The United States dominates global investment banking: does it matter for Europe?

Europe’s banks are in retreat from playing a global investment banking role, and this trend is likely to continue in the future. What will be the cons

Highlights

For the full references and the annex, please see the PDF version of this publication.

- In the aftermath of the global financial crisis, the market share of US investment banks is increasing, while that of their European counterparts is declining. We present evidence that US investment banks are on the verge of taking over pole position in European investment banking. Meanwhile, since 2015, Chinese investment banks have overtaken American and European investment banks in the Asia-Pacific market.

- Credit rating agencies and investment banks are the gatekeepers of the capital markets. The European supervisory institutions can effectively supervise the European operations of these US-managed players. On the political side, we suggest that the European Commission should continue to view its, albeit declining, banking industry as a strategic sector. The Commission, the European Central Bank and the Bank of England should jointly develop a strategic agenda for the EU-US Regulatory Dialogue.

- Finally, corporates rely on investment banks to issue new securities. We recommend that the big European corporates should cherish the (few) remaining European investment banks, by giving them at least one place in otherwise US- dominated banking syndicates. That could help to avoid complete dependence on US investment banks.

1. Introduction

Europe’s banks are in retreat from playing a global investment banking role. This should not be a surprise. It is an, often intended, consequence of the regulatory impositions of recent years, notably of the ring-fencing requirements of the Vickers Report (2011) and the ban on proprietary trading by Liikanen (2012), but also including the enhanced capital requirements on trading books and other measures. The main concern is that a medium-sized European country, such as the United Kingdom or Switzerland, or even a larger country like Germany, let alone a tiny country like Iceland or Ireland, would find a global investment bank to be too large and too dangerous to support, should it get into trouble1. So, one of the intentions of the new set of regulations was to rein back the scale of European investment banking to a more supportable level.

The European Union, of course, has a much larger scale than its individual member countries. If the key issue is the relative scale of the global (investment) bank and state that might have to support it, could a Europe-based global investment bank be possible2? We doubt it, primarily because the EU is not a state. It does not have sufficient fiscal competence. Even with the European banking union and European Stability Mechanism, the limits to the mutualisation of losses, eg via deposit insurance, mean that the bulk of the losses would still fall on the home country (Pisani-Ferry and Wolff, 2012). Moreover, there would be intense rivalry over which country should be its home country, and concerns about state aid and the establishment of a monopolistic institution. While the further unification of the euro area might, in due course, allow a Europe-based global investment bank to emerge endogenously, we do not expect it over the next half-decade or so.

So the withdrawal of European banks from a global investment banking role is likely to continue. That will leave the five US ‘bulge-bracket’ banks, (Goldman Sachs, Morgan Stanley, JP Morgan, Citigroup and Bank of America Merrill Lynch) as the sole global investment banks left standing. The most likely result is a four-tier investment banking system.

The first tier will consist of these five US global giants. The second tier will consist of strong regional players, such as Deutsche Bank, Barclays and Rothschild in Europe and CITIC in the Asia-Pacific region. HSBC is in between, with both European and Asia-Pacific roots. The third tier consists of the national banks’ investment banking arms. They will service (most of) the investment banking needs of their own corporates and public sector bodies, except in the case of the very biggest and most international institutions (which will want global support from the US banks) or in cases of complex, specialist advice. Examples of this third tier are Australian and Canadian banks, which support their own corporates and public sector bodies without extending into global investment banking. The fourth tier consists of small, specialist, advisory and wealth management boutiques.

Why should it matter if in all the European countries, the local banks’ investment banking activities should retrench to this more limited local role? After all, there are few claims that Australia and Canada have somehow lost out by not participating in global investment banking. We review the arguments in section 4. Before doing so, we take a closer look at the investment banking market in Europe. Section 2 investigates the development of the relative market shares of US and European investment banks over time. It appears that the US investment banks are about to surpass their European counterparts in the European investment banking market. Section 3 examines how the US investment banks operate in Europe. We find a typical pattern of a large London head office, where banks locate their financial experts, including traders, and small salesforces in major European capitals. We discuss the policy implications in section 5.

2. The rise of US and decline of European investment banks

2.1 The function of investment banks

Investment banks play a key role in financial markets by bringing together the suppliers of capital (ie investors) and those that require capital (ie corporates, governments and households). In this way, investment banks are the gatekeepers of the EU capital markets union. The European Commission, which initiated the capital markets union project as part of its strategy for the financial sector, has therefore a keen interest in the proper functioning of these gatekeepers from an economic perspective. But there is also a political dimension to the role of investment banks, as in the case of credit rating agencies. Would it be acceptable for the EU to rely on US players, for these important components of the financial system? We return to this in section 4.

On the demand side for capital, corporates make up the largest group3. The provision of corporate finance is the traditional métier of investment banks: helping customers raise funds on capital markets and giving advice on mergers and acquisitions (M&A). This may involve subscribing investors to a security issuance, coordinating with bidders, negotiating with a merger target and liaising with regulators (competition and financial regulatory authorities) and governments. One of the main roles of investment banks in M&A is to establish fair value for the companies involved in the transaction. They are also able to predict how that value could be altered (ie what happens to the value of a company in a number of different scenarios and what those potential futures would mean financially). A pitch book of financial information is generated to showcase the bank to a potential M&A client. If the pitch is successful, the bank arranges the deal for the client.

While investment banks used to underwrite almost all equity and bond issues, their role has now shifted to placing capacity with investors. So most placements are done on a best-efforts basis; only rights issues are still underwritten by the investment banks. Corporates pay for quality and reputation, which are the key ingredients for an investment bank’s success.

As both US capital markets and US corporates are by far the world’s biggest, it is no surprise that US investment banks are leaders in global investment banking. However, US investment banks on Wall Street have close ties with the US government in Washington DC, as witnessed during the global financial crisis. In this sector, the US Congress can easily pass new laws with extra-territorial reach (eg Sarbanes-Oxley). Next, we have seen episodes in which US banks and corporates were acting on stringent orders from Washington (such as over SWIFT4, Cuba, Iran). What if these orders turn against Europe? We leave that for Section 4.

