The effectiveness of the European Central Bank’s Asset Purchase Programme

Since the end of 2014, inflation has been at or very close to zero. With very little ability to move the actual interest rate further into negative te

The general macroeconomic situation and weak inflation dynamics justified quantitative easing (QE) in the euro area. Doubts have emerged about its effectiveness as inflation has remained weak.

However, we do not know where inflation would have been without QE and the still large slack in the economy suggests that inflation might increase only in a few years.

Two major channels through which QE operates are visible: a weaker exchange rate and lower long-term yields. Lending, investment and housing have somewhat increased. However, banks have not shed sovereign debt from their balance sheets at a significant scale.

Bank profitability is squeezed by QE but we do not see a generalised financial stability risk as credit creation remains meager. Further monetary policy action is unlikely to generate strong benefits. It is important that other government action supports the ECB in achieving its goals.

Executive summary

For full references and footnotes, please see the PDF version of this publication.

- Central banks resort to quantitative easing when the normal monetary policy tool of lowering the short-term interest rate is constrained. This constraint typically arises from the zero-lower bound, ie the reluctance to cut nominal rates below zero. This can result in a real interest rate that, while negative, is still too high for an economy to quickly find its way back to full employment and equilibrium. Many indicators such as the low inflation rate, high unemployment rates, the current account surplus and high savings compared to weak investment suggest that the euro area is in such a situation.

- Quantitative easing attempts to address this situation through three different channels: lowering long-term interest rates to improve investment conditions and disincentivise savings (interest rate channel); purchasing relatively safe long-term assets thereby driving investors into riskier investments (portfolio rebalancing channel); and weakening the exchange rate (exchange rate channel).

- The main criticisms of the European Central Bank’s sovereign QE programme are that it is (i) unlawful in a monetary union without a joint treasury; (ii) ineffective and/or unnecessary; and (iii) associated with negative side effects in terms of financial stability and inequality. The design of the programme has dealt with the first criticism. This briefing focuses on the second criticism.

- We argue that the ECB’s QE programme is necessary given the general macroeconomic situation and the continuing weak inflation dynamics in the euro area. But the continuously weak inflation dynamics have raised doubts about its effectiveness.

- Assessing the effectiveness of QE is difficult without a counter-factual, but we show that QE had a strong effect on the exchange rate channel, weakening the euro-dollar exchange rate substantially. We also show that long-term interest rates fell substantially in anticipation of the programme. In relation to portfolio rebalancing, we show that banks have not shed sovereign debt from their balance sheets at a significant scale so the purchases have been from different parties. We show that investment has picked up slightly, housing markets in some countries have gained strength but credit creation is only slightly increasing. Finally, we show that the expansion of the ECB’s Public Sector Purchase Programme in March 2016 has had no visible effect on any variable.

- We document that QE has reduced the profitability of banks by narrowing their margins. The recent corporate QE, while lowering corporate yields, is further reducing margins for banks.

- We argue that further monetary policy measures are unlikely to bring strong benefits. One sensible avenue for monetary policy could be to enact the sovereign bond purchases from banks in order to reduce the exposure of banks to sovereign debt. More important, however, is government action. In particular, reducing the debt overhang, tackling banking fragilities and introducing reforms to create new business opportunities and fiscal measures in countries with fiscal space would help speed the recovery and increase inflation.

1 Introduction

The decision to start quantitative easing in the euro area has been highly controversial. After a long period of deliberation, the European Central Bank decided in January 2015 on a sovereign QE programme that was implemented from March 2015 with monthly purchases of €44 billion. The amount purchased was increased in March 2016.

The controversy over QE now is less about whether the ECB is empowered to use a monetary policy instrument that most central banks in advanced economies have used. It is rather about whether QE is effective as a tool to increase inflation to the target. In addition, there is increasing concern that QE and other non-conventional monetary policy measures produce unintended consequences in terms of financial instability or in terms of wealth inequality.

Central banks resort to QE when the nominal short-term interest rate falls to zero. The so-called zero lower bound prevents central banks from reducing the nominal interest rate below zero. Central banks cannot lower the rate much below zero because households and corporations would shift their savings to cash, which would generate a return above the rate set by the central bank.

When the short-term nominal interest rate reaches zero, the real interest rate of the economy is set by the inflation rate. If inflation is low, this real rate may be well above the level at which the economy returns to equilibrium, unemployment is significantly reduced and output reaches its potential. A low inflation environment with the nominal rate at zero therefore risks creating an economy with high and sustained unemployment.

Quantitative easing attempts to address this problem by lowering the nominal long-term interest rate and by pushing investors into riskier asset classes. The lower long-term interest rate should encourage savers to save less and shift towards consumption, and investors to take advantage of the lower long-term funding cost to fund investment (which is in term more profitable). Moreover, by purchasing sovereign bonds, the central bank forces investors to buy other, riskier assets, which in turn should stimulate activity. The increased liquidity should weaken the exchange rate thereby supporting the recovery. Finally, more targeted QE can remove weak assets from balance sheets, contributing to deleveraging (Woodford, 2012).

But the effectiveness of monetary policy depends on economic circumstances. While arguably inflation is a monetary phenomenon in the long run, the effectiveness of monetary measures in the short to medium run depends on broader macroeconomic circumstances.

The euro area suffered from a number of shocks and a weak starting position that led to particularly strong disinflationary pressures. In principle, the process of disinflation – itself the result of poor aggregate demand conditions – that the euro area is experiencing is the result of the following factors:

- Deleveraging: most countries have at least one sector in their economy that built up levels of excessive debt prior to 2008. Reducing the debt overhang weakens demand and as a consequence there is downward pressure on prices. Debt deleveraging in the euro area has been undertaken comparatively slowly (Ahearne and Wolff, 2012; Ruscher and Wolff, 2012).

