The European Central Bank’s quantitative easing programme: limits and risks

The ECB has made a series of changes to its QE programme in order to expand the universe of purchasable assets and have more flexibility in the execut

Highlights

- The European Central Bank (ECB) has made a number of significant changes to the original guidelines of its quantitative easing (QE) programme since the programme started in January 2015. These changes are welcome because the original guidelines would have rapidly constrained the programme’s implementation.

- The changes announced expand the universe of purchasable assets and give some flexibility to the ECB in the execution of its programme. However, this might not be enough to sustain QE throughout 2017, or if the ECB wishes to increase the monthly amount of purchases in order to provide the necessary monetary stimulus to the euro area to bring inflation back to 2 percent. To increase the programme’s flexibility, the ECB could further alter the composition of its purchases.

- The extension of the QE programme also raises some legitimate questions about its potential adverse consequences. However, the benefits of this policy still outweigh its possible negative implications for financial stability or for inequality. The fear that the ECB’s credibility will be undermined because of its QE programme also seems to be largely unfounded. On the contrary, the primary risk to the ECB’s credibility is the risk of not reaching its 2 percent inflation target, which could lead to expectations becoming disanchored.

EXECUTIVE SUMMARY

- The European Central Bank (ECB) has made a number of significant changes to the original design of its quantitative easing (QE) programme since the programme started in January 2015. The bank has expanded the list of national agencies whose securities are eligible for the Public Sector Purchase Programme (PSPP); it has changed the issue share limit (ensuring that the Eurosystem will not breach the prohibition on monetary financing), which was originally set at 25 percent, to 33 percent (at least for securities without collective action clauses); it has added regional and local government bonds to the list of eligible assets; it has announced that the programme would continue past September 2016, the previously-announced minimum end-date, to March 2017 “or beyond, if necessary”; and it has declared its intention to reinvest the principal payments on the securities purchased under the programme as they mature.

- As explained in Claeys et al (2015b), the programme’s original guidelines would have constrained the size and duration of the programme, especially if it was sustained throughout 2017. The changes to the design of the programme announced during 2015 greatly expand the universe of purchasable assets and should therefore delay the point at which limits will be reached. However, the decision to reinvest the principal payments as bonds mature, by increasing the monthly monetary purchase after March 2017, would also lead to the limits being reached sooner. In the same way, a decision by the ECB to increase the amount of PSPP purchases each month, for instance from €44 billion to €64 billion, would also frontload the purchases. In the end, because of the issue share limit, for a given set of securities there will always be a trade-off between larger monthly purchases and a prolonged programme.

- Further changes to the design of the programme will have to be implemented in order to increase the duration of the programme if the limit is binding in a major country before inflation is on the path towards 2 percent. These could include waiving the issue limit for AAA-rated bonds, or purchasing senior uncovered bank bonds as well corporate bonds. A more radical change could be to move away from an allocation of asset purchases between countries based on the ECB capital keys to an allocation based on the actual size of their outstanding debt.

- We also discuss the possible financial stability risks of a prolonged and large-scale QE programme, and conclude that the benefits of large-scale asset purchases outweigh their potential risks in terms of financial stability. However, micro- and macro-prudential policies should be used forcefully to prevent such risks from materialising.

- We also consider the potential effects that a prolonged asset-purchase programme could have on inequality. The increase in inequality observed in many advanced countries in recent decades is a long-term trend and primarily the result of deep structural changes. Our view is that the primary mandate of the ECB is to maintain price stability, and considerations of inequality are not within its purview, unless inequality prevents the transmission of monetary policy in some way. The ECB should therefore focus on fulfilling its price stability mandate by supporting the fragile recovery now taking place in the euro area. This is the best way for monetary policy to contribute to the avoidance of an increase in inequality.

- The fear that the ECB will lose its credibility solely because it is currently buying a large amount of sovereign bonds appears to be largely unfounded. The primary risk to the ECB’s credibility is the risk of not reaching its inflation target. In our view, the ECB should therefore try to find the right balance between the risk of breaching the monetary financing prohibition and the risk of not fulfilling its mandate because of the limits imposed on its own QE programme.

1. Introduction

On 22 January 2015, the European Central Bank (ECB) introduced the Public Sector Purchase Programme (PSPP). Under the PSPP, the Eurosystem started in March 2015 to buy sovereign bonds from euro-area governments and securities from European institutions and national agencies.

On 3 December 2015, ECB president Mario Draghi announced an extension of the programme. While it was initially foreseen to last until at least September 2016, it was extended until at least March 2017. Additionally, regional and local government bonds were added to the list of eligible assets for purchase, and the interest rate on the deposit facility was lowered from -0.2 percent to -0.3 percent.

