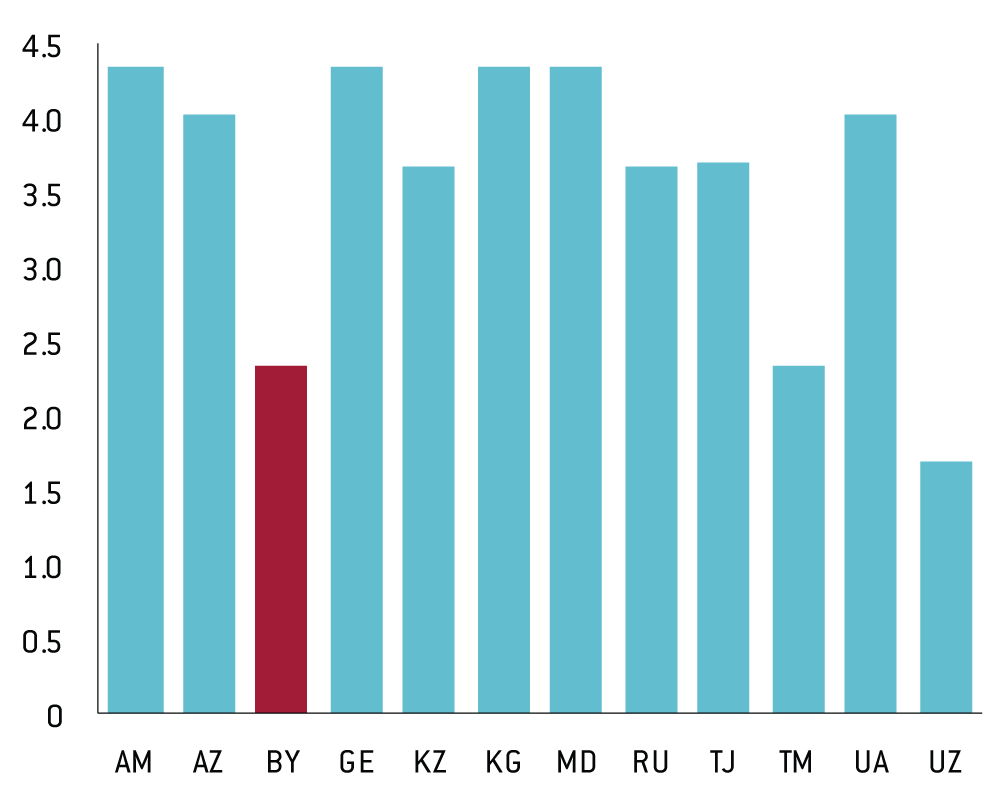

Although in 2001 Belarus formally introduced current-account convertibility of the BYR (as determined by Article VIII of the IMF’s Articles of Agreement), it has never fully respected it. Various forms of foreign-exchange restrictions have remained in place and in times of market strain, for example in 2008-09, 2011 and 2014-15, exchange restrictions were intensified, leading to the re-emergence of a ‘black’ foreign exchange market and multiple exchange rates (see IMF, 2015c).

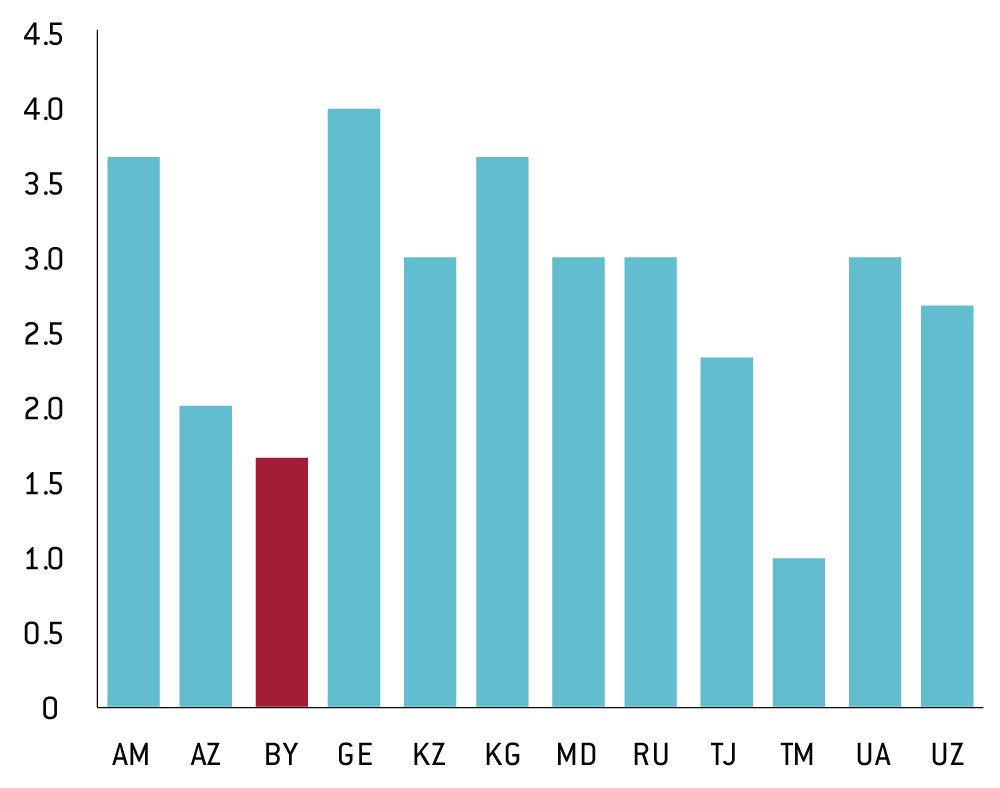

The role of the private sector remains limited. In 2010, according to the most recent EBRD estimate, the private sector’s share of Belarusian GDP amounted to 30 percent only3; probably it has not changed substantially since then. The activities of private firms are administratively restricted in various ways and are often the target of hostile government propaganda. Meanwhile, state-owned enterprises must still meet mandatory production targets, as in the era of the centrally-planned economy. If they fail to do so, their managers put their careers at risk or even face criminal prosecution.