- A fragile banking system is a further factor hampering the effective transmission of monetary policy to the euro area. Mody and Wolff (2015) show the significant weaknesses of the euro area’s banks and in particular the still high non-performing exposures. The currently ongoing resolution of banking problems in Italy illustrates the slow clean-up of the banks. Schoenmaker and Véron (2016) argue that the new European banking supervisor is tough and addresses the weaknesses, but that problems have not yet been fully resolved.

- Risks and uncertainty: a variety of economic, regulatory and geopolitical risks have emerged across the euro area and beyond. Banks are reluctant to invest in new activities, and corporates and households are reining in consumption and investment. The risk of the break-up of the euro area had one of the biggest negative effects on confidence and investment.

- Negative feedback between low growth/inflation and debt: The process of deleveraging becomes increasingly difficult as it progresses. The decline in output and prices that deleveraging causes reduces the scope for further deleveraging. It is exactly for this reason that those countries with the greatest deleveraging needs find it the hardest to reduce their debts.

- Finally, fiscal and structural policies play a central role in supporting growth and thereby helping the ECB to achieve its inflation target. In the euro area, fiscal policies have often dampened demand or have turned slightly expansionary only this year. In turn, progress with structural reforms that could provide incentives for new investment has been slow in the euro area’s biggest three economies. Arguably, monetary policy has been insufficiently supported by other policies (Fratzscher et al, 2016).

The euro area was in need of a quantitative easing programme. Growth was low, inflation dynamics were weak with repeated downward revisions, savings were high and investment was meagre, falling well below pre-crisis investment trends. Overall, the signs of demand weakness were overwhelming pointing to a need for more stimulating monetary policies. But how effective has the ECB’s QE programme been in stimulating demand and increasing inflation? Would increasing QE support the euro area or is the marginal benefit of QE limited? Has QE introduced new risks to the economy? We tackle these questions by reviewing the decisions behind QE, by discussing the macroeconomic implications of QE, and the channels through which it is transmitted, and by assessing the potential risks arising from aggressive monetary policy.

2 The ECB’s unconventional monetary policy: what is it and what does it do?

On 22 January 2015 the European Central Bank (ECB) announced the Public Sector Purchase Programme (PSPP), an expansion of the Asset Purchase Programme (APP). Under the PSPP, the Eurosystem started in March 2015 to purchase sovereign bonds from euro-area governments and debt securities from European institutions and national agencies. This new programme supplemented two other asset-purchase programmes already in place within the APP: the Asset-Backed Securities Purchase Programme (ABSPP, which started in November 2014) and the third Covered Bond Purchase Programme (CBPP3, which started in October 2014).

On 3 December 2015, ECB president Mario Draghi announced an extension of the PSPP. While it was initially planned to last until at least September 2016, it was extended until at least March 2017. President Draghi said that the asset purchase programme would continue “until we see a sustained convergence towards our objective of a rate of inflation which is below but close to 2 percent”. Additionally, regional and local government bonds were added to the list of eligible assets for purchase.

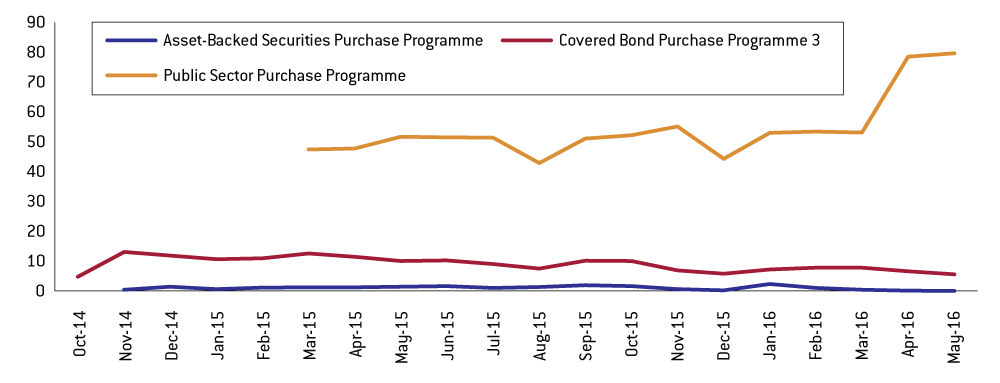

Finally, on 10 March 2016 the ECB announced a further expansion of the APP: the combined monthly amount purchased was increased from €60 billion to €80 billion, and the new Corporate Sector Purchase Programme (CSPP), which involves the purchase of investment-grade euro-denominated bonds issued by non-bank corporations established in the euro area, was added. Details of the amount of corporate bonds to be purchased every month were not given, but the ECB indicated that the CSPP would not lead to a higher amount of monthly purchases under the APP as a whole, thereby indicating that corporate bond purchases will be made at the expense of one or more of the three other programmes already in place. Figure 1 plots the monthly volumes of assets purchased so far under the three existing programmes: the ECB has purchased about €1 billion per month under the ABSPP, almost €10 billion under CBPP3, and €50 billion under the PSPP (before this was raised to about €79 billion in April 2016).

Figure 1: Monthly purchases under the three APP purchase programmes of the ECB (€ billions)

Source: European Central Bank.

Interestingly, Hüttl and Merler (2016) have shown that the increase in the Eurosystem’s holdings of euro-area government bonds has not been matched by a corresponding reduction in the amounts of these bonds on euro-area banks’ balance sheets. This is corroborated by ECB data on bank balance sheets, which shows that bank government bond holdings have gone down by €82 billion since the start of the PSPP, compared to the €726 billion currently being held by the Eurosystem (see Figure 2). This suggests that government bonds purchased under the PSPP have mostly been purchased from non-bank entities and foreign banks.