2.2 The market shares of US and European investment banks in Europe

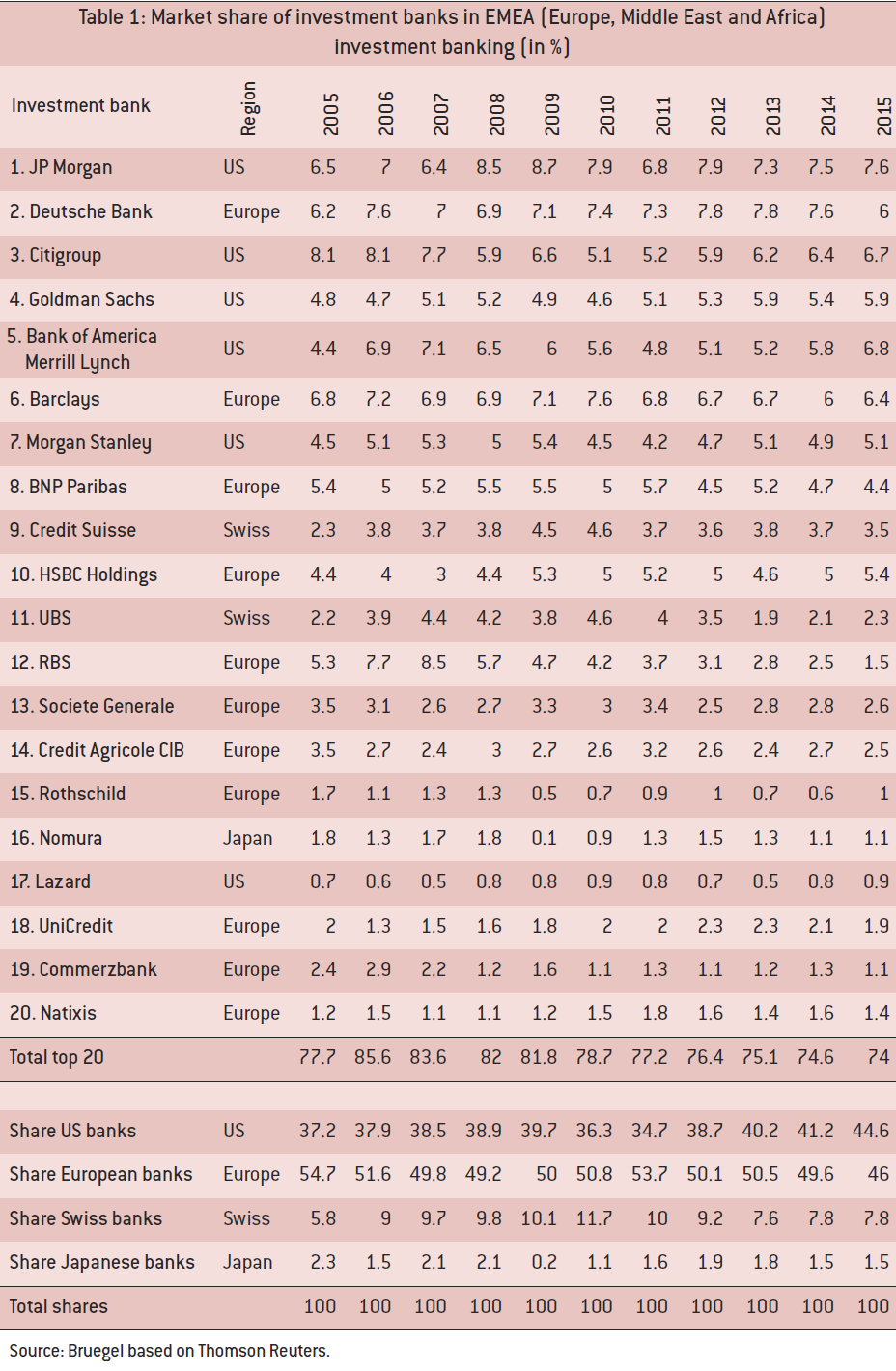

While the US investment banks are the global leaders, what is their share in the European investment banking market? The Thomson Reuters investment bank league tables rank investment banks by market share. These tables typically cover four major segments: M&A, equity, bonds and loans (ie syndicated loans). We have calculated the weighted average of investment banking proceeds of the top 20 players across these four segments for Europe (ie the market share in each segment is weighted by the relative size of that market segment in total investment banking business). Global data are usually split into Americas, EMEA (Europe, Middle East and Africa), Asia-Pacific and Japan, but we have only EMEA data. However, Europe comprises the vast majority of EMEA investment banking. Data is taken from Thomson Reuters and covers the period from 2005 to 2015. To select the top 20, we take the 11-year average across all investment banks, and use that ranking for all years.

Table 1 provides the detailed market shares of the top 20 investment banks. It appears that the top 20 covers about 80 percent of the EMEA investment banking market. Figure 1 summarises the results. The market share of EU and Swiss investment banks has declined since 2010/11, while the share of US investment banks (the big five and Lazards) increased from 35 percent in 2011 to 45 percent in 2015. It should be noted that the evolution of the regional market shares reflects partly the broader banking crisis dynamics. US investment banks were the first to be hit in the global financial crisis and declined from 40 percent in 2009 to 35 percent in 2011, but recovered after the decisive recapitalisation exercise enforced by the US Treasury. The Swiss decline set in in 2010 and the EU decline in 2011. However, the European share of the investment banking market remains significant. While the European banks lose business in the global investment banking market (Figure 2), they have still a strong, albeit declining, presence in Europe, serving the many smaller and mid-sized corporates.

Nevertheless, Figure 1 shows an underlying structural trend, whereby EU and Swiss investment banks are downsizing. If the trend were to continue, US investment banks would take the prime spot from their EU counterparts soon, possibly already in 2016.

Figure 1: Investment banks by origin, EMEA market shares (%)

Source: Bruegel based on Thomson Reuters.

Note: The figure depicts the relative shares of the EMEA investment banking market held by the top 20 investment banks, grouped by origin (EU, US, Switzerland, Japan). Europe comprises the vast majority of EMEA investment banking.