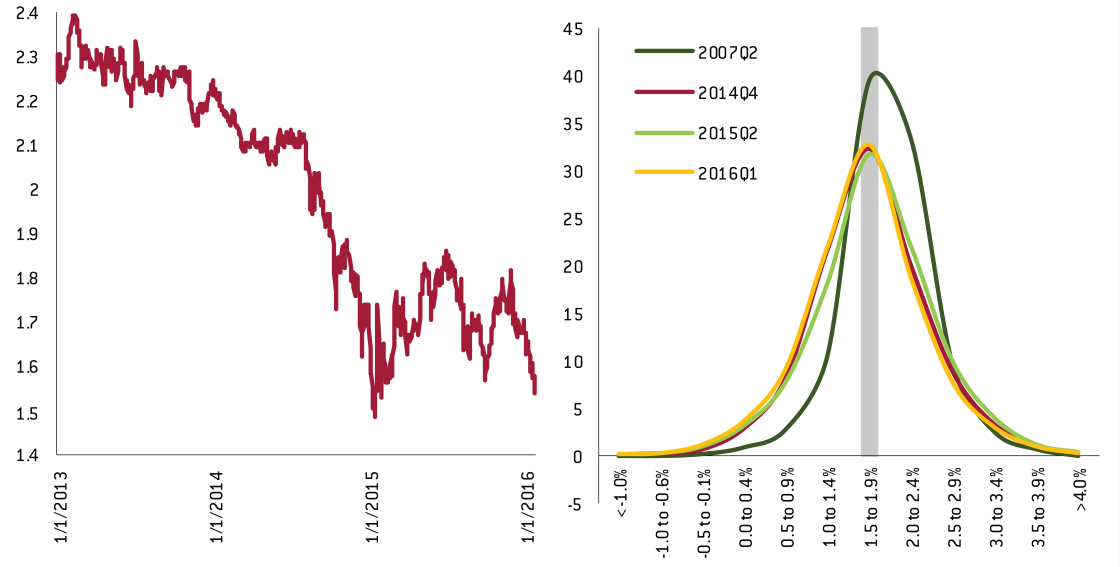

President Draghi said that the asset purchase programme would continue “until we see a sustained convergence towards our objective of a rate of inflation which is below but close to 2 percent” (Draghi 2015c). This goal remains far from being fulfilled: euro-area year-on-year headline inflation has been below 2 percent since January 2013, below 1 percent since November 2013, and was still at 0.2 percent in December 2015, while core inflation was only at 0.9 percent. In the meantime, and most importantly, both medium- and long-term market-based expectations and inflation forecasts have started to fall again (Figure 1). As both measures suggest, after a clear decline until the end of 2014, inflation expectations rebounded significantly after QE was announced in January 2015 and during the whole first half of 2015. However, expectations recently fell back to previous lows, heavily influenced by the steep decline in oil prices, as explained in Darvas and Hüttl (2016).

Figure 1: Market-based and survey-based inflation expectations in the euro area

Sources: Thomson Reuters Eikon (left panel) and ECB Survey of Professional Forecasters (2016) (right panel). Note: HICP = Harmonised Index of Consumer Prices.

For these reasons and because inflation appears likely to substantially undershoot the ECB’s staff forecast over the next two years, it is probable1 that the ECB will enhance its programme further in order to fulfil its mandate and bring inflation back towards 2 percent in the medium term. Even if the impact of asset purchase programmes is more difficult to measure than that of more conventional monetary measures, a growing literature2 concludes that QE programmes implemented around the world boosted inflation, output and employment.

For the euro area in particular, the effects of QE are even more difficult to pin down given that the programme only started in March 2015. However, there are already some indications that QE is having some impact on the euro-area economy. The effects on the exchange rate and on interest rates (and in particular on financial fragmentation in the euro area, with credit rates converging again) have been the most visible. In terms of inflation, monetary measures take time to materialise in prices and it is very difficult to know what can be attributed exactly to QE, but, for instance, the basket share of the consumer price index in deflation declined from 40 percent at the beginning of 2015 to 25 percent at the start of 2016. Darvas (2016) also shows that core inflation adjusted for second-round effects of energy prices went up over 2015 and, after reaching a low point in Q1 2015 of around 0.7 percent, it is now at 1.2 percent, a level unseen since 2011.

However desirable they might be, the recent – and maybe future – extensions of the asset purchase programme raise questions about how its size and its duration can be materially increased given the finite volume of purchasable debt securities. In fact, the universe of purchasable debt securities needs to be expanded because of the ECB’s self-imposed limit on the proportion it can hold of a given debt issue (decided at the launch of the programme) and not so much because of the scarcity of debt securities.

Claeys et al (2015b) showed already at the launch of the PSPP that without any changes to the design of the programme this limit could be reached in March 2017 or before in a number of countries. For Germany, calculations in Claeys et al (2015b) suggested that the limit would be reached in April 2017. Given the structure of the programme using the ECB capital keys to determine the distribution of purchases between countries, this could have seriously limited its effectiveness.

Since then, the issue share limit was raised in September 2015, and the changes to the programme in December 2015 further expanded the universe of eligible debt that can be purchased by the Eurosystem. However, these expansions might still not be enough to prevent the limits being reached before the inflation target is achieved. Furthermore, the unconventional and previously untested nature of such a programme poses legitimate questions regarding the potential adverse consequences that such a substantial and prolonged programme could have.

In section 2 we explain the changes to the design of the purchase programme during its first year of implementation, and their implications for our calculations on when the limits will be reached, also envisaging a scenario in which the monthly amounts purchased under the PSPP would be increased. We then discuss potential risks that accompany a lengthy and massive asset-purchase programme in terms of inequality, financial stability and the central bank’s credibility.