Overall, Belarus retains a largely non-market economy, which is business unfriendly (IMF, 2012). Not surprisingly, the Heritage Foundation’s 2015 Index of Economic Freedom (IEF) ranks Belarus 153 among 178 countries, making it one of the ‘repressed’ economies4. Somewhat surprisingly, the World Bank Doing Business ranking placed Belarus much higher in its 2015 and 2016 reports – ranked 43 and 44 respectively, out of 189. Belarus has also systematically improved its ‘distance to frontier’ (ie to the best practices) scores since 20105 .

However, methodological differences must be taken into account. The World Bank Doing Business ranking concentrates on the number of administrative procedures (and their length) related to starting in business, dealing with construction permits, getting electricity, registering property, obtaining credit, protecting minority investors, paying taxes, trading across borders, enforcing contracts and resolving insolvency. It hardly captures the systemic remnants of a command economy such as de-facto mandatory production targets, and government-inspired investment, exchange restrictions, high inflation, or politically motivated insecurity of property rights. The latter are, at least partly, included in the IEF.

Figure 1: Commonwealth of Independent States, progress in price liberalisation, 2014

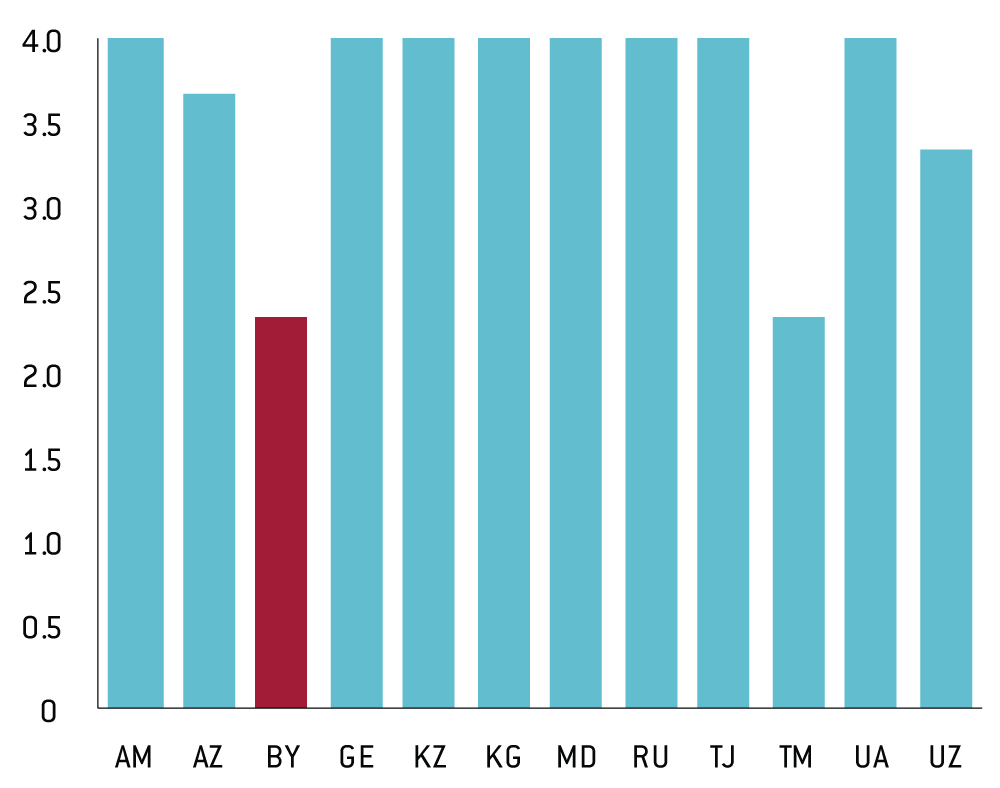

Source for all figures: EBRD Transition Indicators, 2014.

Note: AM = Armenia, AZ = Azerbaijan, BY = Belarus, GE = Georgia, KZ = Kazakhstan, KG = Kyrgyzstan, MD = Moldova,

RU = Russia, TJ = Tajikstan, TM = Turkmenistan, UA = Ukraine, UZ = Uzbekistan.

Figure 2: Commonwealth of Independent States, progress in trade and foreign exchange system liberalisation, 2014

Figure 3: Commonwealth of Independent States, progress in small-scale privatisation, 2014

Figure 4: Commonwealth of Independent States, progress in large-scale privatisation, 2014

Figure 5: Commonwealth of Independent States: progress in governance and enterprise restructuring, 2014

Figure 6: Commonwealth of Independent States, progress in competition policy, 2014