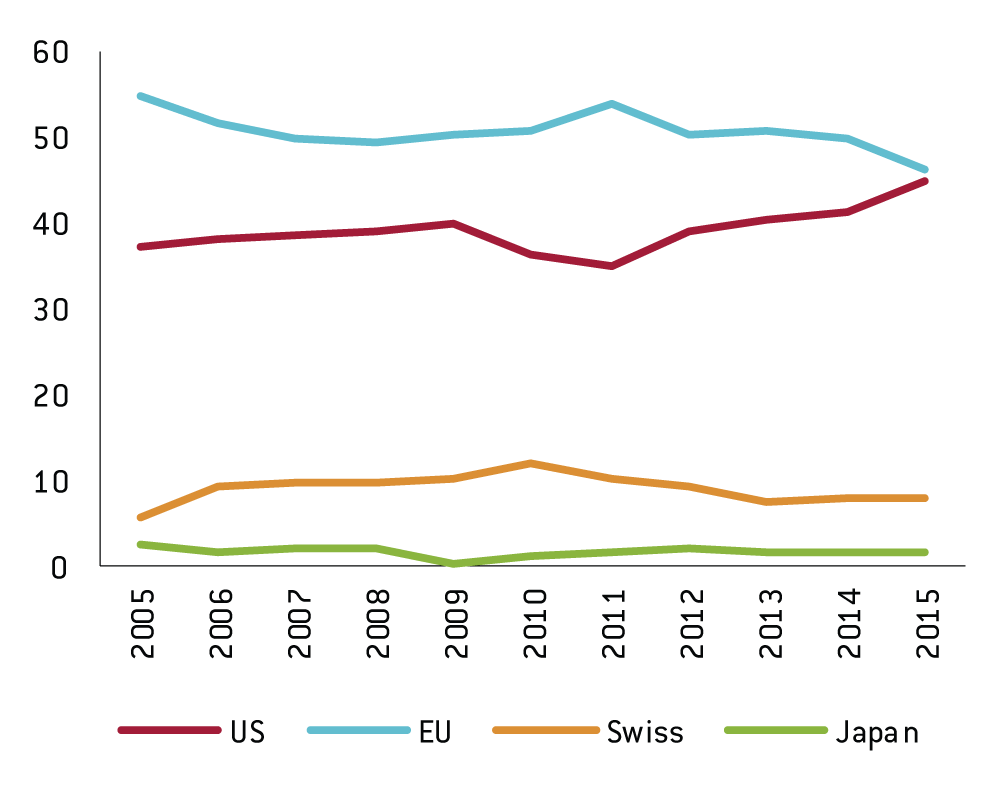

2.3 Global investment banking

To complete our picture of investment banking, we have also calculated the market shares for global investment banking and in the other major regions. For these calculations, we have taken market shares by investment banking fees. Data is again taken from Thomson Reuters, but is only available from 2010 onwards. Figure 2 shows that the share of American (US and Canadian) investment banks increased from 58 percent in 2010 to 62 percent in 2015, while the share of European (EU and Swiss) banks decreased from 35 to 30 percent over the same period. This confirms the general picture of the rise of American investment banks and the decline of their European counterparts.

Figure 2: Investment banks by origin, global market shares (%)

Source: Bruegel based on Thomson Reuters.

Note: The figure depicts the relative shares of the global investment banking market held by the top 20 investment banks, grouped by origin (Americas (US and Canada), Europe (EU and Swiss) and Asia-Pacific (Japan)).

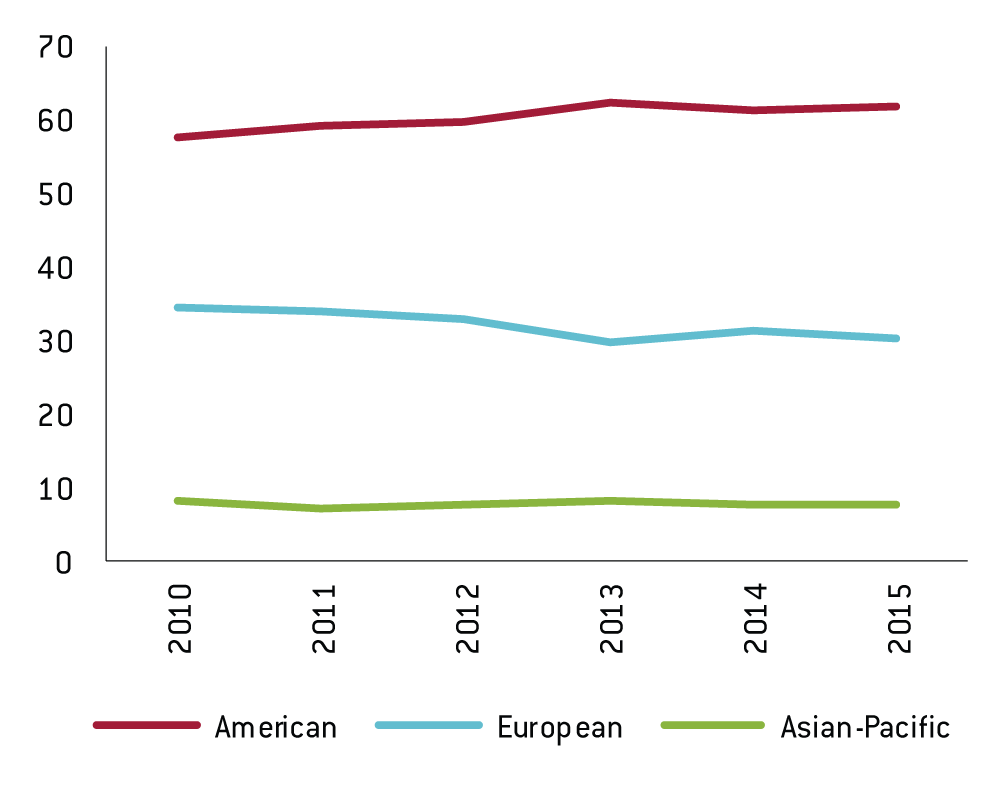

Figure 3: Investment banks by origin, shares of the American market (%)

Source: Bruegel based on Thomson Reuters.