2. Potential implementation limits of the asset purchase programme

2.1 The extended asset purchase programme’s original guidelines

On 22 January 2015 the ECB announced a massive expansion of its asset purchase programme. To supplement the Asset-Backed Securities and Covered Bonds Purchase Programmes (ABSPP and CBPP3) launched in September 2014, the ECB introduced a new Public Sector Purchase Programme (PSPP) to buy sovereign bonds from euro-area governments and securities from European supranational institutions and national agencies. While total monthly purchases of asset-backed securities and covered bonds had previously amounted to approximatively €10 billion per month, the new purchases of sovereign bonds, supranational institutions, and agencies raised the figure to €60 billion per month, €44 billion of which was dedicated to purchases of government and national agency bonds (and this €44 billion was divided between euro-area countries according to each country’s capital subscription at the ECB). The purchases started on 9 March 2015 and were originally meant to last at least until September 2016. The ECB’s Governing Council also made it clear at the time that the programme was open-ended and that purchases would be conducted until the ECB would see “a sustained adjustment in the path of inflation which is consistent with the aim of achieving inflation rates below, but close to, 2 percent”.

On top of the eligibility criteria (ie only debt securities with a remaining maturity between 2 and 30 years and with a yield above the deposit rate can be bought), the ECB’s Governing Council also decided to put in place a 25 percent issue limit and a 33 percent issuer limit on Eurosystem holdings. The 25 percent issue limit was imposed to prevent the ECB from having “a blocking minority in a debt restructuring involving collective action clauses”. This indicated that the ECB did not wish to be in a position in which it had the power to block a potential vote on the restructuring of ECB-held debt of a euro-area country, because not blocking such a restructuring would be interpreted as monetary financing of a member state3.

2.2 Changes to the ECB’s guidelines since March 2015

The ECB’s rules on the Public Sector Purchase Programme (PSPP) have gradually been adapted since the programme started in March 2015. As highlighted in Claeys et al (2015b), the original rules rapidly constrained the purchases in countries in which public debt was small and in which no national agencies were identified as eligible for purchases. The aim of most of the changes was therefore to expand the universe of available debt securities that the Eurosystem could purchase, in order to delay the point at which the programme would reach its limits in each euro-area country.

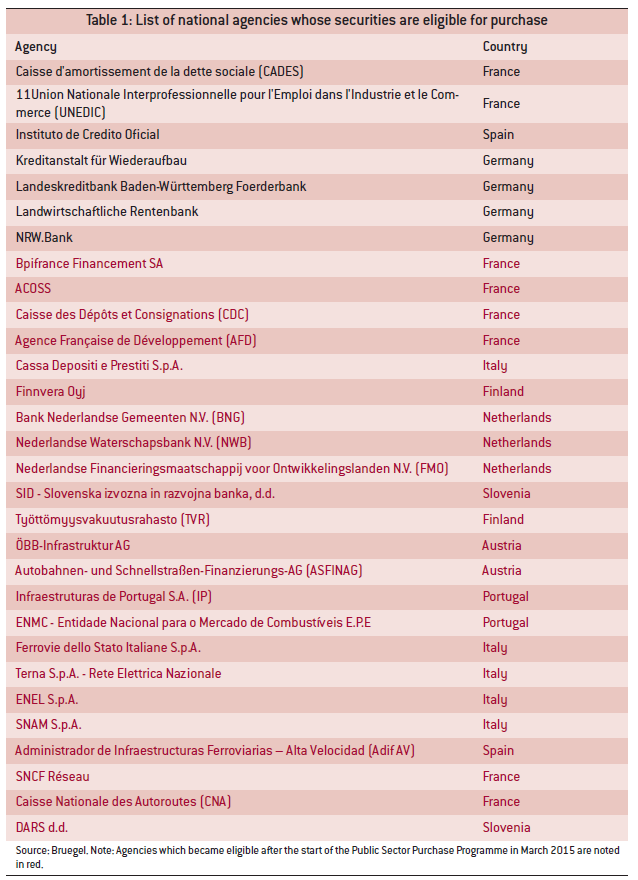

In July 2015, the ECB expanded the list of national agencies whose securities are eligible for purchase under the PSPP (see Table 1), thereby allowing the Eurosystem to purchase debt securities in countries where the limits had already been reached, or were expected to be reached soon.

In September 20154, the issue share limit was increased from 25 percent to 33 percent for debt securities not containing collective action clauses (CACs). This change to the maximum amount that the Eurosystem can hold of a particular issue allows the PSPP to potentially continue for longer than was originally possible under the previous rules.

In December 20155, the Governing Council announced many new changes to the design of the PSPP. First, it decided to reduce the deposit rate from -0.2 percent to -0.3 percent. Since the Eurosystem decided to purchase bonds with yields above the deposit rate in order to avoid making a direct loss on the purchases6, the cutting of the deposit rate effectively increased the amount of debt securities eligible for purchase (even if the rate cut also reduced yields and therefore limited the volume increase). Second, the ECB decided to continue the PSPP past the previously-announced minimum end-date, September 2016, until March 2017, “or beyond, if necessary”. Third, euro-denominated debt issued by regional and local euro-area governments became eligible for purchase. Finally, the ECB declared its intention to reinvest the principal payments on the securities purchased under the programme as they mature, for as long as necessary. This effectively implies that in March 2017, two years after the start of the programme, when the first bonds bought by the Eurosystem will start to mature, monthly purchases of sovereign and agency bonds could exceed €44 billion, as the principals of these maturing bonds will be reinvested.