Rapid growth

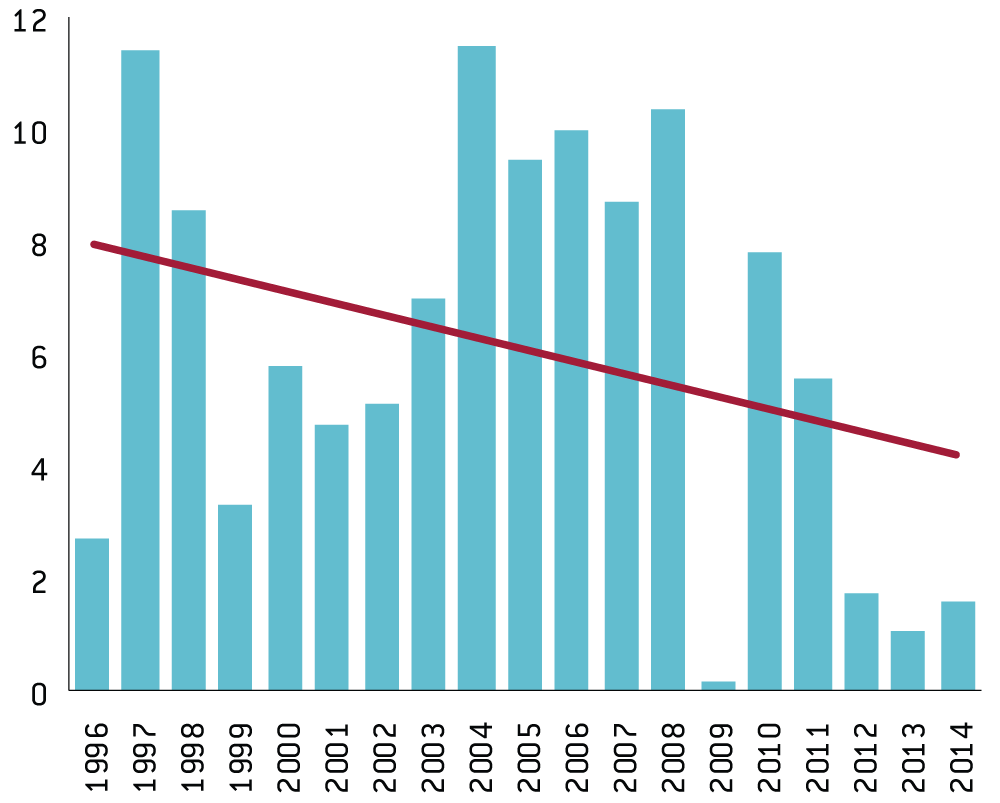

Despite the slow pace of market reforms (or even their reversal in the second half of the 1990s), the Belarusian economy recorded quite impressive growth for the decade and a half between 1997 and 2011 (Figure 7). This allowed some politicians and economists in the country to claim the advantage of the ‘Belarusian economic model’ over the market-oriented transition strategies pursued by Belarus’s neighbours.

To understand how the last enclave of the non-market economy in Europe not only managed to survive but also was able to grow rapidly, one must take into consideration several specific factors.

First, when the Soviet Union collapsed in 1991, Belarus was the second most developed country, after Russia, of the newly-formed Commonwealth of Independent States (CIS), in terms of GDP per capita at purchasing power parity (PPP). It enjoyed well-developed physical infrastructure and human capital and its industrial capacities were relatively modern and better oriented towards consumer and producer market demand, compared to other republics. This legacy allowed Belarusian industry to continue its previous role as a supplier of medium-quality and relatively inexpensive consumer goods to other post-Soviet countries, primarily Russia.

Second, also since the Soviet era, Russian oil and natural gas exports to Europe have transited through Belarus. Unlike Ukraine, Belarus has managed to extract substantial economic rent from this activity. This was made possible by various integration projects with Russia since the mid-1990s. Most of these, except the most recent – the 2010 customs union and the 2015 Eurasian Economic Union (EaEU) – were short lived. However, they allowed Belarus to purchase Russian energy resources at a lower price. Moreover, for several years, Belarus was able to resell to other countries Russian oil purchased at domestic or nearly domestic Russian prices (ie without export duties) and processed in Belarusian refineries (Novopolotsk and Mozyr) at market prices.

Third, unlike most other post-communist countries, Belarus has retained political and administrative capacity to continue operating a sort of command economic system. This was a result of the reluctance of the then prime minister Myechislav Kebich and his government in 1991-94 to start even partial market reforms. Belarus’s non-market system was then reinforced by the authoritarian political regime built by Alexander Lukashenko since he became president in 1994.

Fourth, the largely command character of the Belarusian economy manifested itself, among other ways, in a very high investment rate, significantly exceeding the average in the CIS and central and eastern European countries (Figure 8). This was somewhat reminiscent of the experience of forced industrialisation in the communist era. Most investment came from state-owned enterprises or was committed under government programmes. Obviously, such a high investment rate had to contribute to rapid growth but the non-market character of the investment process led to its low and steadily decreasing effectiveness (Kruk and Bornukova, 2014).

Finally, as we know from economic history, growth rates in non-market systems are not always fully comparable to those in market economies. Thisis not only because of potential over-reporting bias caused by the system of mandatory output targets. Even more important is the incomparability of GDP deflators when prices do not reflect the relative scarcity of goods because of extensive price controls, multiple exchange rates, trade barriers and physical shortages of good and services (see for example Bratkowski, 1993). Even in the periods of less severe price regulation and a single exchange rate, the choice of goods and services in the Belarusian market has remained more limited than in neighbouring countries.