Note: The figure depicts the relative shares of the American investment banking market held by the top 20 investment banks, grouped by origin (US, Canada, Europe (EU and Swiss) and Asia-Pacific (Japan)).

Turning to the Americas, the increasing share of the US investment banks is even more evident. Figure 3 shows that the relative share of the American investment banking market held by the US banks from among the top 20 has risen from 63 to 66 percent, while the European share has declined from 28 to 22 percent. This is in line with the broader retreat of European banks from the US. It should be noted that before the global financial crisis, the European banks had an overly large presence in the US; so there was a bias towards the US in the foreign operations of European banks (Schoenmaker and Wagner, 2013). From the Asia-Pacific region, only the Japanese investment banks operate on a global scale. While the Chinese investment banks are on the rise, they have confined themselves so far to a local role.

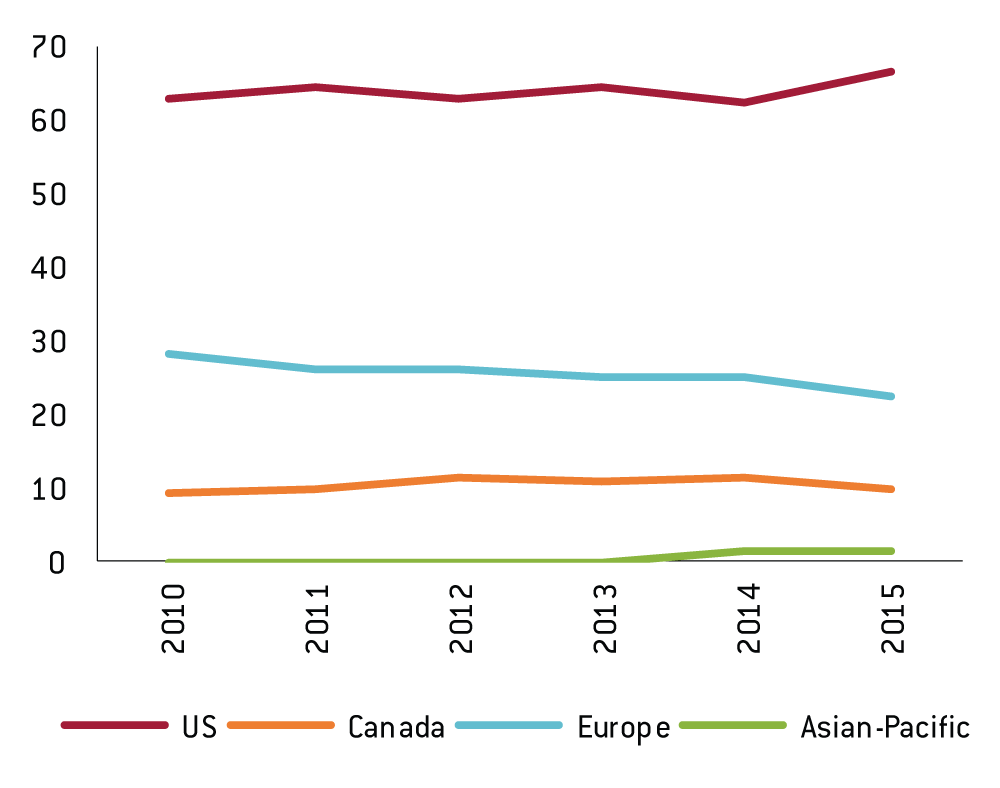

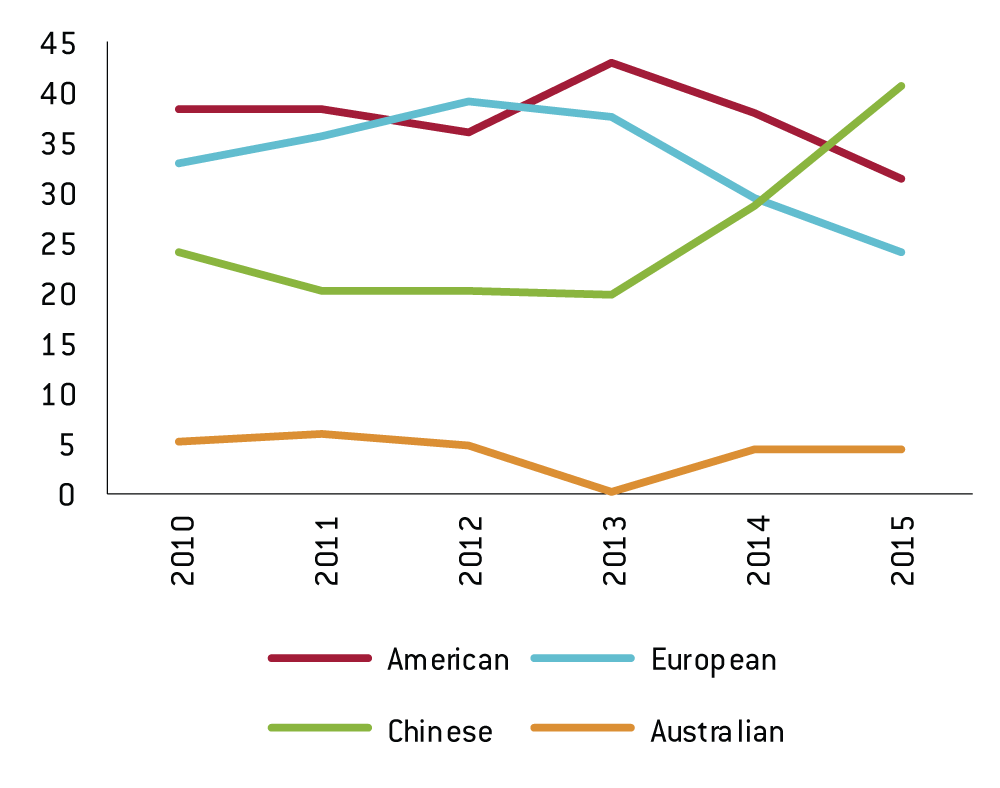

Finally, we analyse the Asia-Pacific and Japanese investment banking market. These are separately calculated by Thomson Reuters. Figure 4 shows some significant and interesting trends. The shares of the Asia-Pacific market held by US and European investment banks have tumbled over this short period. US investment banks have dropped from 38 to 31 percent and European banks from 33 to 24 percent. The Chinese investment banks have now become the largest players in their own region, with a market share of 41 percent in 2015. This reflects the increasing professionalism and self-confidence of Chinese investment banks. These local investment banks are also better placed to understand, and liaise with, the Chinese corporates, regulators and party/government.