2.3 Limits of the programme in terms of size, duration and composition

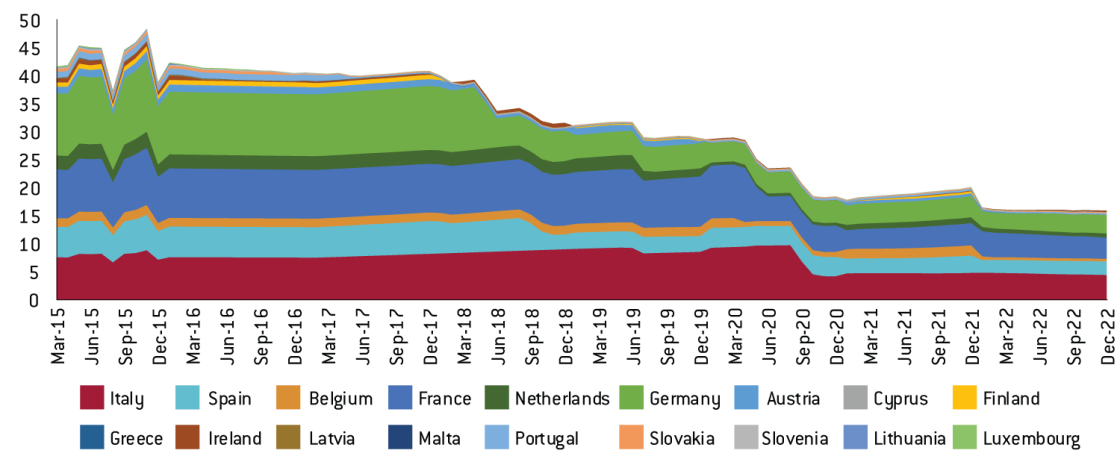

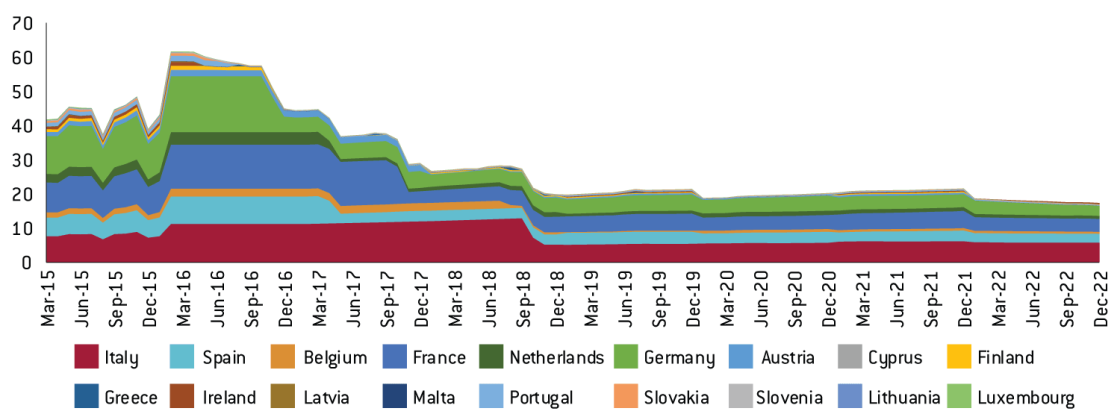

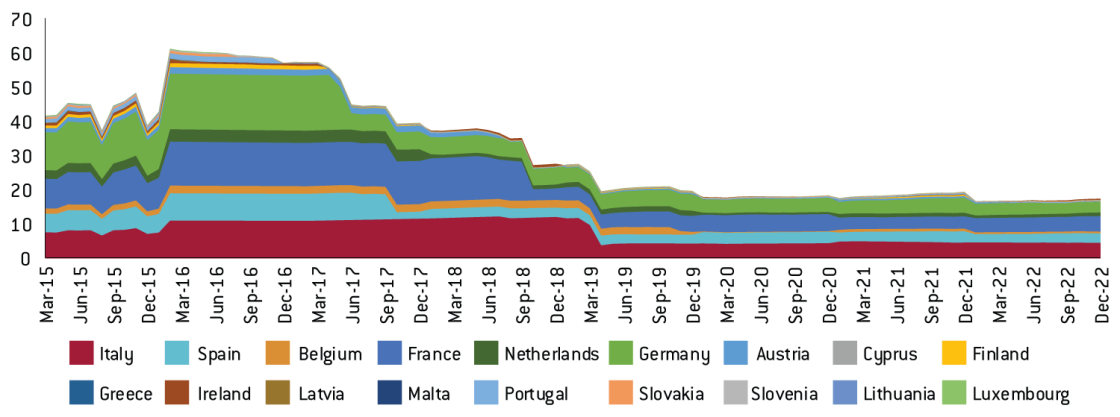

Claeys et al (2015b), published at the time of the start of the purchases, calculated when the ECB’s limits would be reached in each euro-area country (Figure 2). In this section we update these calculations7 in light of the changes to the rules. We also include national agencies in our calculations8.