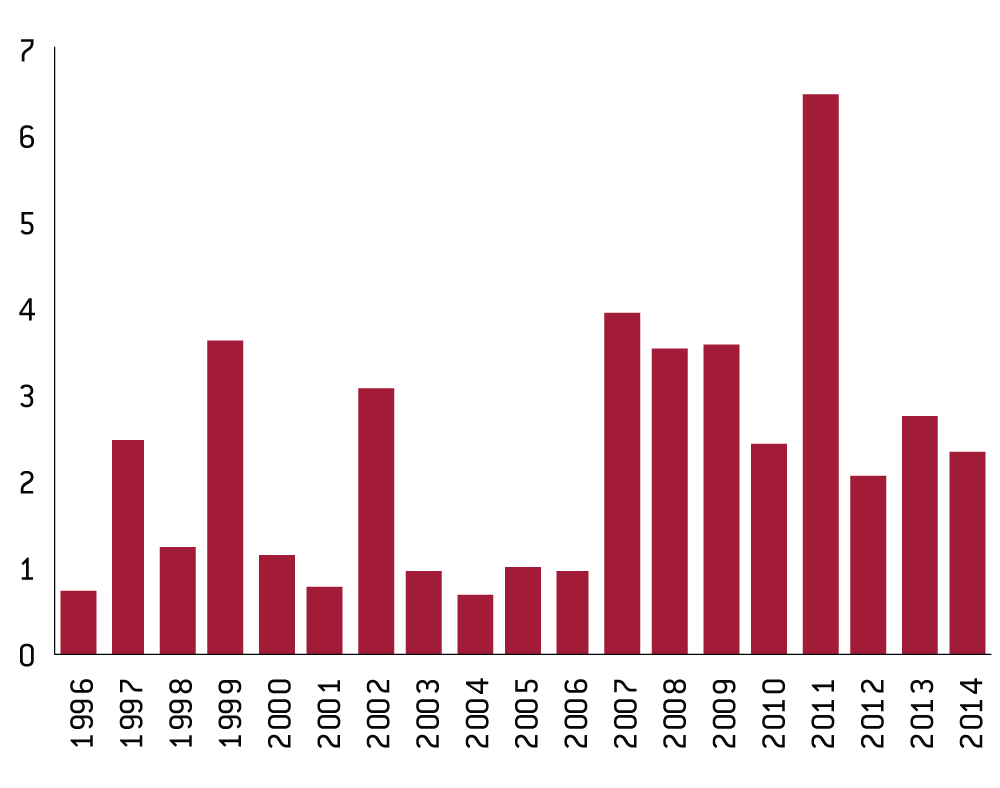

Figure 7: Belarus, GDP, constant prices, % change, 1996-2014

Source: Bruegel based on IMF World Economic Outlook

database, October 2015.

Figure 8: Investment rate in Belarus, CIS and emerging and developing Europe, % of GDP,1996-2014

Source: Bruegel based on IMF World Economic Outlook

database, October 2015.

Note: emerging and developing

Europe includes Albania, Bosnia & Herzegovina, Bulgaria,

Croatia, Hungary, Kosovo, Macedonia, Montenegro, Poland,

Romania, Serbia and Turkey.

Macroeconomic disequilibria

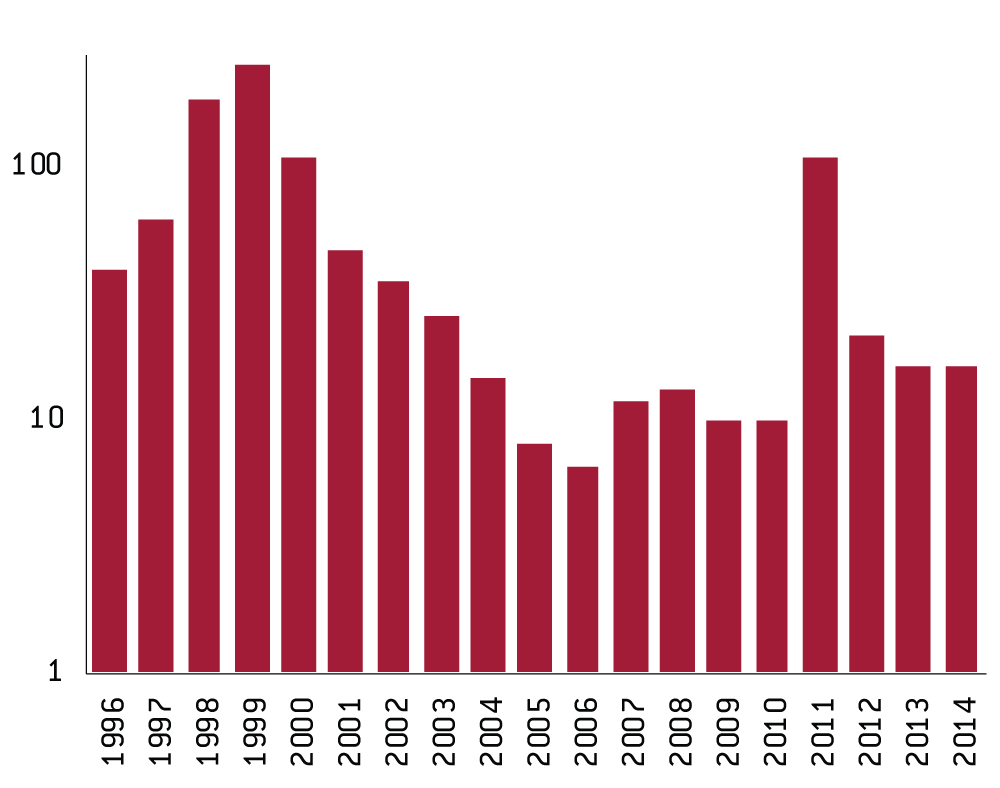

As Figure 9 shows, Belarus has suffered from chronic inflation at the high or moderately high level, despite its administrative price controls. Cumulatively, between 2000 and 2014, the consumer price index increased more than 17-fold (!) giving the country the dubious honour of inflation champion of the former USSR.