HSBC Group is a global bank, with a strong presence in Europe (42 percent of its total loan book) and Asia (37 percent of its total loan book). Moreover, the Hongkong and Shanghai Banking Corporation (the Hong Kong subsidiary of HSBC Group) is the largest bank in Hong Kong. It would be interesting to see whether it conforms to the declining path of the European banks or the rise of the Chinese banks. The market share of HSBC in Asia-Pacific investment banking rose from 1.7 percent in 2010 to 2.9 percent in 2015. While HSBC is ranked under European banks (because its headquarters are in London), it thus follows the pattern of Chinese investment banks supplanting their US and European counterparts.

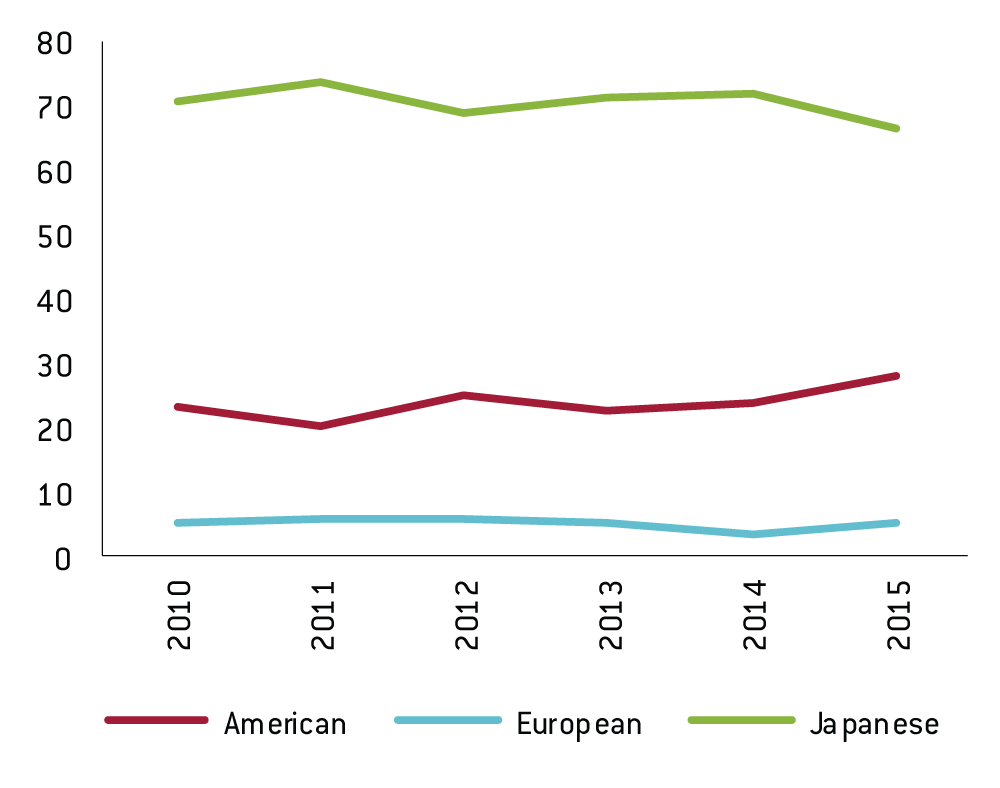

Figure 5 shows the Japanese investment banking market. It highlights the traditionally relatively closed nature of the Japanese banking market, with a more than 70 percent market share for domestic banks. Nevertheless, there is a decline in the market share of the Japanese investment banks from 71 percent in 2010 to 67 percent in 2015. This part of the market has been taken over by the American investment banks, which increased their market share from 24 to 28 percent during this period.

Figure 4: Investment banks by origin, Asia-Pacific market shares (%)

Source: Bruegel based on Thomson Reuters.

Figure 5: Investment banks by origin, shares of Japanese market (%)

Source: Bruegel based on Thomson Reuters.

Note: The figure depicts the relative shares of the Japanese investment banking market held by the top 20 investment banks, grouped by origin (Americas (US and Canada), Europe (EU and Swiss) and Japan).

While the Chinese and Japanese investment banks are the dominant players in their own markets, these markets are far smaller than the American and EMEA investment banking markets. Thomson Reuters (2016) provides data on total investment banking fees for the various geographical regions: Americas $48.6 billion; EMEA $22.1 billion; Asia-Pacific $12.6 billion; and Japan $3.6 billion in 2015. This reconfirms the overall picture that the five US investment banks are the global leaders, with leading positions in the major American and European markets (see also Figure 2).

3. How do US investment banks operate in Europe?

An interesting question is how the US investment banks operate across Europe. That is difficult to answer because investment banks, like any large corporates, are not very transparent about the precise geographical location of their operations. But under the recent EU Capital Requirements Directive (CRD IV), financial institutions must disclose, by country in which they operate through a subsidiary or a branch, information about turnover, number of employees and profit before tax. These so-called country-by-country (CBC) reports allow us to refine the geographical split at country level. From the 2014 CBC reports of the five US investment banks, we take the investment banking activities across Europe and exclude the commercial banking activities of Citi, Bank of America and JP Morgan Chase. In two cases (Citigroup, JP Morgan), some EU countries are not covered in the main CBC reports. We use additional documents for these banks5.