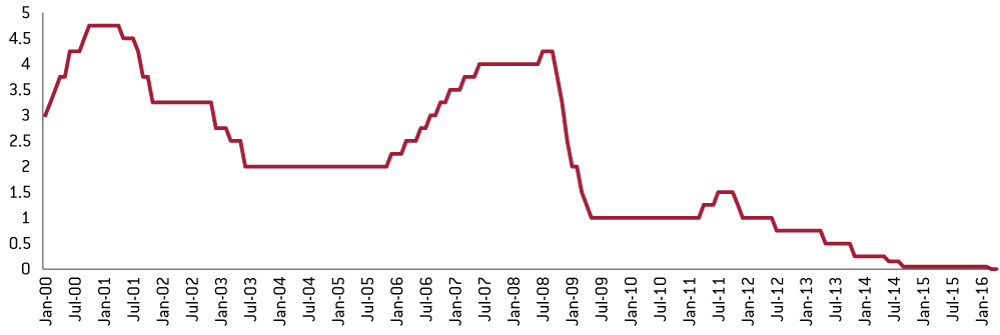

Figure 3 shows that the ECB’s main refinancing operations rate was gradually lowered in response to the Great Recession, until it reached zero in March 2016.

Figure 2: Government bond holdings of euro-area monetary and financial institutions (€ billions)

Source: European Central Bank. Notes: 1) “Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP; 4) CSPP and expansion of PSPP. * “Whatever it takes” refers to the speech given by ECB President Draghi in July 2012, in which he vowed to do whatever it takes to safeguard the financial stability of the euro area. See https://www.ecb.europa.eu/press/key/date/2012/html/sp120726.en.html.

Figure 3: The European Central Bank main refinancing operations rate (%)

Source: European Central Bank.

However, QE can become less effective as the purchase programme continues. It can also increase inequality (Claeys, Darvas and Leandro, 2015) and undermine financial stability (Claeys and Darvas, 2015), especially as the policy continues to be implemented over a longer period. Additionally, the untested nature of such unconventional monetary policies makes it much harder to calibrate them in order to obtain the desired increase in aggregate demand, especially if they go on for a long period.

3 The effects of quantitative easing

Analysing the effects of QE is a difficult task. Its effectiveness can only be assessed against a benchmark that is unknown, the so-called counterfactual. What would have the developments in inflation, employment and GDP been if the ECB had not embarked on QE? In this section, we show simple charts documenting developments in key macroeconomic and financial variables around the dates of major decisions by the ECB on both QE and the Outright Monetary Transactions (OMT) programme.

3.1 Inflation and inflation expectations

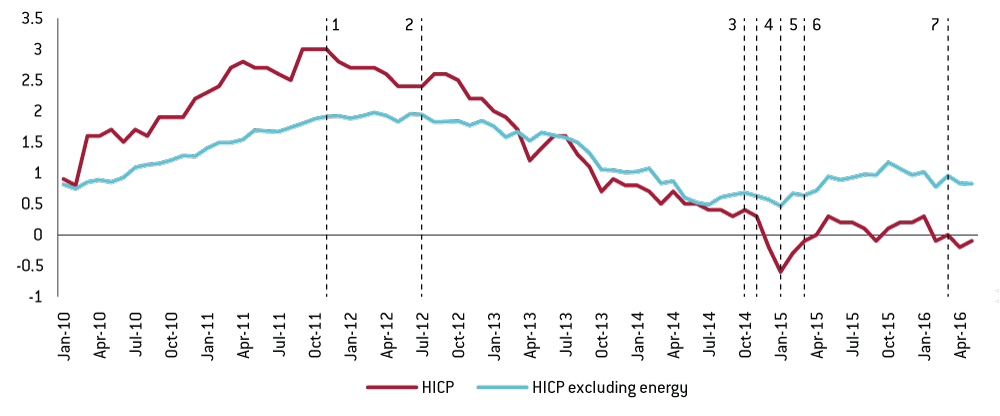

January 2015, the month of the announcement of the PSPP, was the month with the lowest rate of inflation in the euro area ever, -0.6 percent (Figure 4). Thereafter, year-on-year inflation reached a peak of 0.3 percent in May 2015, the third month of government bond purchases. Since then, monthly inflation has drifted between -0.1 percent and 0.3 percent, falling to -0.2 percent in April 2016, and -0.1 percent in May. This is still far from the ECB’s target of close to but below 2 percent, and data for recent months points to a deteriorating trend. Core inflation is currently higher than overall inflation because energy prices are falling, but it is still below 1 percent, though the start of the PSPP does seem to have had a short-lived positive effect.

Figure 4: Euro area overall HICP annual growth rate (%)

Source: European Central Bank. Notes: 1) CBPP2; 2) “Whatever it takes’’*; 3) CBPP3; 4) ABSPP; 5) PSPP announcement; 6) Start of PSPP; 7) CSPP and expansion of PSPP. * See notes to Figure 2. HICP = Harmonised index of consumer prices.

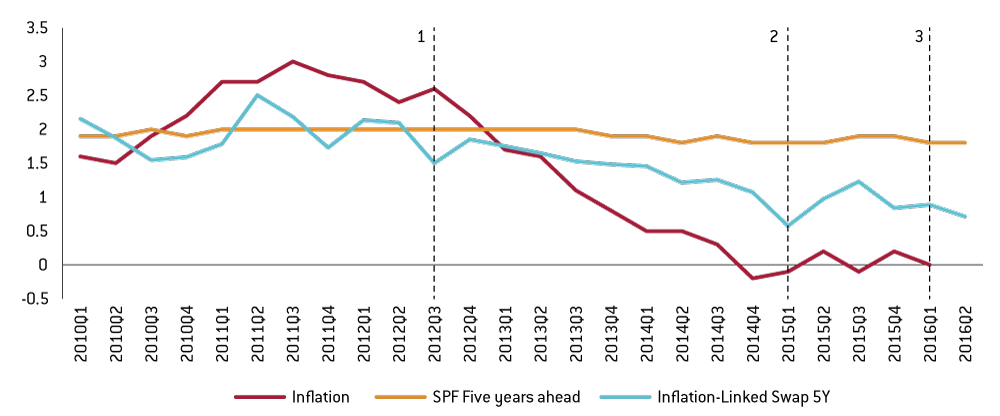

Figure 5: Inflation expectations: Survey of Professional Forecasters and 5-year inflation-linked swap rates

Source: European Central Bank and Thomson Reuters Datastream. Notes: 1) “Whatever it takes’’*; 2) Announcement and start of PSPP; 3) CSPP and expansion of PSPP. * See note to Figure 2.