Before September 2015 the issue limit was 25 percent regardless of the type of bond. Now, however, this limit is 33 percent if the issue does not contain a collective action clause. Unfortunately, information on whether an issue contains a CAC is not readily available. We know, however, that according to the ESM Treaty9, all euro-area government debt securities with maturity over one year issued after 1 January 2013 contain CACs. Therefore, we envisaged two extreme scenarios: in the first scenario, we assume that all eligible debt securities, be they from agencies, local governments, or central governments, have CACs, in which case the Eurosystem can only hold a maximum of 25 percent of a country’s eligible debt securities. In the second scenario, we assume that the only debt securities to have CACs are those issued by central governments after 1 January 2013 (in this scenario, the Eurosystem can hold 25 percent of each issue containing CACs, and 33 percent of each issue which does not). Reality will lie between these two extremes.

Figure 3 shows our projections for the monthly purchases, by country, in the scenario in which every debt security contains a CAC. Despite the increase in eligible debt (with the expanded list of agencies, and the new ability to buy regional and local debt), the limits are reached roughly at the same time as in Figure 2, and even earlier in some cases. This is because of the reinvestment of principals, which kicks in in March 2017: it effectively raises the amounts purchased each month, and increases the speed at which the limits are reached. In fact, while redemptions of PSPP holdings will be small at first, they would accelerate quickly as more and more debt securities held by the Eurosystem mature. In Germany, for instance, the holdings maturing in March 2017 will be worth a few million euros, while, were the programme to go on until then, they will be worth roughly €1.5 billion per month in March 2019, which is sizeable because it would increase the monthly purchases of German bonds by approximately 10 percent. This effectively means that, while the limits will be reached at roughly the same time as before the rules changed, the balance sheet of the Eurosystem will be bigger at that time thanks to the increase in eligible debt.

Figure 4 shows our projections for the second scenario, in which only central government debt securities issued after 1 January 2013 are assumed to contain CACs. The limits will be reached later than in scenario 1, as can be seen easily by comparing figures 2 and 3. For example, while in scenario 1, purchases in Germany are heavily constrained after April 2017, this is not the case until March 2018 in scenario 2.

On 21 January 2016, President Draghi hinted at further easing, given “downside risks” related to heightened uncertainty about the growth prospects of emerging economies, volatility in financial and commodity markets, and geopolitical risks. While this further easing could come in the form of a further reduction in the deposit rate, which would increase the amount of debt eligible for purchase (provided that the yields on these securities do not fall excessively in the meantime), the Governing Council might also decide to increase the amounts purchased each month under the PSPP. The Eurosystem is currently purchasing €44 billion of agency and government debt per month, but this could be raised. In Figures 5 and 6 we show our projections of monthly purchases were the amounts purchased each month to increase from €44 billion to €64 billion in March 2016, in both scenarios. As is apparent, the limits in each country would be reached much more quickly. Under the more restrictive scenario 1, the limit in Germany, the country in which purchases are the highest, would be reached as soon as November 2016. An increase in monthly purchases might be desirable to provide immediately a more accommodative stance to the euro area’s monetary policy in order to reach the inflation target, but it might not be compatible with a longer duration of the programme if the rest of the programme design remains unchanged.

Figure 2: Projection of monthly purchases (€ billion) per country with original rules (excluding national agencies) from Claeys et al (2015b)

Sources: Bruegel based on ECB, NCBS, National Treasuries, Datastream. Note: Luxembourg, Lithuania and Estonia do not appear on this chart given the very small amount of debt securities of these countries in the market.

Figure 3: Projection of monthly purchases (€ billion) per country, including national agencies (scenario 1: all debt securities contain CACs)

Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters.

Figure 4: Projection of monthly purchases (€ billion) per country, including national agencies (scenario 2: only central government debt issued after the 1st of January 2013 contains CACs)

Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters.

2.4 What could be done to further extend the duration of the programme if necessary?

Claeys et al (2015b) already recommended that the ECB increase the 25 percent issue limit to address the constraint that it would place on the size and duration of the PSPP. Claeys et al (2015b) also recommended that the list of eligible agencies be broadened. These changes have been put in place since March 2015, but that might not be enough to increase the pool of eligible assets. That is why Claeys et al (2015b) also recommended waiving entirely the issue limit, at least for AAA-rated bonds. This would allow, for instance, longer purchases of German sovereign bonds or European Investment Bank bonds.

The composition of the purchases could also be further altered. As already discussed at length in Claeys et al (2014), there are other types of assets that the Eurosystem could purchase if the ECB QE programme needs to be enhanced to bring inflation back to target. This could lengthen the duration of asset purchases, and increase the monthly monetary stimulus.

The Eurosystem could purchase senior well-rated uncovered bank bonds. While they are riskier than the covered bank bonds which are already being purchased under the CBPP3, the comprehensive assessment carried out by the ECB and national supervisors in 2014 and 2015 should theoretically ensure that euro-area banks are adequately capitalised and can smoothly absorb financial shocks. According to the ECB, there is currently more than €2 trillion of uncovered bank bonds which are eligible as ECB collateral10 (the Eurosystem collateral eligibility framework is not exactly similar but is roughly comparable to the eligibility criteria of assets for purchase, except for instance in terms of accepted maturity and minimum yield).