3.1 The hub and spoke model

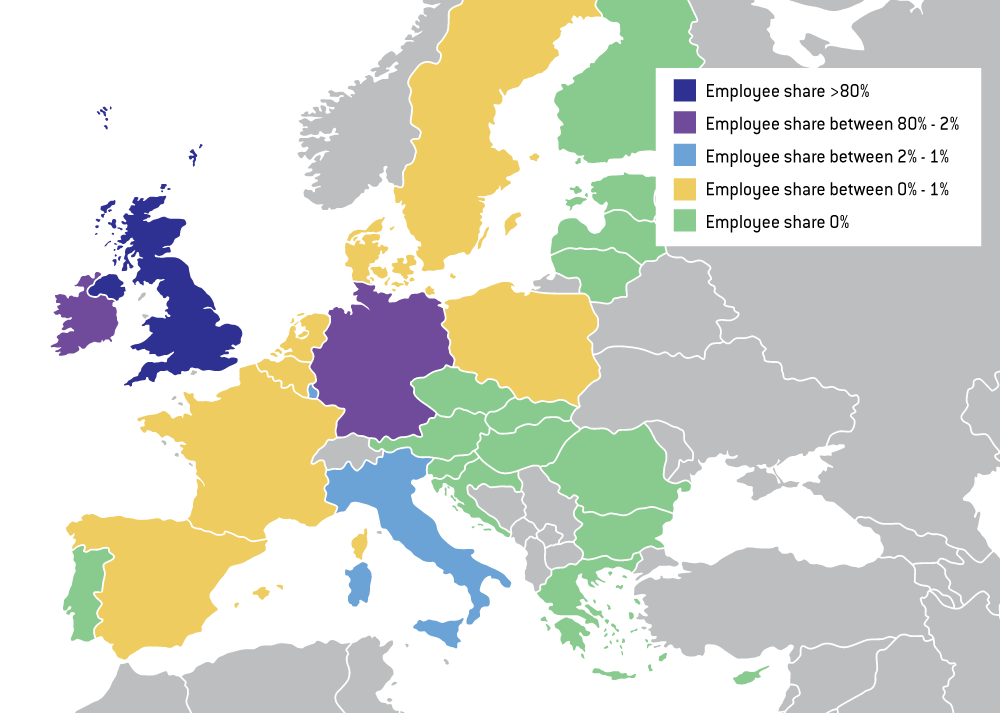

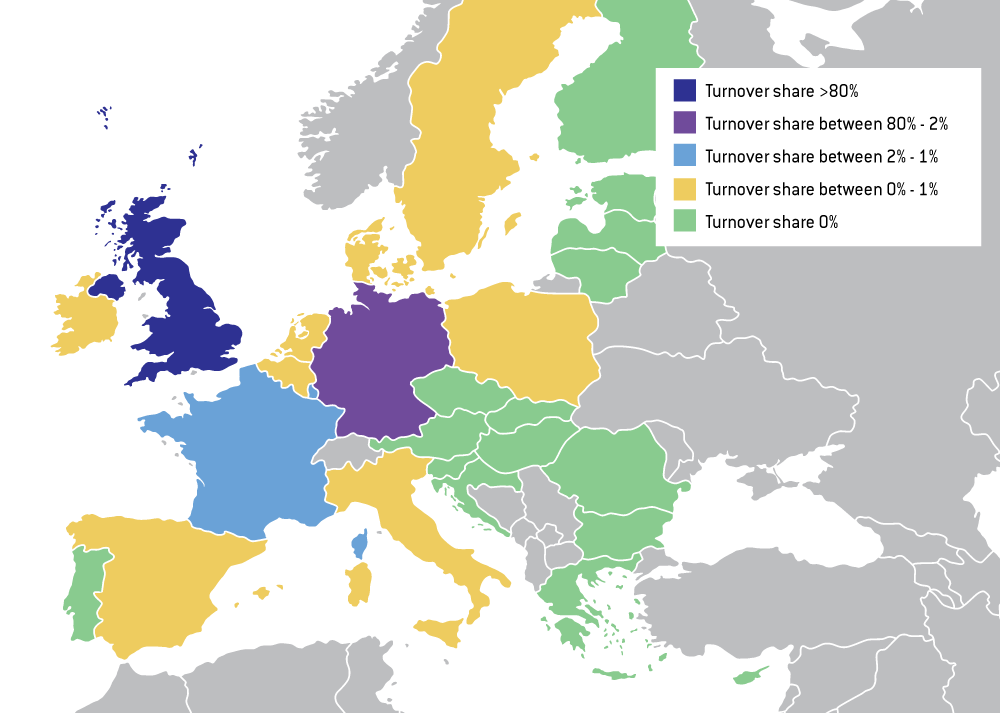

Tables A1 and A2 in the annex contain a detailed breakdown of turnover and employees in 2014 for the five US investment banks. Figures 6 and 7 illustrate the aggregate breakdown for the five banks. The figures show how the US investment banks apply the hub and spoke model in their European operations. These banks use the international financial centre of London as their main hub (with more than 80 percent of business) with spokes radiating out to the other larger and mid-sized European countries. They have no operations in the smaller markets, such as Austria, Finland, Portugal and the Baltic States. In central and eastern Europe, they have only a small presence in the largest country, Poland.

A few capitals act as sub-hubs. Frankfurt and Dublin are the larger sub-hubs with more than 2 percent of business. Frankfurt has emerged as the financial capital of the euro area. The rise of Frankfurt can be explained by the presence of the European Central Bank, which has expanded from monetary policy towards banking supervision. Moreover, Frankfurt is the financial capital of Germany, the largest and strongest European country, which reinforced its dominant position during the euro sovereign crisis. By contrast, Dublin is located in one of the smaller countries, but has a favourable tax regime and belongs, together with the United Kingdom, to the group of English-speaking countries. Americans might find it easier, also culturally, to set up office (and home) in these countries. Finally, Luxembourg and Paris are smaller sub-hubs with more than 1 percent of business.

So, the large London head office contains the vast majority of an investment bank’s financial experts and traders, with some further specialists based in Frankfurt and/or Dublin. The investment banks have small salesforces in the other main European capitals. These account managers speak the local language and liaise between the London experts and local clients, who might prefer to do business with their fellow countrymen. An interesting detail is that the US investment banks actively attract financial talent from across Europe to ensure that the main nationalities (and cultures) are present in their London teams, and can also move into senior positions6. Appointing Europeans to key positions helps in liaising with European corporates, investors, regulators and governments, which is an important part of the investment banking function.