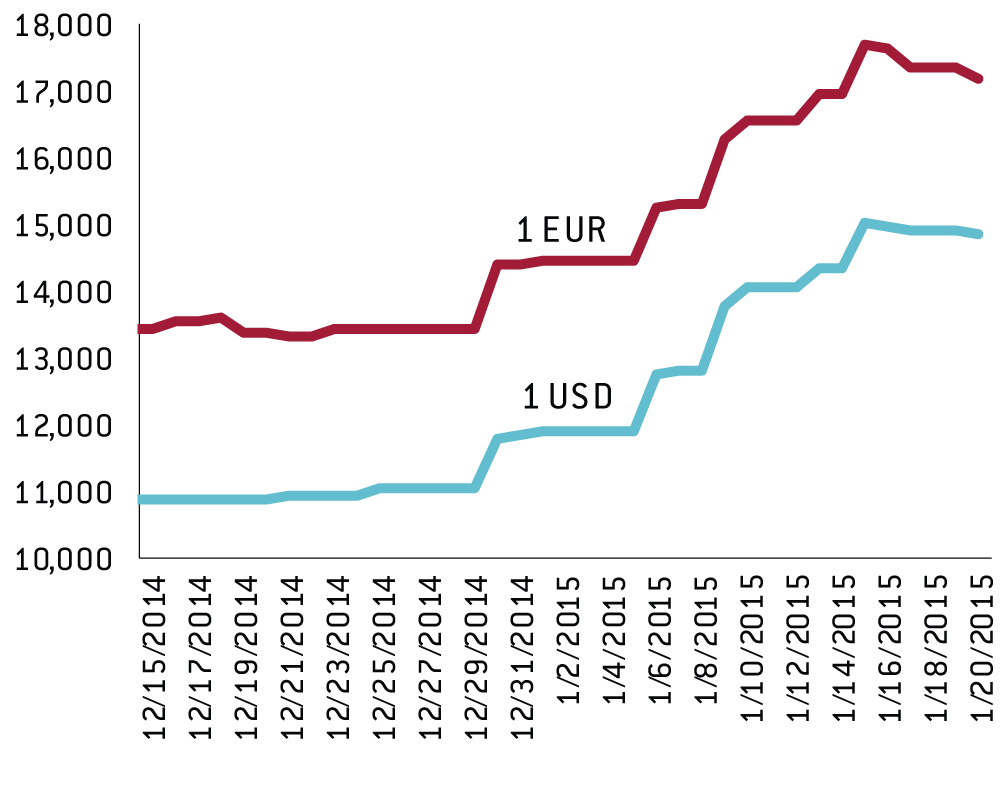

In particular, periodic inflation hikes resulted from abrupt devaluations of the BYR (see Figure 10). The most recent was triggered by the currency crisis in Russia at the end of 2014 and early 2015 (Figure 11) that spilled over to other CIS economies (Dabrowski, 2015). In turn, these devaluations were caused by balance-of-payments crises. Domestic monetary expansion voriginating from extensive quasi-fiscal activities has been another source of rapid price growth.

High inflation and frequent devaluations undermined trust in the BYR, which led to the high level of actual dollarisation. The ratio of foreign-currency denominated loans to total loans exceeded 55 percent in the first quarter of 2015 (IMF, 2015a).

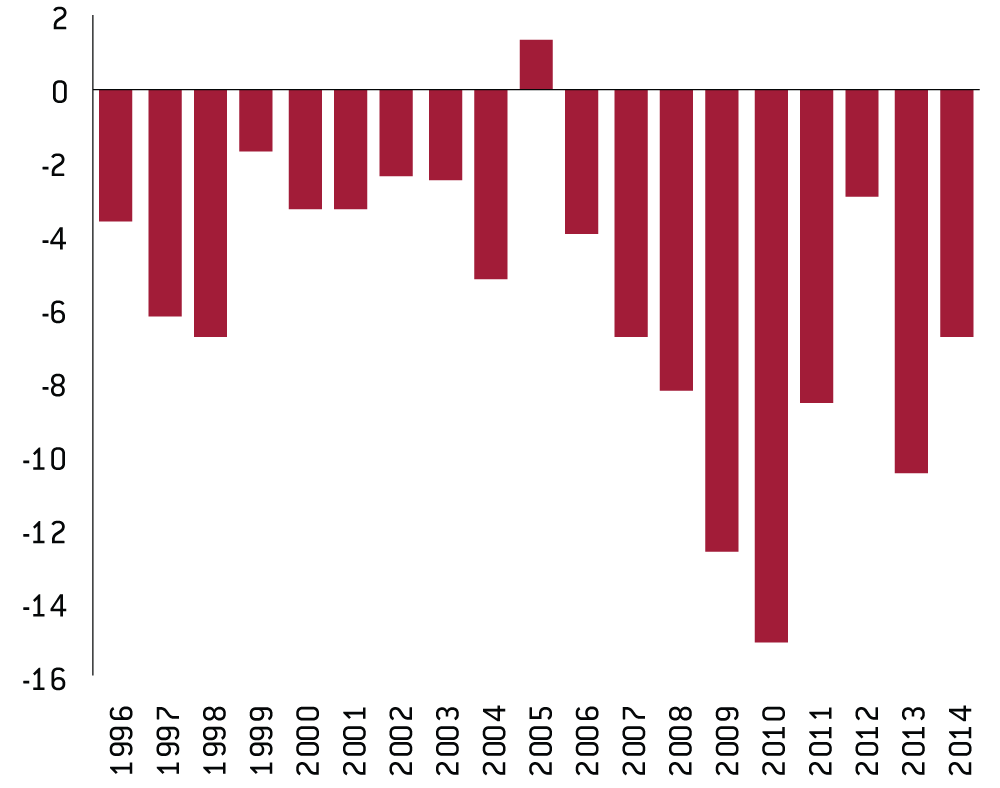

As Figure 12 shows, Belarus recorded continuous high current account deficits (resulting, among other factors, from the high investment rates) which, unlike in other transition economies, were largely financed by official borrowing (mainly from Russia, the Anti-Crisis Fund of the Eurasian Economic Community, and the IMF) and only partly by net inward foreign direct investment (Figure 13). As a result, the gross international reserves of the National Bank of the Republic of Belarus (NBRB) remained at the low level of $5.1 billion at the end of 2014 (IMF, 2015a). The net NBRB international reserves, ie gross reserves minus foreign liabilities, are negative.

FDI flows have mainly originated from Russia. Some have resulted from one-off large transactions involving the sale of Belarusian assets to Russian owners, such as sales to Gazprom in 2007 and 2011 of shares in Beltransgaz, which operates a gas transit pipeline from Russia to the EU.

Figure 9: Belarus, end-of-year inflation, %, 1996- 2014

Source: Bruegel based on IMFWorld Economic Outlook

database, October 2015.

