The benefits and drawbacks of TTIP

What’s at stake: Since the recent leak of documents on TTIP (Transatlantic Trade and Investment Partnership) negotiations, there has been renewed inte

The Biannual Eurobarometer survey indicates that support for TTIP in the EU fell from 56 percent in May 2015 to 53 percent in November 2015, while opposition grew from 28 percent to 32 percent for the same period. The countries most strongly against TTIP are Germany, with 59 percent up from 51 percent in May 2015, and Austria, with 70 percent up from 67 percent. Support has also fallen by 10 points in the Netherlands, matched by drops in selected Central and Eastern European member states, including a 9 point fall in Bulgaria and 13 point decrease in the Czech Republic.

TTIP and its impact on economic growth and labour markets

Economic research company Ecorys recently published a 400-page study for the European Commission, detailing the macroeconomic impact of TTIP on national income, GDP, wages, aggregate and bilateral trade flows in the EU and the US. The study updates the CEPR (2013) study, and employs a computable general equilibrium (CGE) model. It adds recent growth forecasts, but extends the time under consideration from 2027 to 2030. National income is expected to be 0.3 percent higher each year, and GDP 0.5 percent higher for the EU and 0.4 percent for US. Wages for both low and high-skilled workers go up by 0.5 percent in the EU, and bilateral trade is expected to increase by 27 percent on EU exports to US and 35.7 percent on US exports to the EU. They predict that consumer prices will increase by 0.2 percent in the EU on average, and decrease by 0.1 percent in the US. In the meantime, the price of imported products and services from the US will be 4.1 percent cheaper, particularly in the agricultural sector through tariff reductions. The conclusions of this study are similar to one by CEPS (2014).

Concepción la Torre et al. construct four different scenarios for Spain, depending on the depth of implementation and the time horizon. For example, for a 5-year horizon and ‘ambitious’ setup, with no tariffs and a 25 percent reduction of non-tariff barriers, they argue that TTIP would lead to an extra 0.74% of annual GDP growth. For the conservative scenario, with no tariffs and only a 10 percent reduction on non-tariff barriers, they estimate extra annual GDP growth of 0.3%. Their results suggest that mining, and some manufacturing production, could benefit the most, while other sectors, mainly transport, could experience a decline. Furthermore, they estimate that TTIP will create around 65,000 jobs over five years.

Felbermayr and Aichele from the IFO institute calculate the impact of the US-EU trade deal on Germany. Encompassing almost half of world GDP, it will have strong economic effects on Germany. The authors argue that, despite appearances, US-German trade has the potential to increase. Surveying existing studies, they find that the deal could increase per capita income in Germany by between 1 and 3%.

Rodrik discusses the models employed in the pro- and anti-TTIP groups, the most important ones being the CEPR study and the paper by Capaldo. The CEPR study uses a standard CGE model that assumes full employment and perfect competition and finds that by 2027 the GDP of EU and US will rise by 0.5% and 0.4% respectively. These results, however, have been challenged in a paper by Capaldo, who uses a Keynesian model where output is demand-determined and finds that EU GDP would fall as a result of a decline in net exports. In his view, the CEPR study would be his baseline for the economic effects of TTIP a decade down the line, but large margins of error would make it unfit for policy purposes. The Capaldo model, by contrast, seems to be an inappropriate perspective for anything other than the short run.

TTIP and investor-to-state dispute settlements

Rodrik goes on to state that the real issues lie elsewhere – in the broader social and political consequences of regulatory harmonisation and the appropriateness of an ISDS (investor-to-state dispute settlement[1]) regime in the North Atlantic region. According to The Economist, ISDS is at the centre of activists’ opposition to TTIP. ISDS is not an uncommon practice, it is featured in most of the 3000 bilateral trade and investment deals. The commission in the past suspended talks with the US on investor protection. With TTIP negotiations the investor dispute settlement has come to the fore again.

Felbermayr and Aichele critically question the need for investor-state dispute settlement. Referring to the history of German trade deals, Germany was the first country in history to sign a Bilateral Investment Treaty (BIT). These type of treaties often contain such ISDS clauses. Typically, the partners to the agreement are poorer, less developed countries, which are recipients of German foreign direct investment. In the case of TTIP, Germany itself is a recipient of FDI – this has negatively affected the public perception of BITs.

TTIP and its impact on social conditions, corporate taxation and innovation

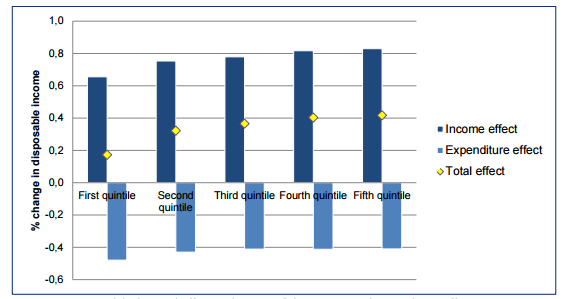

The Ecorys study also looks at the social impacts of TTIP on income and expenditure in the EU. The results indicate a wage increase of 0.4 percent for both low and high skilled workers. However, the effect is uneven across different groups on the income distribution, with the top incomes increasing more than low incomes. Similarly, on the expenditure side, higher consumer prices will have bigger impact on low earners, due to the fact that food and utilities make up a larger share of the expenditure basket for the bottom quantiles. Overall, this uneven effect on income distribution is expected to produce an increase, albeit marginal, of 0.1 percent in the Gini coefficient.