In terms of perceptions, the information that expectations convey is mixed. Figure 5 shows long-term expectations (at the 5-year horizon) from two different sources: a survey of professional forecasters and market expectations (swap rates). The survey figures show that expectations have been and remain both very stable as well as at the level of the ECB’s inflation objective, below but close to 2 percent. This indicates that professional forecasters believe that given enough time, inflation will return to the definition of price stability. However, market expectations, at the same horizon, show something different. The 5-year inflation-linked swap rate shows a clear declining trend (Figure 5). We interpret this difference to mean two things: first, as these two series diverge, this signals that confidence is starting to wane. Second, the existence of this persistent wedge, visible also recently in the US, might be a reflection of increased uncertainty. Market expectations are quicker to follow actual inflation (even at longer horizons) because they attempt to also capture perceptions about risk and therefore hedge against them. Survey expectations on the other hand, reflect an opinion about inflation reaching its target in the relevant horizon and are therefore arguably more a measure of policymakers’ ability to deliver.

A formal measure of credibility1 shows that both the Federal Reserve and the ECB have been able to remain credible during the financial crisis that started in 2008. However, while the Fed has only seen a temporary decrease in credibility that was recovered almost in full subsequently, the ECB has not been able to regain the credibility it has lost. Arguably since inflation in the two areas has been very similar in the last eight years, the difference in the way the credibility of the Fed and ECB has changed is arguably the result of the different macroeconomic policy mixes applied. Therefore, also factors largely outside the control of the ECB have affected its credibility.

3.2 The real effects of QE: GDP, investment and unemployment

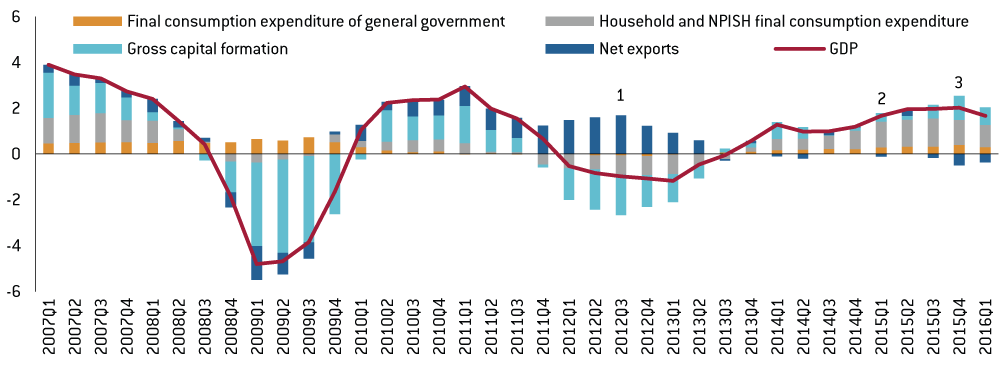

Euro-area real GDP fell for seven consecutive quarters starting in 2012: the second dip of the euro area’s double-dip recession (Figure 6). Since then, GDP has grown moderately, reaching a peak of around 2 percent following the start of the ECB’s PSPP. The latest data shows a drop in GDP growth to 1.7 percent during 2016 Q1. Household consumption, investment and to a lesser extent fiscal expenditure have been the main drivers of growth in the last quarters.

Figure 6: Contributions to real GDP growth (growth contribution, percentage points)

Source: Eurostat. Notes: 1) “Whatever it takes’’*; 2) Announcement and start of PSPP; 3) CSPP and expansion of PSPP. * See notes to Figure 2. NPISH = Non-profit institutions serving households.

Figure 7: Euro-area gross fixed capital formation (real year-on-year growth, %)

Source: Eurostat. Notes: 1) ‘’Whatever it takes’’*; 2) Announcement and start of PSPP. * See notes to Figure 2.

For the recovery to be stronger, a bigger increase in investment would be desirable. Gross capital formation has picked up slightly after a period of continuous decline throughout 2012 and 2013 (Figure 7). Annual investment growth has been positive since 2014 Q1, reaching a peak of 3.9 percent in 2015 Q4, the penultimate quarter of available data. It is unclear whether the start of the PSPP had any impact.

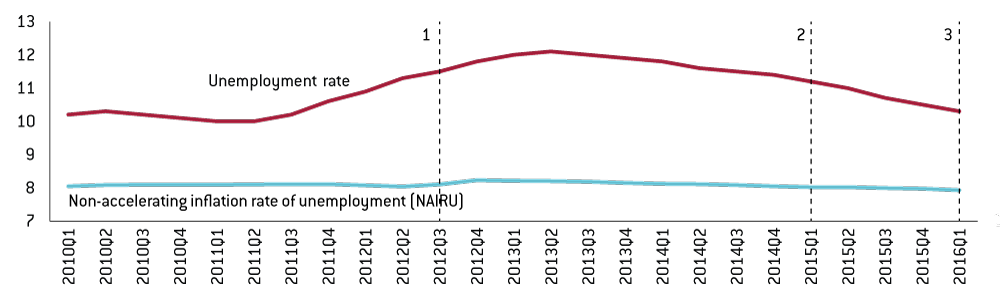

Figure 8: Euro-area unemployment (%)

Source: Eurostat and Oxford Economics. Notes: 1) “Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP. * See notes to Figure 2.