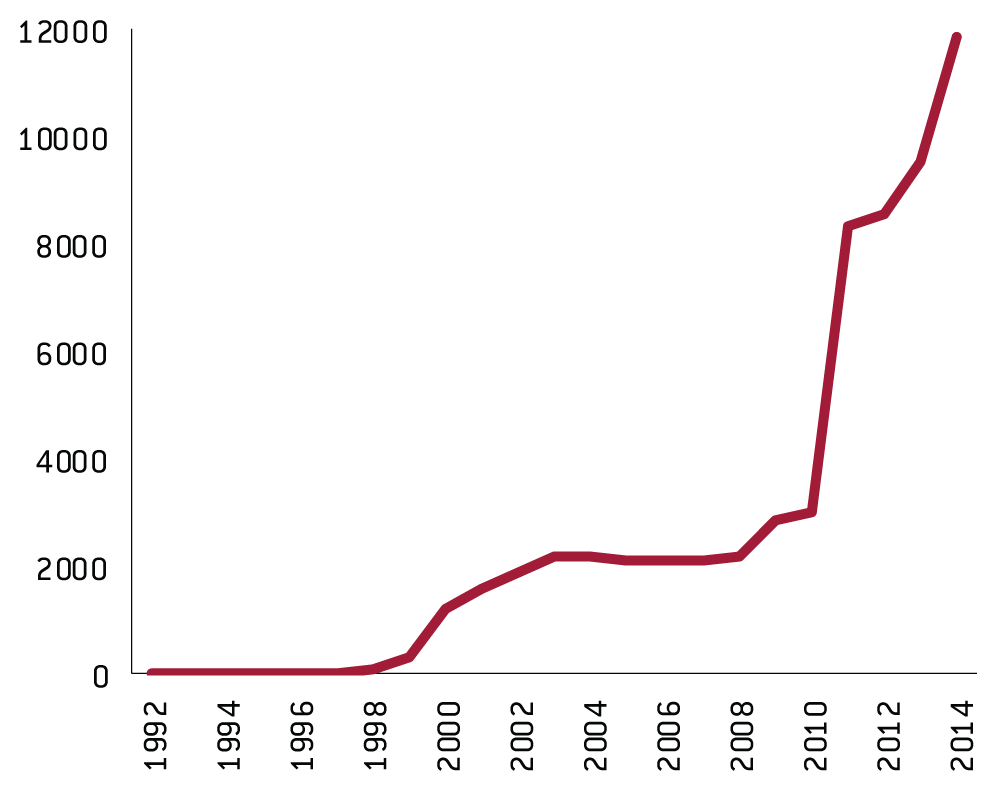

Figure 10: End-of-year exchange rate, BYR/1 USD, 1992-2014

Source: Bruegel based on

http://www.nbrb.by/engl/statistics/Rates/RatesDaily.asp.

Figure 11: Daily exchange rate, BYR/1 USD and BYR/1 EUR, December 2014 – January 2015

Source: Bruegel based on

http://bru.gl/1NmcwyM.

Figure 12: Belarus, current account balance, % of GDP, 1996-2014

Source: Bruegel based on IMF World Economic Outlook database, October 2015.

Figure 13: Belarus, net inward FDI, percent of GDP, 1996-2014

Source: Bruegel based on http://bru.gl/1OyEyLs.

Fiscal and quasi-fiscal balances

When an economy suffers from chronic high inflation and current account deficits, fiscal imbalances are the prime suspect. Paradoxically this is not the case in Belarus, at least at first sight. As Figure 14 shows, Belarus has had either fiscal surpluses or relatively small deficits since 1998. But the gross public debt statistics look less rosy (Figure 15). To resolve this apparent inconsistency, two factors must be taken into account: the necessity of official borrowing to close the balance-of-payments financing gap and domestic quasi-fiscal imbalances.

The second factor explains, to a great degree, the observed macroeconomic imbalances and repeated balance-of-payments crises in Belarus (see Miksjuk et al, 2015). While quasi-fiscal operations are present in various sectors of Belarusian economy, such as the energy sector and public utilities forced to provide their services at tariffs below the cost-recovery level, they mainly fall on the banking sector and the central bank.