The hub-and-spoke model is reinforced by the drive towards regulatory efficiency. The US investment banks prefer to deal with one regulator for their European operations. That is obviously the regulator in the main hub. For prudential matters, the Bank of England’s Prudential Regulatory Authority has the supervisory power under the Second Banking Directive (89/646/EEC) over the European operations of the US investment banks. The UK licence can then be used as a passport throughout the European Union. Similarly, the UK Financial Conduct Authority supervises the market operations under the Markets in Financial Instruments Directive (2004/39/EC; shortly to be replaced by MiFID II (2014/65/EU)), and offers a European passport for these activities. Insofar as the US investment banks have additional subsidiaries across the EU, the respective country supervisors (eg ECB/Bafin for Citigroup Global Markets Deutschland AG) have supervisory control over these subsidiaries.

Figure 6: US investment banks, segmentation of turnover across the EU (2014)

Source: Bruegel based on country-by-country reports of the 5 US investment banks.

Figure 7: US investment banks, segmentation of employees across the EU (2014)

Source: Bruegel based on country-by-country reports of the 5 US investment banks.

3.2 Consequences of Brexit

Our analysis shows that London is not only an international financial centre, but also a gateway to Europe for the large US and Swiss investment banks. These banks use their UK banking licence(s) as passports for their operations throughout the European Union. That might no longer be possible in the unfortunate case of a UK exit from the EU. Although various alternative scenarios (from a ‘Norway’ deal to a loose free trade pact) can be postulated, investment banks have an overriding interest in safeguarding their European passport. A vote for Brexit in the UK’s 23 June 2016 referendum would be the starting point for negotiations between the United Kingdom and the European Union on a new cooperation model. Such negotiations could easily last several years, with lingering uncertainty about the outcome during this period. Investment banks hate uncertainty. Moreover, their clients want to know what to expect (for example, under which law their securities are issued). So, investment banks are making preparations for the relocation of their business, or parts of their business, and their regulatory passports, if needed in the case of Brexit.

Speculation is already starting about whether the investment banks might move their European head offices to Frankfurt, Dublin, Paris or the outsider Amsterdam. In the aftermath of the global financial crisis, Ireland would not be very keen to host these large banks. Hosting banks brings not only benefits (eg employment and taxes), but also costs in the form of a fiscal backstop to the banking system (Schoenmaker, 2015). The latter can in particular be costly for small countries.

The US investment banks are happy with their current presence in London; HSBC also recently confirmed it would stay in London and not relocate to Hong Kong. The Anglo-Saxon culture, in terms of both the free-market driven business culture and private residence, suits them well. It is no surprise to see that the US investment banks are vocally in favour of the UK staying inside the European Union7. In contrast, some London-based hedge funds campaign for Brexit. The volatility following a Brexit could be a fertile trading ground for hedge funds. Moreover, a United Kingdom outside the European Union might be less (over)regulated. These hedge funds perhaps guess, rightly or wrongly, that the United Kingdom will strike a trade deal with the European Union after a potential Brexit. But the more such a deal resembles the Norwegian membership of the European Free Trade Association with passport rights into the European Union, the more the UK will have to continue to adopt the full regulatory acquis of the European Union. The only difference is that the United Kingdom would have no voting seat at the negotiation table for new directives and regulations8.

4. Concerns for Europe

We now turn to the consequences of the rise of US investment banks and the decline of their European counterparts. Why should it matter if in all the European countries, the local banks’ investment banking roles retrench to a more limited local role? After all, there are few claims that Australia and Canada, which are largely served by local banks, have somehow lost out by not participating in global investment banking.

4.1 Regulatory dialogue

There are, perhaps, three inter-related arguments why leaving global investment banking to the big five American banks might be problematic. The first is that this could leave Europe at greater risk from possibly ill-advised American political or regulatory intervention. Oudéa (2015), wrote that:

“In the last crisis, American banks came under intense pressure to reduce their European assets. Having banks able to finance European companies is an essential part of the EU’s economic sovereignty. Europe’s industrial champions will be at a serious disadvantage if they cannot rely on access to capital when their rivals in America and China can.”

While this danger exists, it was already present before the withdrawal of European banks from global investment banking. Since the US dollar and US financial markets play the central role in the financial system, the US is in a position to enforce its demands on acceptable counterparty transactions and to dominate, for good or ill, the international monetary policy scene, whether or not the big five US banks are the only global ‘bulge-bracket’ banks left standing.

As we have discussed, Washington has had no problem enacting far-reaching regulations, such as Sarbanes-Oxley for corporates, or the leverage ratio for banks operating in the US (pre-Basel 3). In the aftermath of the Enron debacle, US Congress enacted strong corporate governance rules (ie the Sarbanes-Oxley Act of 2002), which applies to all companies (both domestic and foreign) listed in the US. The usual practice is that companies can follow the corporate governance rules of their primary listing, often in the country where they are headquartered. If they subsequently get a secondary listing in another market, they do not have to follow these rules. However, the US decided that European (and other foreign) corporates with a secondary listing in New York had to follow the new Sarbanes-Oxley rules. A controversial requirement was that CEOs and CFOs have to sign off on the accounts. While this rule was strongly resisted by the foreign executives, the US enforced the rule for all listed companies.

Similarly, the European Commission started to put clauses in directives to give themselves the powers to recognise or not the equivalence of US, Swiss and other countries’ regulation and supervision (eg in the Financial Conglomerates Directive). The European Commission and the US authorities therefore set up an EU-US Regulatory Dialogue to discuss bilateral regulation issues9. In some cases, the parties reached consensus (eg exemption of European banks from the leverage ratio for their operations and recognition of US prudential regulation and supervision as equivalent for financial conglomerates). In other cases, there is no consensus. A case in point is the accounting rules. While Europe adheres to the IFRS (International Financial Reporting Standards), the US sticks to its US GAAP (General Accepted Accounting Principles)10.

A recent issue in the bilateral dialogue is the new US requirement for an Intermediate Holding Company (IHC) for large US operations (with more than $50 billion of assets) of foreign banks. In that way, the US Federal Reserve can exercise full control over the US operations of European (and other foreign) banks. By requiring separate capitalisation of the US operations, the rule could reduce bank profitability at the parent level and induce organisational changes.