Another possibility would be for the Eurosystem to purchase corporate bonds, of which there are almost €1.5 trillion eligible for collateral purposes (although part of these are not euro-denominated, or are issued by corporates outside the euro area, in which case they should not be eligible).

Purchases of these securities might have different, or even complementary, effects, as explained in Claeys et al (2014). However, they could help the Eurosystem provide a stronger monetary accommodation for a longer period, and delay worries that the QE programme would reach its limits before the path of inflation is consistent with the inflation target.

Finally, the ECB Governing Council could also decide to change the way purchases are spread across euro-area countries, in order to shift some of the purchases from countries in which the limit will be binding (eg in Germany by the Bundesbank) to other national central banks. The first major country in which the limits will be reached is Germany, because the amounts purchased in each country are proportional to the country’s capital subscription to the Eurosystem, of which Germany is the largest, while there is proportionally much less outstanding debt in Germany than in Italy, for example. Distributing the purchases across countries according to their outstanding debt instead of distributing them according to the ECB capital keys would lead to limits being reached in every country at roughly the same time11. Given the various channels through which asset purchases can influence monetary conditions and thereby economic activity and prices, changing the country distribution of purchases could alter the effects of QE in the euro area12, which should be carefully taken into consideration by the Governing Council, were it to take this decision.

Figure 5: Projection of monthly purchases (€ billion) per country, including national agencies, if amount purchased is increased to €64 billion (scenario 1: all debt securities contain CACs)

Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters. Note: see note to Figure 3.

Figure 6: Projection of monthly purchases (€ billion) per country, including national agencies, if amount purchased is increased to €64 billion (scenario 2: only central government debt issued after 1 January 2013 contains CACs)

Source: Bruegel based on ECB, NCBs, National Treasuries, Thomson Reuters. Note: see note to Figure 3.

3. Potential risks related to unconventional monetary policy

The unconventional and previously untested nature of these policies poses some legitimate questions regarding their potential adverse consequences for financial stability, inequality and in terms of the credibility of the ECB.

3.1 Risks for financial stability

The ECB’s asset purchase programme, combined with the other unconventional monetary measures implemented since 2008 to avoid a full-scale liquidity crisis in the banking sector and the break-up of the euro area, contributes to an accommodative monetary policy stance. Cuts to the central bank rates to close to or even below zero, large-scale asset purchases, long-maturity lending to banks and forward guidance lead to loose monetary conditions that should stimulate growth and bring inflation back towards the 2 percent target. By increasing inflation and output (and therefore public debt sustainability), these measures should benefit financial stability. However, prolonged accommodative monetary policies could also pose some challenges to financial institutions and might have adverse consequences through various channels for financial stability.

One of the purposes of monetary policy is to support the economy by encouraging more risk-taking at a time when risk-taking in the financial system is less than socially desirable. However, if risk-taking becomes excessive and goes beyond what is socially desirable, it might contribute to future financial instability. It is very difficult to say when risk-taking becomes excessive, but as discussed in Claeys and Darvas (2015), banking indicators do not suggest substantially-increased risk-taking over the last six years and show on the contrary a clear tightening of credit standards in the euro area, while bank leverage has declined significantly, which should reduce the risks to financial stability. Bank regulation, stricter supervision and market pressure might have played an important role in limiting financial-sector leverage.

Increases in asset prices disconnected from fundamentals are also often mentioned as a potential side effect of QE programmes. However, while it is true that stock-market indices have been trending higher throughout the world over the last few years, simple equity valuation indicators do not suggest any obvious bubbles. The same appears to be true for housing prices in the euro area14.

QE programmes are also accused of threatening financial stability by reducing the profitability of financial institutions. For instance, some life insurance companies in the euro area have liabilities with longer maturities than their assets and are thereby exposed to a decline in interest rates given the guaranteed returns they promise to clients15. But it also appears that non-life insurance activities are expected to perform well in the coming years, which might compensate for the declining profitability of life insurance, which is often provided by the same companies. Moreover, as argued by President Draghi in January 201616, even if the ECB monitors the impact of its low rate policy on financial stability, the ECB’s mandate is not per se to ensure the profitability of any particular financial institution, especially if the decline in profitability of this institution arises from an unsustainable business model based on a peculiar maturity mismatch17.

Should monetary policy target financial stability explicitly? The global financial crisis has demonstrated that price stability in itself is not sufficient to ensure financial stability. Bubbles and boom-bust credit cycles emerged and eventually led to very high costs in terms of reduced output and unemployment in several advanced countries. A broad consensus has emerged that financial stability issues should be addressed ex ante. However, there is no consensus on the role of monetary policy in supporting financial stability. In our view, monetary policy tools are not well suited to tame financial excesses when the financial cycle deviates from the economic cycle or when financial cycles in euro-area countries differ. Monetary policy should focus on its primary mandate of area-wide price stability. Micro-prudential supervision, macro-prudential supervision, fiscal policy and regulation are the keys to mitigating financial stability risks. It is still too early to judge the effectiveness of the new European frameworks for micro- and macro-prudential supervision. The literature assessing these tools in other jurisdictions has produced some encouraging results, but the complex European set-up could make their implementation less effective.