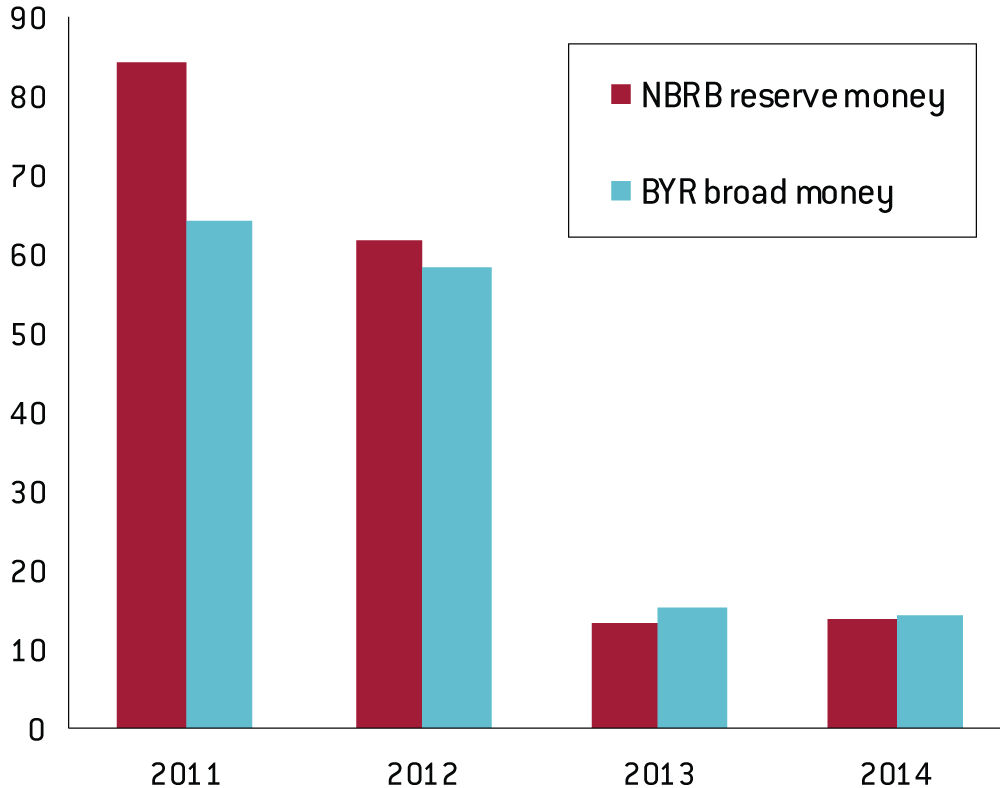

State-owned enterprises and farms that have to meet production targets and invest in new production capacity (often regardless of the effective market demand for their output) and carry out the government’s required wage increases are kept afloat by directed loans on highly concessionary terms. Directed and subsidised loans also serve as an instrument to support various government programmes, for example, in the housing sector. The exact legal forms of these loans have changed frequently, so measuring them is not an easy task. According to the IMF (2015a) their size increased from about 6 percent of GDP in 2010 to 9.3 percent in 2011 and then gradually decreased to about 4 percent of GDP in 2014. Without any doubt, this was a major driver of the rapid increase in both NBRB reserve money and BYR broad money (Figure 16), and a primary cause of the subsequent balance-of-payments crises.

Directed lending also leads to high levels of non-performing loans in the banking sector and the need for periodic recapitalisation of state-owned banks. For example, the cost of bank restructuring measures amounted to 4.9 percent of GDP in 2011 and is expected to amount to a further 2.8 percent of GDP in 2015. In addition, each year, the government must cover part of its credit guarantees related to directed lending. In the period 2011-15, this involved expenditures in the range of 0.3 and 0.9 percent of annual GDP (IMF, 2015a). These items are not included in the general government balances reported in Figure 14.

Figure 14: Belarus, general government net lending/borrowing, % of GDP, 1998-2014

Source: Bruegel based on IMF World Economic Outlook database, October 2015.

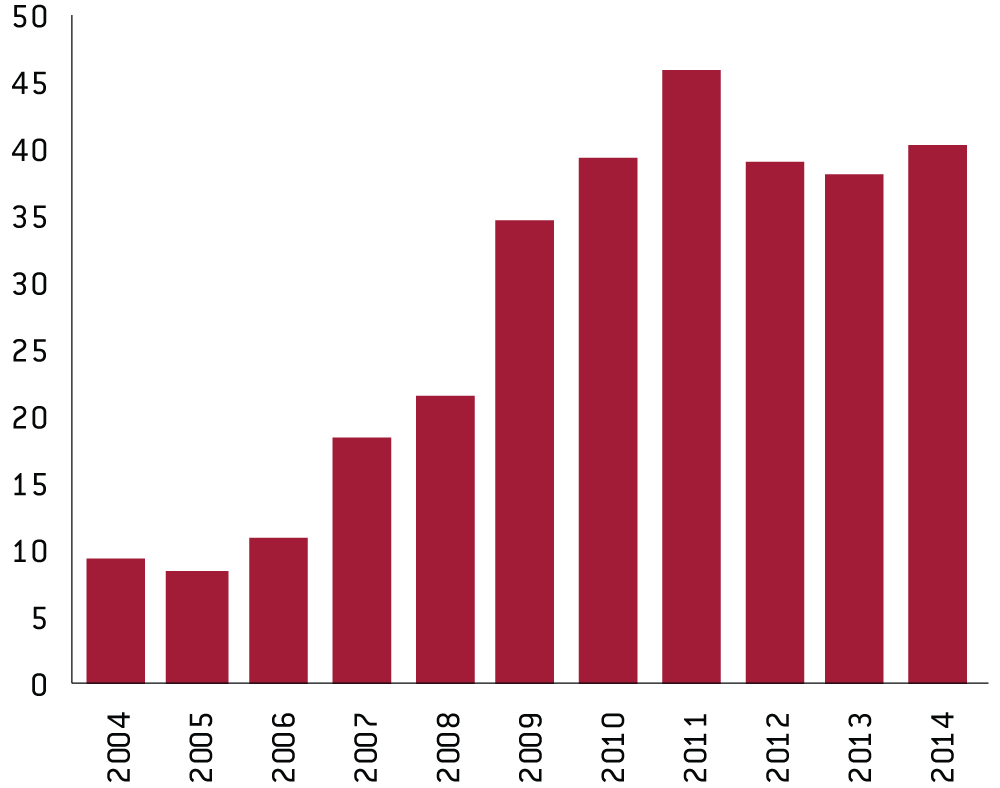

Figure 15: Belarus, end-of-year general government gross debt, % of GDP, 2004-14

Source: Bruegel based on IMF World Economic Outlook

database, October 2015.

Figure 16: Belarus, nominal increase in monetary aggregates, %, 2011-14

Source: Bruegel based on IMF (2015a), Table 1, p26.

The end of the belarusian model?

As seen in Figure 7, the debate on the sources and costs of Belarus’s high growth rate has already become a historical matter. Since 2011, growth has slowed substantially. For 2015, a 3.6 percent contraction is expected, according to the IMF World Economic Outlook October 2015 forecasts. The reasons for such a dramatic change are numerous.

Over the years, the country’s relative structural advantages have gradually disappeared. Growth in total factor productivity in Belarus’s dirigiste economy was relatively modest until 2008, and then started to decline (Kruk and Bornukova, 2014). Unreformed state-owned enterprises not sufficiently exposed to competitive market pressures lost part of their export markets, including Russia and other CIS countries. Russia’s accession to the World Trade Organisation (WTO) in 2012 and the formation of the EaEU exposed Belarusian companies to stronger external competition, on the Russian and domestic markets. In fact, being still far from completing its own WTO accession bid, Belarus has become unilaterally exposed to the WTO rules and competition from WTO members (via the EaEU) without symmetric access to their markets. This situation will become even more disadvantageous for Belarus following Kazakhstan’s WTO accession, which was completed in November 2015.

Gradual withdrawal by Russia of preferential prices for imported oil and gas has reduced substantially the oil and gas-related rents that accrue to the Belarusian economy and budget. The oil price decline in the second half of 2014 further reduced this rent and led to deterioration in Belarus’s terms of trade.

Belarus has also been hit indirectly by the consequences of the Ukrainian conflict, including the western sanctions against Russia and, especially, by Russia’s countersanctions against the EU and US, even if some Belarusian enterprises have been able to either substitute EU exporters to Russia or profit from circumvention of Russian countersanctions in the single EaEU customs space in the short-term.

The opportunity to receive further financial support from Russia or the EaEU in order to close the balance-of-payments gap has also diminished because of the increasing fiscal constraints in Russia and geopolitical differences over the Ukrainian conflict. More strategically, President Lukashenko seems to be reluctant to further increase Belarus’s dependence on Russia.

The required reform agenda…

To avoid a new round of the balance-of-payments crisis and to return to growth Belarus must finally accelerate its process of transition to a market economy.

Macroeconomic stabilisation and completing basic reforms are the most urgent tasks. These require the abandonment of price controls, direct and indirect subsidies, full current account convertibility of the BYR and the elimination of quasi-fiscal operations, in particular, directed lending. The NBRB must obtain genuine independence with a single mandate to ensure price stability.

However, this is not enough. As previous experience demonstrates, macroeconomic stabilisation will not be sustainable without accompanying microeconomic, structural and institutional reforms. These should involve a broad set of measures aimed at, among other objectives, dismantling the remnants of the command system, large-scale privatisation, opening up to foreign investment, completing WTO accession, closing down loss-making firms, easing the business and investment climate and reforming the financial system. Such an agenda will not be easy, economically, socially or politically. However, Belarus has lost too much time to wait longer.

…and its potential pitfalls

Since the end of 2014, there have been attempts to modify Belarus’s economic policy, including personnel changes in the government economic team and the NBRB, and a change in the official rhetoric in favour of less government control. For the first time, the presidential election in October 2015 was not preceded by massive credit expansion and administrative pressure for wage increases. The new leadership of the NBRB declared it would move to a flexible exchange rate for the BYR and monetary targeting, which will replace the previous regime of a crawling band against a currency basket. On the microeconomic front, there have been some measures to restructure the largest state-owned enterprises, including shedding of redundant labour (Alachnovic, 2015). These moves go in the right direction, but are not sufficient to restore growth and ensure macroeconomic stability in the long term.

It remains a big question whether the country’s authorities will decide to intensify reforms and make them sufficiently comprehensive. Apart from the usual political risks that accompany far-going market reforms in any country, in Belarus reform has always been seen as a challenge to its authoritarian political regime. This has been so far the main difference between Belarus and other CIS countries, many of which are also far from political freedom and democracy. However, for Belarus the status quo does not look sustainable: it does not offer the continuation of economic growth and living standard improvements, the basic preconditions of the regime’s political legitimacy.

The question of external support

Another question relates to the potential external support for a reform process. Obviously, Belarus can count on the support of the Bretton Woods institutions – in first instance, the IMF. The latter started discussing the prospects for a three-year Extended Fund Facility (EFF) programme with Belarusian authorities in November 2015 but it remains unclear how long this negotiation will take and what its final outcome will be. As put diplomatically in the IMF press release of 20 November 2015 ‘…discussions on some issues require more time’6. These are, most likely, structural and institutional issues that, as discussed, are key conditions for reform success. If completed successfully, the EFF might be supplemented by World Bank loans focused on concrete structural and institutional reforms.

The IMF faces a major challenge to avoid repeating the mistakes of the 2009 SBA when under the geopolitically motivated pressure of some its major shareholders (including the EU), the programme was insufficiently tough and comprehensive (especially in relation to structural benchmarks). The Belarusian authorities used the programme’s various loopholes to continue directed lending to state-owned enterprises on concessionary terms (IMF, 2011 and 2012) and to de-facto finance the 2010 presidential election campaign, which ended up with the large-scale currency crisis in the first half of 2011 (ie just after completion of the SBA).

As discussed, the success of macroeconomic stabilisation in Belarus depends on a front-loaded programme to dismantle the legacies of the command system, complete basic market reforms and carry out comprehensive microeconomic restructuring. Some of these reforms should go beyond the standard agenda of SBA/EFF and even World Bank programmes, especially when they touch governance issues and the political system.

Here interventions by other bilateral and multilateral donors, including the EU and the US, play usually a useful role. However, it remains unclear if Belarus can expect such support, similar to other Eastern Partnership countries, without carrying out at least limited political reforms and improving its poor human rights record.

To restructure its economy, Belarus also needs large-scale FDI, primarily from the OECD countries. This might be difficult to accomplish as long as Belarus does not improve its business and governance image and fails to complete its macroeconomic stabilisation. Although in the 2014 Transparency International Corruption Perception Index, Belarus is rated ahead of Azerbaijan, Kazakhstan, Kyrgyzstan, Russia, Ukraine, Tajikistan, Uzbekistan and Turkmenistan, its position far down the ranking in place 119 out of 174 countries means that this area also requires a lot of effort.

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

Ukraine’s path to European Union membership and its long-term implications

The war complicates the accession process, but Ukraine can work progressively towards meeting the entry conditions

To become a geopolitical player the European Union needs Treaty change

The EU will never become a serious geopolitical player without reducing national veto power.

Halftime for the European Union’s recovery fund: is the glass half full or half empty?

How has the RRF performed at its halfway point in terms of implementation, results orientation and additionality for future EU funding instruments?