4.2 Competition

Five is not a large number. So, the second argument is that this will leave global investment banking much more concentrated. Is this not potentially dangerous? Perhaps, but these five banks still compete quite ferociously, so margins are not rising all that much. The current economic pressures, especially of much greater capital requirements, impact on the US banks just as much as on European banks through the Basel 3 framework. What would happen if one, some or all of these US banks decided to follow the European banks and to withdraw from providing global investment banking services in Europe, especially in London?

To a great extent, greater concentration, higher margins and less liquid markets are the inevitable cost of imposing much higher prudential requirements. If much more capital is required to backstop risk-taking in such activities, then margins must rise until the capital employed in such activities earns the (risk-adjusted) equilibrium rate. This means that weaker competitors must depart, and concentration rises, until equilibrium is restored. It is arguable that the sooner such equilibrium is once again reached, the better. Perhaps it would be good, rather than bad, if one or two of the US big five also packed up and left?

4.3 European banking becoming parochial?

The third argument is that current developments are inducing European banks more and more to concentrate on their national roles and clients in their investment banking operations, rather than taking a wider European stance. Table 1 illustrates that Deutsche Bank and Barclays are the only Europeans left in the top seven for the EMEA market. But they are likely to lose their positions, because Deutsche Bank is currently undergoing a major reorganisation and Barclays is in the process of executing the Vickers split. In the investment banking field, the only pan-European banks will all soon be American. This has the corollary, for good or bad, that European national and EU-level authorities, such as the European Commission, will have rather less direct control over them. A key part of the European financial system is slipping out of the grasp of the European authorities.

It seems anomalous that, at a time when the European authorities are trying to establish a banking union and a capital markets union, the effect of their regulatory reforms has been to cause EU banks to concentrate their focus on their national roles, leaving the US banks as the only pan-European actors on this particular stage. But does it matter that the European authorities are left dependent on banks over which they have less ability to subject them to their demands?

There are concerns about US dominance in European investment banking. These are related to information advantages and soft relationships. The rise of Chinese investment banks to support the international expansion of Chinese corporates is a strong countervailing power to US and European investment banking dominance. The question arises whether US investment banks, as outsiders, are sufficient knowledgeable about European corporates. Moreover, what is the loyalty of these US banks to European corporates in times of distress? Next, there are concerns about corporate culture. Not long after successfully taming the global financial crisis, US financial firms resumed their practice of paying high salaries and bonuses. In contrast, Europe enacted caps on bonus payments. The large US investment banks are already trying to exempt their high-flyers in London from these EU rules, by arguing that these managers have a ‘global’ role and should therefore be remunerated by international rather than European standards11.

5. Policy response and conclusions

The European banking system is downsizing, partly because of on-going problems, partly because Europe is overbanked (Langfield and Pagano, 2016). That should run its course. The consequence is that the big US investment banks will be the sole leaders in the global investment banking market, as the Europeans, including the Swiss, are in retreat. We also find that the big five Americans are getting into pole position in the European investment banking market.

What should be the policy response? First, we look at the political side. With the decline of European banking (both in general and specifically investment banking), Europe’s hand in the EU-US Regulatory Dialogue is diminishing. Nevertheless, the European Commission is advised to strengthen its position in the EU-US bilateral negotiations and keep on viewing its banking industry as a strategic sector. The emerging role of the European Central Bank (ECB), on both the monetary and supervisory sides, can be used in these negotiations. Of the 30 global systemically important banks (so-called G-SIBS), eight are located in the US and eight in the EU banking union area. A further four G-SIBs and the European head offices of the US investment banks are based in the United Kingdom under the supervisory watch of the Bank of England. The European Commission, the ECB and the Bank of England should therefore jointly develop a strategic agenda with European priorities for their dealings with the US authorities. As in the US, this strategic agenda should be discussed with, and supported by, the industry. A strong and united front would enhance Europe’s position.

Second, we turn to the supervisory side. While Europe may lose some political clout, the supervisory implications are not a problem for Europe. With the move to capital markets union, the European supervisory architecture can handle the gatekeepers, which are becoming more US-dominated. The European Securities and Markets Authority (ESMA) has powers under the Regulation on Credit Rating Agencies (EC/1060/2009) to licence and supervise the European operations of the primarily US-based credit rating agencies. Similarly, the relevant directives (Second Banking Directive and Markets in Financial Instruments Directive) give the relevant European supervisors (in this case the Prudential Regulatory Authority and the Financial Conduct Authority) powers over the London-based European operations of the US investment banks.

Third, the large corporates could themselves take precautions. For the bigger financing operations, a corporate typically hires a banking syndicate, which is a group of investment banks that jointly underwrite and distribute a new security offering, or jointly lend money to the corporate. European corporates would be well advised to include at least one (large) European investment bank in this syndicate, also in good times when they do not need them. That could help them in bad times, when US banks might be reluctant for whatever reason (including more detached decision-making). The involvement of a (local) European investment bank in the syndicate is not only useful for loyalty but also information reasons. Because of their local roots, the European banks have an information advantage over their US peers, which keep offices in New York and London. The practice of giving a European investment bank at least one place in further US-dominated banking syndicates could help to avoid complete dependence on the whims of the big US investment banks.

Finally, as the underlying financial architecture for banking union and capital markets union is still under construction, we do not expect big changes in the European financial landscape in the short term. If, however, further steps are taken to complete banking union as suggested in the Five Presidents Report (2015), including European deposit insurance with a fiscal backstop by the European Stability Mechanism, a truly European banking system might emerge with strong regional, and potentially global, players. But that is only speculation.

About the authors

Related content

A brown or a green European Central Bank?

The European Central Bank portfolio is skewed towards the brown economy, reflecting a bias in the market.

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition

A new integrated-value assessment method for corporate investment

To contribute more to the green transition, companies should start to make investment decisions based on integrated-value assessment.

Halftime for the European Union’s recovery fund: is the glass half full or half empty?

How has the RRF performed at its halfway point in terms of implementation, results orientation and additionality for future EU funding instruments?