One possible explanation of why expansionary monetary policy has had little visible effect on inflation is the significant slack in the economy. Euro-area unemployment has steadily but slowly decreased from its peak of 12.1 percent in the second quarter of 2013, reaching 10.3 percent in Q1 2016 (Figure 8). Following the announcement and start of the PSPP, the unemployment rate continued its gradual decrease but there does not seem to have been a significant effect from QE on the pace of unemployment reduction. The unemployment rate is still very high compared to the non-accelerating inflation rate of unemployment (NAIRU), the theoretical level of unemployment below which inflation would start accelerating.

4 The channels

4.1 Bond yields

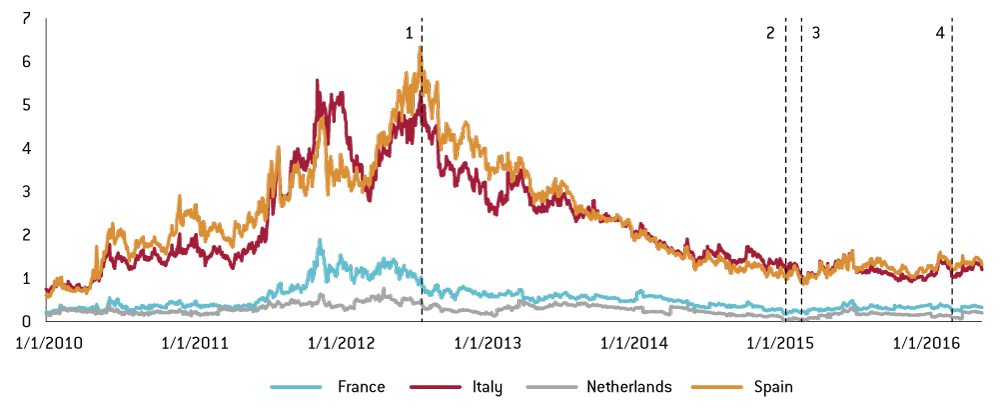

Euro-area government bond yields shot up during the sovereign debt crisis of 2011, especially in the periphery countries (in Spain and Italy, 10-year bond yields reached 7.6 percent and 6.5 percent respectively; Figure 9). The highest values were attained in summer 2012, until President Draghi’s famous “whatever it takes” speech (see note to Figure 2). Since then bond yields have steadily reduced except for a temporary increase in the summer of 2015 during the Greek crisis. In fact, this increase in bond yields coincided with the first few months of the PSPP’s operation. There has since been a gradual reduction in yields.

While bond yields declined both in the core and periphery countries, periphery bond yields fell faster after Draghi’s July 2012 “whatever it takes” speech, thus compressing the spreads against German bonds (Figure 10). However, the announcement and start of the PSPP did not seem to have a very strong effect on these spreads.

Figure 9: 10-year government bond yields (%)

Source: Thomson Reuters. Notes: 1) “Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP; 4) CSPP and expansion of PSPP. * See notes to Figure 2.

Figure 10: Ten-year government bond spreads against Germany (%)

Source: Thomson Reuters. Notes: 1) ‘’Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP; 4) CSPP and expansion of PSPP. * See notes to Figure 2.

4.2 Lending

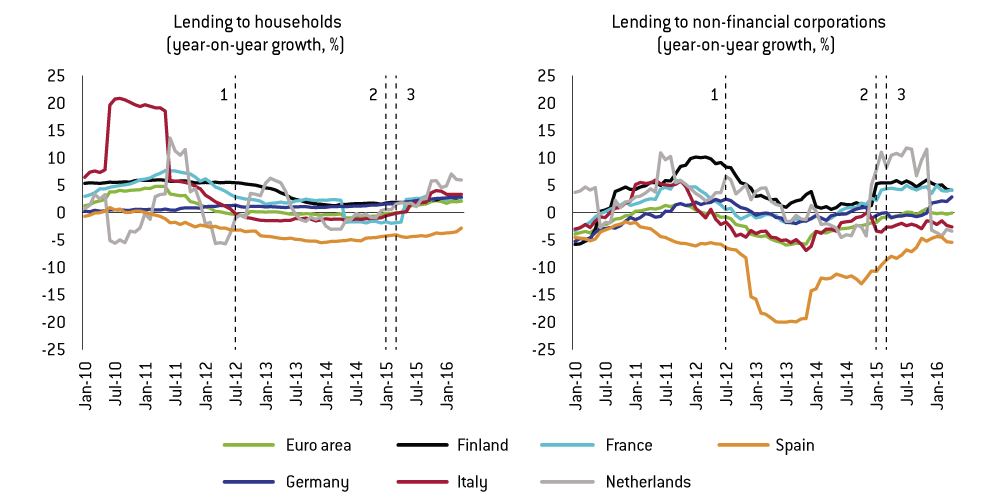

We observed earlier that consumption and investment are picking up and are the two main contributors to GDP growth. The link to monetary policy comes through credit creation. Figure 11 shows that lending to non-financial corporations fell steadily since 2012, before it stabilised in the second half of 2015 following the start of the PSPP. Lending to households has held up more robustly, increasing since the announcement of the PSPP from stagnation to a yearly growth rate of about 2 percent. This credit was mostly in the form of mortgages, which was helped by the stabilisation of, or even the increase in, house prices. Credit, therefore, has been important in reversing and sustaining the contributions of consumption and investment to growth.

Figure 11: Loans to households and non-financial corporations (year-on-year growth, %)

Source: European Central Bank. Notes: 1) “Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP. * See notes to Figure 2.