Overall, as assessed by Claeys and Darvas (2015), the benefits of unconventional monetary policy measures including large-scale asset purchases seem to outweigh their potential risks to financial stability. The ECB should nevertheless be vigilant and be aware of the potential financial stability consequences of its monetary policy actions. Prudential policies, to which the ECB will now contribute via the Single Supervisory Mechanism and the European Systemic Risk Board, should be implemented forcefully in order to create a first line of defence in addressing financial stability concerns and avoiding the build-up of financial imbalances in the euro area.

3.2 Distributional effects of QE

The increase in income and wealth inequality observed in many advanced countries in recent decades is a long-term trend and primarily the result of deep structural changes, including skill-biased technological change, globalisation, demographics, institutional and political changes and, in particular, changes to fiscal, educational and labour institutions. Nevertheless, there are some concerns that QE programmes could amplify this trend, at least in the short and medium terms.

Through increases in financial asset prices, central bank asset purchases could increase inequality between the wealthy and poor, between the young and old, and also between regions when they have different financial structures. Increases in the value of assets such as equities and government and corporate bonds will tend to favour the rich who have greater holding of them, as illustrated in Claeys et al (2015a) using the ECB's Household Finance and Consumption Survey (2013). Because older people tend to have higher savings and might sell them in the future in order to maintain their consumption, while younger households will usually buy these assets in the future in order to save for retirement, QE programmes might have distributional consequences across generations. QE can also benefit households differently depending on the structure of their financial assets, since certain households could make better use of the opportunity offered by low-interest rate borrowing than others.

However, QE programmes could also reduce inequality through an increase in (or at least a stabilising effect on) housing prices and a fall in interest rates. Housing is the main asset of the middle class19 and therefore house price increases will tend to compress the wealth distribution. Falls in mortgage interest rates also tend to benefit people with lower incomes who spend a greater share of their income on servicing their debts.

Likewise, the stimulative effects that unconventional monetary policy has on the economy tends to reduce inequality. The empirical literature suggests that asset purchase programmes tend to boost inflation, output and employment. In the absence of these policies, unemployment would thus be higher, which would lead to higher income inequality because the poor and low-skilled are the most likely to lose their jobs in recessions and because wages are the primary source of revenue for poorer and lower-income people.

The ECB’s primary mandate is to maintain price stability, and considerations of inequality are not within its purview, unless inequality prevents the transmission of monetary policy in some way. The ECB should therefore focus on its price stability mandate by supporting the fragile recovery now taking place in the euro area. This is the best way for monetary policy to contribute to the avoidance of an increase in inequality.

Another important policy question is how to tackle inequality in general, and whether governments should design special measures in a deep recession or in a situation in which central bank actions increase inequality. For example, in the United States, policies such as the Home Affordable Refinance Programme, which helped homeowners with negative home equity to refinance their mortgages, might have helped dampen the rising inequality that resulted from the housing slump. Fiscal and social policies are the right tools to fight inequality. As documented by Darvas and Wolff (2014), there are huge differences in the efficiency of social redistribution systems in EU countries. For their levels of social expenditure and personal income taxes, several southern European countries and Belgium achieve a much smaller reduction in inequality than other EU countries. Revising national tax/benefit systems for improved efficiency, intergenerational equity and fair burden-sharing between the wealthy and the poor is the right way to fight inequality.

3.3 Credibility risks for the ECB

The primary mandate of the ECB is to ensure price stability in the euro area, and the ECB’s credibility is based on fulfilling this mandate. If inflation deviates significantly from “below but close to 2 percent” for a prolonged period of time, expectations might start to deviate as well, and companies and households might start making decisions concerning wages and prices with a different inflation anchor in mind, which could be very dangerous given the self-fulfilling nature of inflation expectations. Since the beginning of 2013, inflation has been trending well below its target and expectations have started drifting downwards as a result. The ECB has thus not been fulfilling its mandate and is therefore at risk of losing its credibility.

On the contrary, the fear that the ECB will lose its credibility because of the significant amount of sovereign bonds it is currently buying appears to be unfounded for several reasons. First, it is true that if inflation was running well above the 2 percent target and that the ECB was buying sovereign bonds with the sole objective of easing financing conditions on government debts despite the fact that it could drive inflation further above the target, then the ECB could easily lose credibility and put itself in a very dangerous situation. However, the current situation is the opposite. Inflation is currently very low and the ECB needs to avoid at all costs that the inflation expectations of euro-area citizens and companies become disanchored. Without the option of easing monetary conditions further through rate cuts, the ECB had to resort to QE, like every other major central bank, in order to provide the necessary accommodation to fulfil its mandate.

Second, since the launch of the PSPP, the ECB Governing Council has been very careful to avoid breaching the prohibition of monetary financing included in the EU Treaty. The 25 percent issue limit for bonds containing CACs is there to prevent the ECB from having “a blocking minority in a debt restructuring involving collective action clauses” (ECB, 2015). This clearly indicates that the ECB does not want to be in a position in which it would have the power to block a potential vote on the restructuring of the ECB-held debt of a euro-area country, because not blocking such a restructuring could be interpreted as monetary financing of a member state. On the contrary, if a majority of creditors with collective action clauses would accept a restructuring of some bonds, the ECB could do nothing against such a restructuring and would have to accept it. Because it would not be voluntary, it would not be considered as monetary financing and would therefore not be in contradiction with the EU Treaty.