Source: Ecorys

Piketty states that TTIP could be an opportunity for both sides — if it stretches beyond the free trade aspect. It must also be a treaty about fiscal cooperation and a basis for a common corporate tax. Very often, multinationals on both sides of the Atlantic pay less tax than small or medium-sized businesses, which is unacceptable. A binding treaty between the US and the EU is the right place to address and solve problems like tax havens and unregulated capital flows. Such a treaty would represent half of the world’s GDP. If this powerful bloc of the global economy doesn’t manage to find a solution and speak with one voice, then progress seems very unlikely.

Dreher and Schwäbe ask if TTIP actually promotes innovation, which is one of the main drivers behind economic growth. They focus on the opportunities for participating economies to become more innovative. The article concludes that, according to currently published documents, the legal properties of TTIP could harm the ability of states to adapt their regulatory standards – the main instrument for a dynamic and technology-specific innovation policy. A lack of flexibility for the new supranational standards could be a major reason for difficulties. They question the capacity of the standards which aim at “creative disturbance” of market processes by the state in order to stimulate innovative activities and to induce additional growth.

Impact of TTIP on third parties

Akman, Evenett and Low analyse the impact of TTIP on third parties, and conclude that it is highly unlikely that TTIP will trigger other major trade deals. On the positive side, if trade compliance is harmonised between the two largest economies, access to a single regime might prove beneficial for the third parties. Moreover, if efficiency gains are made and costs reduced, the growth dividend might benefit third countries through a spill-over effect. Negative outcomes might result from trade and regulatory diversion and restrictions, which ultimately lead to limited market access, particularly for developing countries. However, TTIP also presents an opportunity for the third countries to undertake domestic reforms, such as increasing market access, reducing administrative trade costs and other regulatory reforms to make their economies fit for outside competition.

The Ifo Institute investigates the potential impact of TTIP on developing and emerging countries and find that the effect on both winners and losers is likely to be small. Microeconomic analysis shows that the cumulative losses from over 10-12 years amount to less than 1 percent of per capita income. The report stresses that against a background of 3-4 percent annual growth rates in the developing countries, this is a small loss. Furthermore, those involved in the value creation chains of US and EU exports, including raw material exporters, are expected to be positively affected. Conversely, those that compete with the US and the EU in textile manufacturing and some food sectors, stand to be negatively affected.

Beyond TTIP and TPP

De Arcangelis looks at European trade beyond TTIP and observes that the world balance of trade is being shifted towards the US. Combining TPP (Trans-Pacific Partnership) and a potentially successful conclusion of TTIP, the US would be at the centre of world trade (excluding the world's biggest exporter, China). To break the deadlock, and to safeguard a joint trade policy, it is paramount to think about measures of compensation for the segments of the population hit most by globalisation. If the EU had such national or communitarian instruments, it could more easily reposition itself on the stage of global trade, and take a more active role towards the most dynamic economies. In sum, thinking big after TTIP means combining new trade policies with compensatory policies.

Paul Krugman considers himself a lukewarm supporter of free trade, however his take on both TTIP and TPP is that there is much less than meets the eye. What the world needs at the moment is not more trade liberalisation, but more demand and solutions to escape the threat of deflation. On the demand side, perhaps trade liberalisation might increase world exports. However, liberalisation will also increase world imports by the same amount. As a consequence, the composition of world expenditure will change, with each country spending more on foreign goods and less on its own, which does not necessarily raise total spending. On the supply side, trade liberalisation tends to raise efficiency and productivity, but only when starting from high levels of protectionism. Considering the already low trade tariffs, cutting it further will not boost global trade significantly.

The Economist, in a bold move, urges Krugman to do more homework on TPP. First, even though tariffs are low, they have not come down universally. Cutting tariffs for instance on wind-power installations and solar energy facilities might be macroeconomically insignificant, but it could still be microeconomically desirable. Another key issue on TTIP and TPP’s agenda is updating the rules on services trade, considering an expanding array of cross-border tradable services, such as insurance, finance and consulting. In sum, the impact of TTIP and TPP could be a good thing for investors, consumer and producers if the participating governments honour each other’s’ approval of the set of standards.

[1] Via an investor-state dispute settlement (ISDS) mechanism, foreign investors can sue the state (i.e., the EU or the US) that is separate from the normal public judicial system, in case of a breach in the agreement.

About the authors

Related content

Reconciling contradictory forces: financial inclusion of refugees and know-your-customer regulations

The authors contributed to the new issue of the 'Journal of Banking Regulation' with a paper on financial inclusion initiatives and banking regulation

People on the move: migration and mobility in the European Union

Migration is one of the most divisive policy topics in today’s Europe. In this publication, the authors assess the immigration challenge that the EU f

Emerging countries have replaced most of Russia’s lost trade with advanced economies

Russian trade overall seems to have suffered little from sanctions; meanwhile, medicine and food trade continues with sanctioning countries

Global supply chains: lessons from a decade of disruption

This paper revisits the effects of three shocks on the functioning of global supply chains.