4.3 Exchange rate

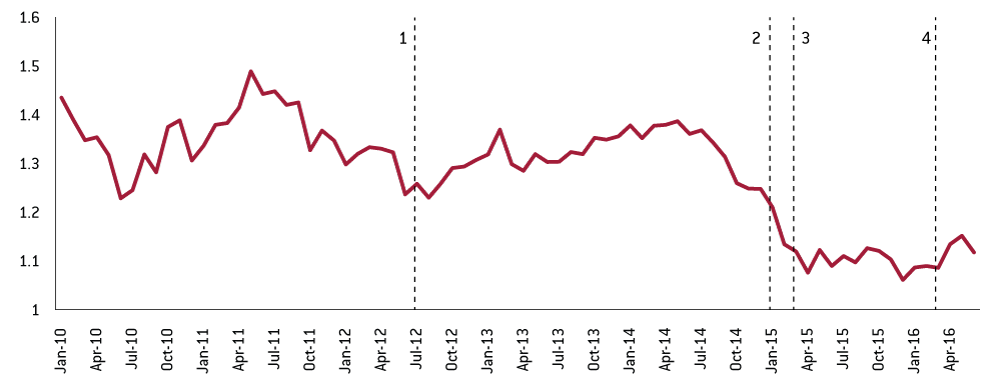

QE has likely had a significant effect on the exchange rate. The USD/EUR exchange rate is now significantly weaker (Figure 12). Compared to the peak in 2014, the exchange rate is now down from almost 1.4 to 1.12. Most of the decline happened prior to the official announcement of the PSPP, but in line with discussions about when and how the ECB would start the PSPP. One factor that has significantly affected the exchange rate during the last year is monetary policy normalisation in the United States. The divergence in monetary policy across the Atlantic leads to capital flows which put downwards pressure on the euro area’s effective exchange rate. A weaker exchange rate facilitates exports and contributes to GDP by making domestic goods relatively cheaper than foreign goods.

Figure 12: USD/EUR exchange rate

Source: Thomson Reuters Datastream. Notes: 1) “Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP; 4) CSPP and expansion of PSPP. * See notes to Figure 2.

4.4 Portfolio rebalancing

Portfolio rebalancing is perhaps the hardest QE transmission channel to document. In principle, one would want to observe that sellers of government bonds to the ECB are then obliged to allocate cash to riskier assets. In the euro area, it is important to note that the ECB’s purchases of government bonds from the balance sheets of banks have been limited (Figure 12 and Table 1). Table 1 shows that only Spanish banks have sold government bonds significantly. This is much less the case for France, Italy and Germany, where other residents or even non-residents have sold government bonds.

This suggests that portfolio rebalancing should come primarily from non-banks. Unfortunately, we do not have good data readily available on these non-banks.

5 The risks of current monetary policy

Monetary policy, in its conventional form, affects bank balance sheets through two channels. First, are low interest rates leading banks to search for yield? This implies that they might take bigger risks by lending to riskier projects. Arguably, this is unlikely to happen while the levels of private debts remain high. The demand for new credit is unlikely to pick up before the levels of private debt reduce to lower and more sustainable levels. At the same time, banks are still in the process of repairing their balance sheets and are seeking to conform to new regulatory requirements.

The second channel is banks’ profits. Banks want to pass falling interest rates through to deposit rates. This means that their cost of funding reduces, which, all things being equal, increases their profits. As banks see their profits increase they are less likely to invest in risky projects because they have more to lose. However, the situation is different when deposit rates are close to zero. In reality banks are very reluctant to reduce these rates to negative numbers, effectively charging depositors, because that would encourage them to withdraw their money. As interest rates reduce, banks instead see a squeeze on their profits, which further restricts bank business. In turn this undermines the creation of new credit and the funding of new investments.

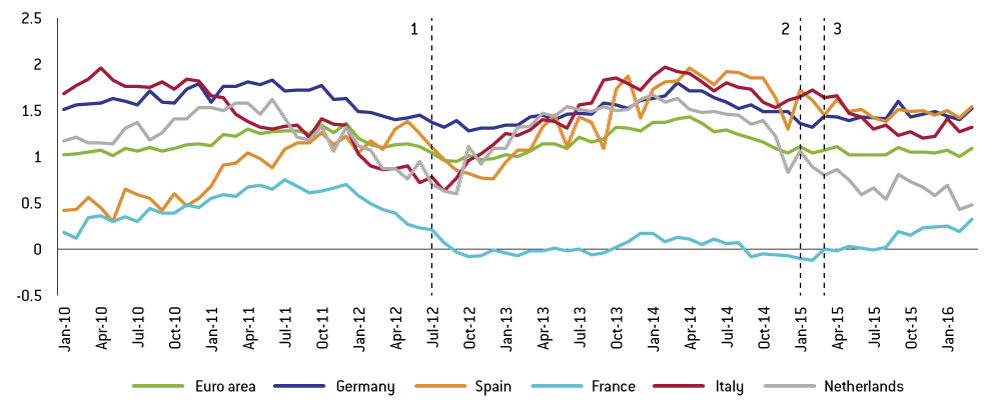

Unconventional monetary policy, in the form of QE, aims directly at reducing the long-term yield of assets. The term spread, or the spread between long- and short-term bond yields for a given country, should thus have declined following the start of the PSPP. As Figure 13 shows, the term spread fell from very high levels in the periphery countries during 2013 and 2014, but increased after the announcement and start of QE. The explanation might be the uncertainty over negotiations with Greece in summer 2015. As this subsided, the term spread also fell. The term spread appears to have increased a little since the ECB announcement of the expansion of the PSPP in March 2016, under which monthly purchases were increased and corporate bonds were included.

Figure 13: Government bond term spreads(10 year yields – 1 year yields) (%)

Source: Thomson Reuters. Note: 1) “Whatever it takes”*; 2) PSPP announcement; 3) Start of PSPP; 4) CSPP and expansion of PSPP. * See notes to Figure 2.

Figure 14: Changes in the term spread and the lending-deposit spread between January 2014 and April 2016 (%)

Source: Papadia and Wolff (2016) (updated), European Central Bank and Thomson Reuters Datastream.

Figure 15: Lending-deposit rate spread (%)

Source: European Central Bank.

Note: 1) “Whatever it takes’’ 2) PSPP Announcement 3) Start of PSPP. See notes to Figure 2.

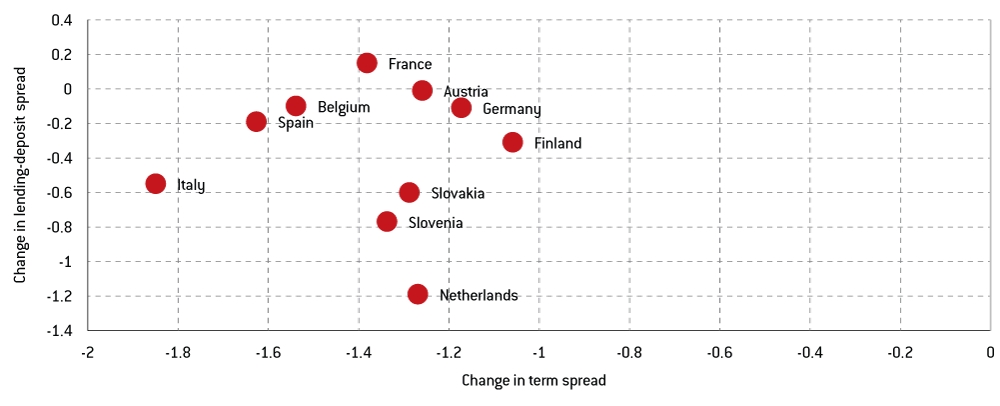

Overall, a fall in the term premium affects banks’ profitability to the extent that banks transform short-term deposits into long-term loans. Figure 14 shows the positive correlation between term spreads and bank lending spreads, suggesting that QE does influence profitability.

Furthermore, Figure 15 shows that the spread between lending and deposit rates in the euro area as a whole has been reducing since the beginning of 2014. While these developments reflect lower lending rates which are helpful in an economy with little lending, they also indicate declining bank profitability. This can be a problem if these conditions remain for a long period. In fact, the lending-deposit spread of France’s banks has been very low for four years now, and below zero at times.

Housing markets could be another area in which financial risks could emerge. Figure 16 shows the evolution of mortgage loans in the euro area. These were growing at a rate of 5 percent annually at their peak in April 2016, after which growth rates fell to negative values in 2014 until they picked up around the time of the announcement and start of the PSPP.

Figure 16: Euro area monetary and financial institutions (excluding ESCB) lending for house purchase (year-on-year growth, %)

Source: European Central Bank. Note: 1) “Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP; 4) CSPP and expansion of PSPP. ESCB= European System of Central Banks. * See notes to Figure 2.

Figure 17: House price index (index, 2010=100)

Source: Eurostat. Notes: 1) “Whatever it takes’’*; 2) Announcement and start of PSPP. * See notes to Figure 2.

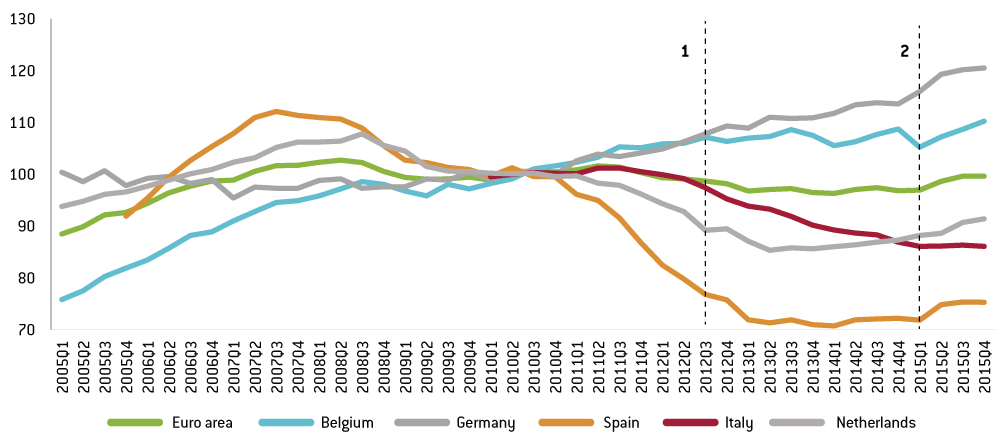

House price developments have however been very different across the euro area (Figure 17). As a whole, the euro area's house price index is now at roughly the same level as in 2010, and seems to have picked up following the announcement and start of the PSPP. Different countries, however, have seen very different developments in their housing markets. In Spain, which experienced a large housing bubble before the crisis, house prices continuously fell between 2007 and 2013, and have stayed fairly constant since then. Italy and the Netherlands have also seen corrections to their housing markets, but these have been less severe than in Spain. House prices in Germany and Belgium have been growing steadily and do not seem to have been overly affected by the crisis. Finally, it seems that house prices have been growing in the all countries shown except Italy since the start of the PSPP.

There has therefore been some effect in terms of generating new lending primarily for households, consistent with a general recovery in housing markets. On the corporate side however, there is still close to no new lending. The European Commission estimates that most euro-area countries have at least one sector that requires a reduction in debt of at least 10 percent (Bricongne et al, 2016). This inevitably reduces the demand for new credit, despite ample supply. We expect therefore that the low interest rate environment and the availability of liquidity in the system will not pose financial risks as long as the process of deleveraging continues.

Finally, between Draghi’s “whatever it takes” speech and right after the start of QE, stock markets values have increased (Figure 18). After that, however they have been declining. This reflects, among other things, increased uncertainty on world markets and, in 2016, uncertainty coming from China.

Figure 18: Stock market price index (Dow Jones Euro Stoxx 50 Price Index)

Source: European Central Bank. Note: 1) “Whatever it takes’’*; 2) PSPP announcement; 3) Start of PSPP; 4) CSPP and expansion of PSPP. ESCB= European System of Central Banks. * See notes to Figure 2

6 More QE : the expanded Public Sector Purchase Programme (PSPP) and the Corporate Sector Purchase Programme (CSPP)

It is a little too early to judge the effects of the ECB’s decision to expand government bond purchases from March 2016. Inflation is still hovering around zero and the government bond term spread has increased a little and stabilised.

In its latest action of purchasing corporate bonds, which started on 8 June, the ECB’s intervention is much more targeted. The Corporate Sector Purchase Programme (CSPP) involves outright purchase of investment grade euro-denominated bonds issued by non-bank corporations in the euro-area, and carried out by central banks in Belgium, Germany, Spain, France, Italy and Finland. Purchases are conducted both in primary and secondary markets; primary market purchases will not involve any purchases by public undertakings.

Figure 11 shows that credit to non-financial corporations, having been negative since 2012, has only recently stabilised broadly around zero. This implies that banks’ net lending to firms has not increased in four years2. And since banks are still very much in the process of building up capital to satisfy the new regulatory requirements, it is unlikely that they will issue significant new credit. The ECB is therefore aiming to reach the corporate sector directly by bypassing the banks.

Bypassing the banks at the current juncture might be useful but it is not sufficient. For this measure to be successful, the corporate sector needs to funnel the money it borrows to the real economy. If the money borrowed from the ECB is used for deleveraging, there will not be a beneficial effect on the economy in the short run (although there will eventually, as corporates become stronger). The ECB’s rationale is to take on the risk that banks are currently unable or unwilling to take.

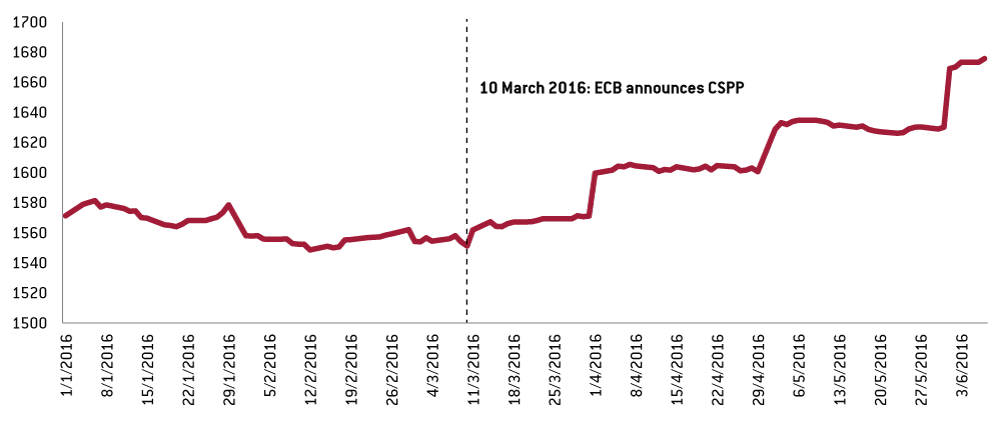

There is some evidence that corporates have sought to take advantage of the ECB decision by issuing a greater amount of securities following the March 2016 announcement (Figure 19).

Figure 19: Net issues (flows) of securities other than shares, excluding financial derivatives (Nominal value, Non-financial corporations, € billions)

Source: European Central Bank.

Figure 20: IBoxx total market value of the corporate investment grade bonds (€ billions)

Source: Thomson Reuters Datastream.

The total market value of the corporate investment grade bonds has increased substantially since then, in particular for high-rated bonds (Figure 20).

At the same time, bank profitability has once again been put under pressure because corporate yields have been depressed. Irrespective of the outcome of this intervention by the ECB, the role of the central bank as a ‘financial intermediary’ needs to be both an exception and short-lived. Lending to firms needs to be the outcome of a market mechanism. The ECB’s intervention is therefore a significant market distortion. It is necessary given the current conditions, but a distortion nonetheless.

Conclusions

Since the end of 2014, inflation has been at or very close to zero. With very little ability to move the actual interest rate further into negative territory, the ECB has resorted to unconventional measures. The latest of these includes a programme to purchase corporate bonds, which started on 8 June 2016.

Monetary policy so far has helped extend new credit to the euro-area economy and has positively contributed to growth. These effects are visible but small relative to the size and type of monetary policy interventions. There are no inflationary risks while slack continues to exist in the euro area. At the same time, we do not see any immediate financial risks arising from excessive debt as long as there is a need to reduce existing levels of debt to lower and more productive levels.

Quantitative easing can pose risks to the profitability of banks, a factor that could hamper the creation of new credit. This risk would increase if banks do not divert to other business models, a reason why European banking supervision has called for revisions to business models (Nouy, 2016). While a correction of bank margins was probably inevitable, the longer this pressure exists, the greater the threat to financial intermediation.

Draghi’s “whatever it takes” speech was a critical turning point for the euro area. This was sufficiently convincing to remove risks to the system’s financial stability. The QE that followed has helped to sustain progress made since then. Investment, employment and growth continue to move in a positive direction. At the same time, QE has made an important contribution to lowering the exchange rate (aided also by US monetary policy). Given the underlying uncertainties about the global economy, it is difficult to imagine how this result would have been attained without such aggressive intervention. Also, confidence appears to have stabilised with bond yields and spread volatility substantially lower and more stable. Markets still have faith that the ECB is able to manage inflation, given enough time. However, this confidence is beginning to wane given the scale and unconventional nature of the measures taken and the absence of inflation. It is unlikely that confidence will be sustained for long in the absence of a visible increase in aggregate demand and inflation. Given also that the marginal benefits of more central bank action are disputable, more of the required stimulus would have to come from elsewhere. This includes better use of fiscal space where it is available and more effective resolution of unproductive debt.

About the authors

Related content

The European Central Bank, inflation tolerance and the last mile

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition

What about the EU’s cohesion?

European capital markets union: make it or break it

Capital markets union has not delivered, but it should be given a last chance, with a focus on supervisory integration