In our view, the problem is that the ECB has been so careful to avoid the possibility of monetary financing ex ante that it has put the operational implementation of its QE programme at risk by constraining it too much, as detailed in section 2. The ECB should instead try to balance both the risk of breaching the monetary financing prohibition and the risk of not fulfilling its mandate because of the limits imposed on its own QE programme. For instance, the risk of monetary financing of an AAA-rated government such as Germany’s appears to be currently negligible and should not act as a constraint on the full implementation of the programme and the achievement of the ECB’s mandate. We therefore renew our recommendation to the ECB to waive the 25 percent limit, at least for well-rated countries, in order to facilitate the implementation of its QE programme.

4. Conclusions

The sovereign quantitative easing programme of the ECB finally started in 2015. This decision was welcome given the clear downward trend in inflation and the feeble recovery of the euro area in the last few years.

Nevertheless, in a monetary union such as the euro area, with multiple sovereign debt securities, the execution of such a programme is very complex. The ECB Governing Council imposed limits to ensure ex ante that the ECB would not breach the prohibition of monetary financing. However, our updated calculations show that these limits will constrain the duration and size of the programme throughout 2017, even when taking into account the changes announced throughout 2015, and especially if the ECB decides to increase its monthly purchases. We recommend that the ECB further alter the programme guidelines. Changes could include the purchase of corporate bonds as well as senior well-rated uncovered bank bonds. A more radical change would be to move away from an allocation of asset purchases between countries based on the ECB capital keys, to an allocation based on the actual size of countries’ outstanding debts.

Additionally, the extension of the QE programme raises some legitimate questions on its potential adverse consequences. In our assessment, the benefits outweigh the potential negative implications, for instance for financial stability or for inequality. Central banks should of course be aware of the potential side effects of their actions (which are generally temporary), but issues of financial stability and inequality are mainly the result of deep structural changes, and therefore other policies remain essential to deal with them. Micro and macro-prudential policies should constitute the first line of defence to avoid the build-up of financial imbalances, while fiscal and social policies are the right tools to fight the current rise in inequality in advanced countries.

References

Baumeister, C. and L. Benati (2010) ‘Unconventional monetary policy and the great recession Estimating the impact of a compression in the yield spread at the zero lower bound’, Working Paper Series No 1258, European Central Bank

Claeys G., Z. Darvas, S. Merler and G. Wolff (2014) ‘Addressing Weak Inflation: the ECB’s Shopping List’, Policy Contribution 2014/05, Bruegel

Claeys G. and Z. Darvas (2015) ‘The Financial Stability Risks of Ultra-loose Monetary Policy’, Policy Contribution 2015/03, Bruegel

Claeys G., Z. Darvas, A. Leandro and T. Walsh (2015a) ‘The Effects of Ultra-loose Monetary Policy on Inequality’, Policy Contribution 2015/09, Bruegel

Claeys G., A. Leandro and A. Mandra (2015b) ‘European Central Bank Quantitative Easing: the Detailed Manual’, Policy Contribution 2015/02, Bruegel

Darvas Z. (2016) ‘Oil prices and inflation expectations’, Bruegel Blog, 21 January

Darvas Z. and P. Hüttl (2016) ‘Has ECB QE lifted inflation?’ Bruegel Blog, 12 January

Darvas Z. and G. B. Wolff (2014) ‘Europe's social problem and its implications for economic growth’, Policy Brief 2014/03, Bruegel

Diamond D. and P. Dybvig (1983) ‘Bank runs, deposit insurance, and liquidity’, The Journal of Political Economy, 91(3)

Draghi, M. (2015a) ‘Introductory statement to the press conference (with Q&A) Frankfurt am Main, 22 January’, available at http://www.ecb.europa.eu/press/pressconf/2015/html/is150122.en.html

Draghi, M. (2015b) ‘Introductory statement to the press conference (with Q&A) Frankfurt am Main, 3 September’, available at http://www.ecb.europa.eu/press/pressconf/2015/html/is150903.en.html

Draghi, M. (2015c) ‘Introductory statement to the press conference (with Q&A) Frankfurt am Main, 3 December’, available at http://www.ecb.europa.eu/press/pressconf/ 2015/html/is151203.en.html

Draghi, M. (2016) ‘Introductory statement to the press conference (with Q&A) Frankfurt am Main, 21 January’, available at http://www.ecb.europa.eu/press/pressconf/2016/html/is160121.en.html

ECB (2013) Household Finance and Consumption Survey, available at https://www.ecb. europa.eu/home/html/researcher_hfcn.en.html

ECB (2015) Implementation aspects of the public sector purchase programme (PSPP), 5 March, available at http://www.ecb.europa.eu/mopo/liq/html/pspp.en.html

Kapetanios, G., H. Mumtaz, I. Stevens and K. Theodoridis (2012) ‘Assessing the Economy‐wide Effects of Quantitative Easing’, The Economic Journal, 122(564): 316-347

About the authors

Related content

What will it cost the European Union to pay its economic recovery debt?

Servicing the EU debt until 2058 seems feasible, despite increased borrowing costs, but member countries must make choices about budget funding

Inflation inequality in the European Union and its drivers

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition