An Italian job: the need for collective wage bargaining reform

Italy’s current system of centralised wage bargaining needs to be reformed. The system was designed without regard for the underlying industrial struc

Highlights

For references and footnotes, please see the PDF version of this publication.

- Since the mid-1990s, Italy has been characterised by a lack of labour productivity growth, combined with a 60 percent growth in labour costs, 20 percentage points above euro-area average consumer price growth. As a consequence, Italy has become less competitive compared to its euro-area partners, the profitability of its firms has dropped and real GDP-per-capita has flatlined.

- At the root of the substantial discrepancy between wages and productivity is Italy’s current system of centralised wage bargaining which, in many ways, is designed without regard for the underlying industrial structure and geographical heterogeneity of the Italian economy. This has fostered perverse incentives and imbalances within Italy.

- Collective wage bargaining, and in particular the determination of base salaries, should be moved from the national to the regional level for all contracts, in the public and private sectors. The Mezzogiorno, which might superficially be seen as losing out from this policy, would actually gain the most in competitiveness terms.

- Furthermore, measures should be taken so that, in the long run, the Italian industrial structure evolves into a less fragmented small-company-based economy. This firm consolidation would likely expand the use of firm-level agreements and performance payments, and would improve Italy’s productivity and competitiveness overall.

Background

Competitiveness is often presented as a nebulous concept, lacking a clear workable definition, and too vague to guide policymaking (Odendahl, 2016). Krugman (1994) goes as far as accusing it of being a “dangerous obsession”, insofar as it makes people believe that it is countries that compete on the world market, rather than firms. However, even Krugman espouses Laura D’Andrea Tyson’s definition of competitiveness as “the ability to produce goods and services that meet the test of international competition while […] citizens enjoy a standard of living that is both rising and sustainable” (Tyson, 1993).

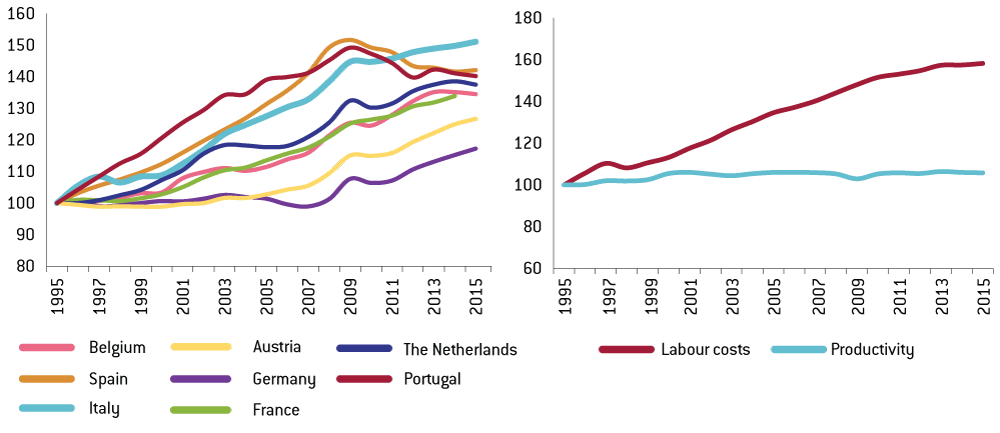

It is unquestionable that the euro-area crisis was preceded by significant competitiveness losses in several Mediterranean economies (Bénassy-Quéré, 2015). Several indicators illustrate the evolution of competitiveness at country and sector level, including current account balances, R&D expenditure, market share and productivity (Castellani and Koch, 2015). Thimann (2015) looks at a particular indicator of price competitiveness, namely nominal unit labour costs (ULC), and by decomposing it, shows how in some countries wages and productivity have diverged at a stunning rate. Italy is among them (Figure 1, right panel).

Since the mid-1990s, Italy has been characterised by substantially flat labour productivity growth, combined with a 60 percent growth in labour costs over an 18-year period. Obviously this divergence partly reflects inflation developments, although over that period prices in Italy increased by 10 percentage points less (51.3 percent). However, within a monetary union real wages deflated with domestic prices are not a relevant competitiveness benchmark (Thimann, 2015). What matters for purchasing and investment considerations are nominal prices in euros. And over a comparable period of time, consumer prices in the euro area increased by roughly 40 percent.

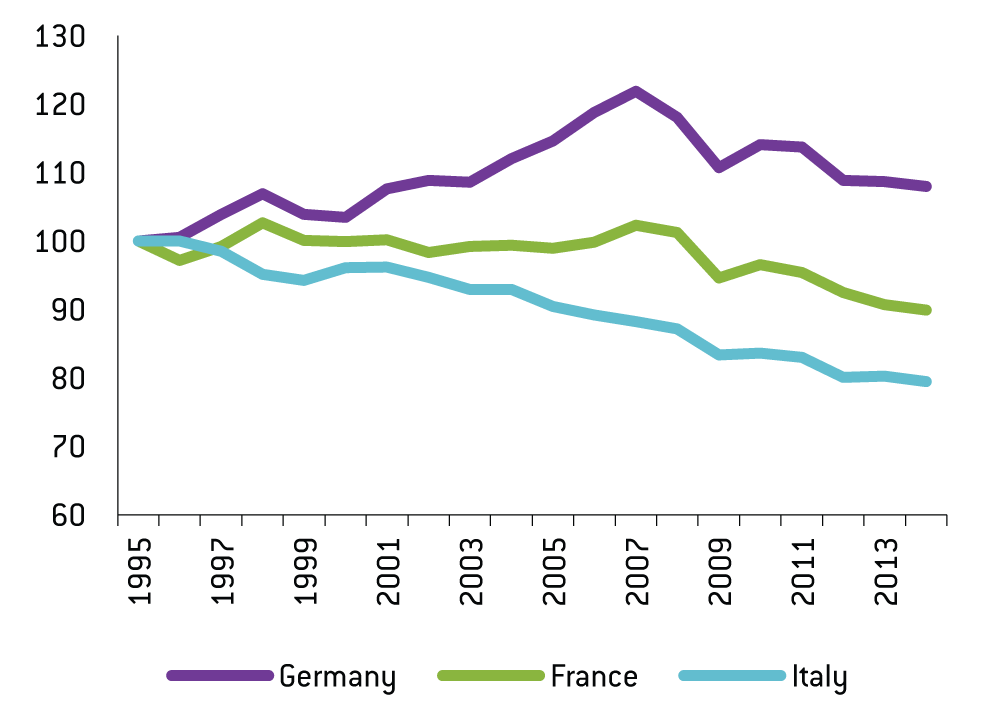

The result of this widening gap is that over the past two decades Italy’s ULCs have risen more than those of its euro-area peers (Figure 1, left panel) and firm profitability has been eroded. Figure 2 shows how the ratio of gross operating surplus (revenues net of the cost of intermediate goods and labour costs) to value-added shrank by a fifth since 1999, compared to -10 percent in France, and +8 percent in Germany.

Figure 1: Nominal unit labour costs (left panel) and labour costs and productivity developments in Italy (right panel), 1995=100

Source: Bruegel, Eurostat, OECD. Note: Productivity is computed as real GDP per hour worked; wages are computed as nominal compensation per hour worked. These two metrics are used to calculate nominal unit labour costs.

Figure 2: Ratio of gross operating surplus to value added, 1995=100

Source: Bruegel, Eurostat. Note: Gross operating surplus is defined as revenues of non-financial corporations minus the cost of intermediate goods (hence value added) minus compensation of employees.

In line with Tyson’s predictions, Italy’s real GDP-per-capita has flatlined (Terzi, 2015). Clearly, this is a great concern not only for Rome, but also for other European capitals, because a country with feeble growth and very high public debt (132.7 percent of GDP in 2015) is highly exposed to exogenous macroeconomic shocks and can be a source of instability for the whole euro area.

Italy stands out as a country that did not manage to embrace the ICT revolution and live up to the challenges posed by globalisation, as argued by Pellegrino and Zingales (2014). However, at the same time, its labour costs continued to increase. Interestingly, this trend did not reverse even with the inception of the crisis, as it did in Spain and Portugal.

While Italy’s top priority at this point clearly should be to resurrect productivity growth, ensuring that wages and productivity stay more aligned could be a first step towards restoring price competitiveness and preventing the generation of imbalances in the future. To understand why this did not happen so far, it is important to understand how wage bargaining works in Italy.

Wage bargaining in Italy

In Italy, almost all (97 percent) contracts in private-sector establishments are covered by collective bargaining arrangements (Eurofound, 2013). Bargaining can take place at industry- and company-level. Industry-wide negotiations between employers and unions establish the main items of the employment contract, mostly take place at national level, need to be renewed every three years and effectively set base salaries for each job category and level of seniority. On top of this, they also define, among other things, hours and holidays, health and safety, training and the use of temporary workers.

Company-level negotiations take place between the employer and the in-company representatives elected to work councils (RSU)1, and can modify only selected items of the nationally-negotiated contracts, where explicitly allowed by the latter (so-called escape clauses). This is the level at which performance premia are usually defined, on top of company-specific conditions.

In terms of coverage, employers that do not wish to apply the relevant industry-level national contract need to step out of the employer’s association that negotiated it. A prime example of this was FIAT in January 2012 leaving the employers’ association Confindustria. Conversely, employers can apply a collective agreement even if they are not a member of the employers’ association that signed it.

On the workers’ side, a collective agreement applies in principle only to the employees that belong to the negotiating trade unions2. In practice, labour courts have considered the base salaries defined in the collective arrangements as the benchmark for minimum fair pay3, effectively extending their validity to all workers.

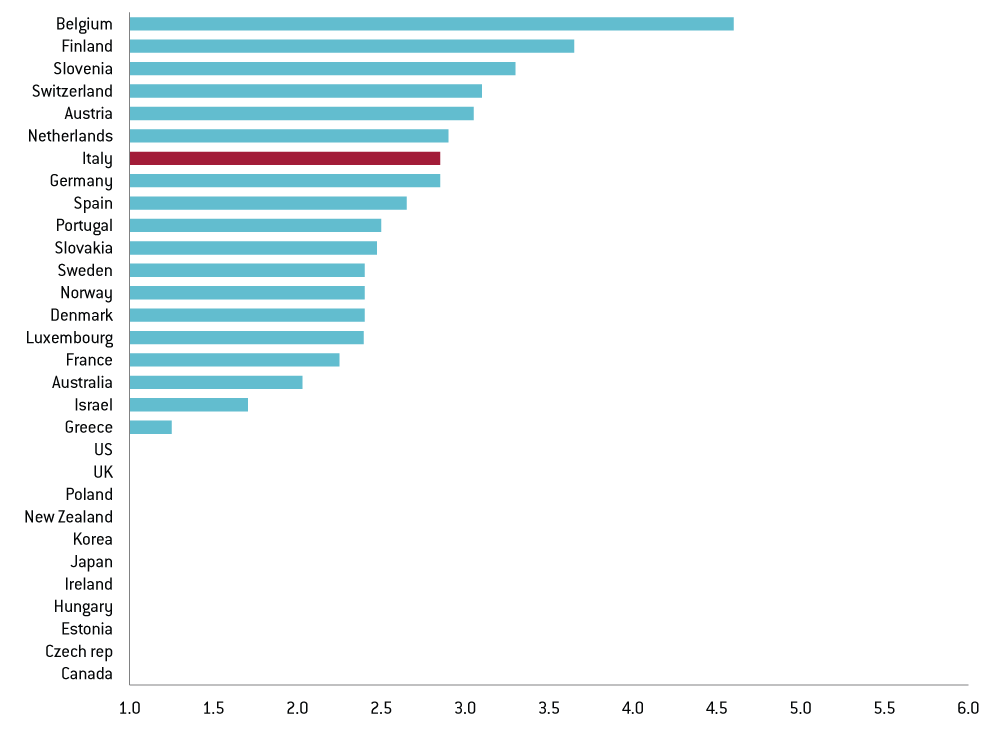

The result is one of the most centralised systems of wage bargaining among developed economies (Figure 3). According to a composite index of centralisation (CWG) developed by the Amsterdam Institute of Labour studies, Italy’s wage bargaining system is now the most centralised among southern European economies, after Spain, Portugal and Greece significantly overhauled their labour market institutions at the peak of the euro-area crisis.

Figure 3: Index of centralisation of wage bargaining, 0-6 (highly centralised)

Source: Amsterdam Institute for Advanced Labour Studies.

However, several highly competitive economies4, such as Switzerland, Germany and the Netherlands, also have levels of wage centralisation that are similar to Italy’s, if not higher. As such, a high ranking on the CWG index should not be interpreted necessarily as a warning sign of possible price competitiveness losses on the horizon (Calmfors and Driffil, 1988).

Instead, centralised wage bargaining, coupled with other institutional arrangements, can ensure that wages and productivity do not excessively diverge, hence safeguarding strict price competitiveness. Italy and Germany have more or less the same degree of centralisation of wage bargaining (Figure 3). Germany managed to keep wages more in line with productivity in the run-up to the crisis because labour unions responsibly chose to hold back on their compensation requests in order to safeguard the country’s competitiveness (The Economist, 2013). This decision can be attributed to some degree to Germany’s peculiar system of co-determination, in which employees’ representatives actively participate in the management of companies, fostering a climate of shared responsibility (Dustmann et al, 2014). In Italy, this did not happen.

Co-determination is not however the only way to ensure wages and prices move broadly in tandem. Belgium, another country where wage bargaining is almost fully centralised, has managed to prevent excessive wage increases thanks to the creation of a competitiveness council (Sapir and Wolff, 2015).

However, overlaying a competitiveness council on the current mechanism of nationwide centralised wage bargaining will not solve Italy’s entrenched price competitiveness problems. It should rather be part of a more wide-reaching reform package. This is because the current system in Italy seems to be designed without regard for the underlying industrial structure and geographical heterogeneity of the Italian economy, thereby fostering perverse incentives and imbalances.

A straitjacket for a heterogeneous country

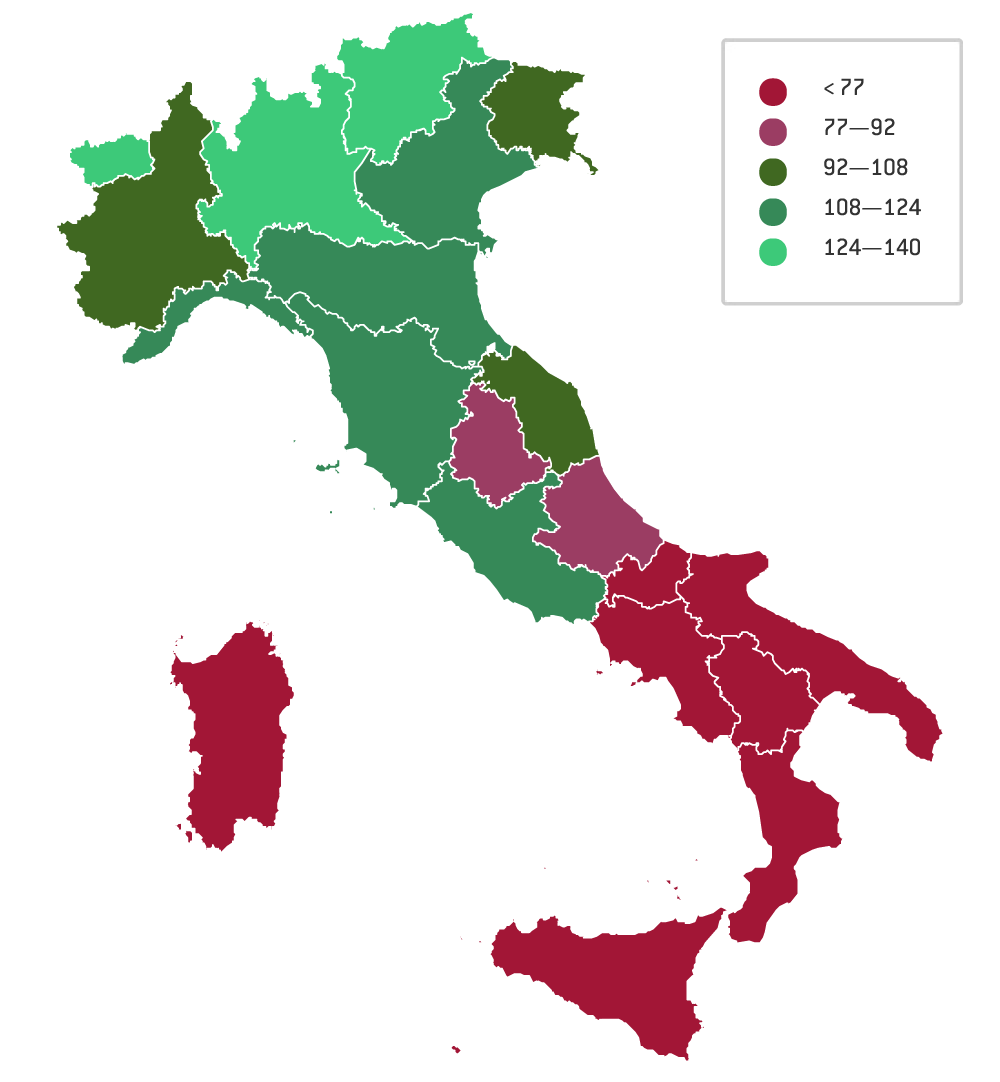

Italy is a highly divided country in terms of incomes in different regions (Figure 4). GDP per capita in the richest region (Val d’Aosta) is as high as €37,000, more than twice that of the poorest region (Calabria) at €16,000. More broadly, Italy is characterised by a richer north (117 percent of EU28 GDP per capita), an average centre (108 percent), and a poorer south and islands (64 percent and 65 percent, respectively). This long-enduring heterogeneity has been further intensified by the euro-area crisis since 2009. During the recession years the south was more affected than the north, while the nascent (weak) recovery seems to be being led by the north (The Economist, 2015a).

Figure 4: Nominal GDP per capita, Italy = 100

Source: Bruegel based on ISTAT.

These sharp income differences translate into different price levels in different regions. Although no official data on this is produced, Cannari and Iuzzolino (2009) estimate the cost of living to be as much as 20 percent lower in the Mezzogiorno (south and islands) than in the north. Analysing the data at provincial level, Boeri et al (2014) find differences that can be as great as 28 percent lower in some areas of Sicily compared to Lombardy.

The current system of national centralised wage bargaining, both in the public and private sectors, with its intricate grids of base wages for all job categories and levels of seniority, leads to perverse results, such as real wages being in many instances higher in the south than in the north, while productivity is significantly higher in the north (Boeri et al, 2014). Clearly, the price the Mezzogiorno pays for this is a higher unemployment rate than the north, as adjustment cannot take place on the basis of wages and happens on quantity (Table 1).

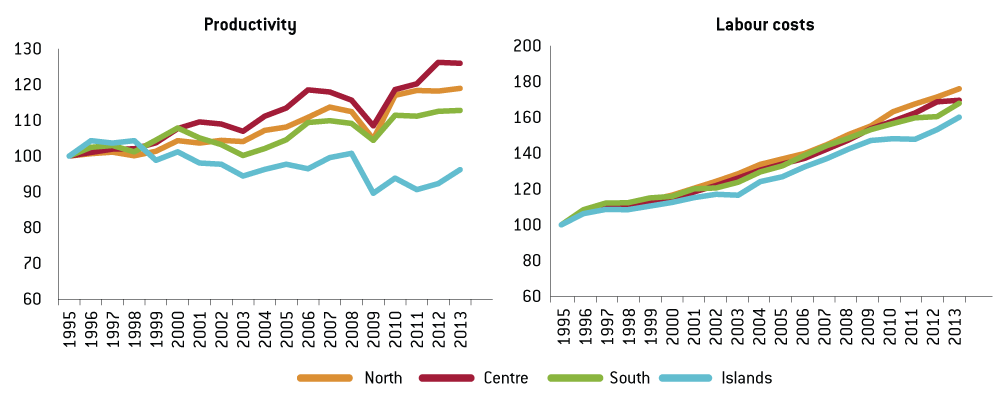

Productivity developments are also quite different across Italy. Figure 5 plots real GDP per full-time equivalent employee, in order to correct for differences in the use of part-time workers, for the tradable sector (proxied by manufacturing). Interestingly, since 1995, productivity has increased by 25 percent in the centre, while it is now below its 1995 level in the islands (Sicily and Sardinia). In this context, Figure 5 (right panel) shows how wages have increased in a very similar way across Italy (and by too much in all regions). The resulting nominal ULCs increased more in the islands (66 percent) than in the north (48 percent) over this time period.

Figure 5: Productivity and labour-cost developments, tradable sector, 1995=100

Source: Bruegel based on ISTAT. Note: Tradable sector here proxied by manufacturing.

Figure 6: Employment by enterprise size, 2012

Source: OECD Entrepreneurship at a Glance 2015.

Following Thimman (2015), Figure 5 implies that in effect price competitiveness in the Mezzogiorno has been eroded even more than in the north by a nationally centralised wage bargaining system. All things being equal, an entrepreneur is today even less likely to choose Sicily or Sardinia as her place of business, as she would see her profits squeezed even further, while remunerating more production inputs – most notably labour – that are adding less value than two decades ago. Interestingly, similar dynamics played out in Germany in the aftermath of reunification in 1990 (Box 1).

We should also briefly draw attention to the underground economy. Studies highlighting inter-regional differences in Italy are often downplayed or dismissed on the grounds that the underground economy, which is more prevalent in the south, is not picked up by official statistics, hence distorting the overall conclusions. While this heterogeneity in illegality is documented (see for example Frenda, 2010), it does not invalidate the reasoning outlined above. Collective wage bargaining only applies to the legal economy, and should thus cater to regional disparities in productivity and wages in the official sector6.

Connected to this point on the underground economy is the consideration that having a large wedge between the Mezzogiorno’s equilibrium level of wages and the base salaries imposed via centralised wage bargaining might actually be a distorting incentive. As companies look for alternative ways to safeguard their competitiveness and remain in business, they might resort to informal employment. Clearly, this is also favoured by an environment in which the public authorities have less control of the territory.

Escape clauses and firm-level agreements

A legitimate question worth raising at this point would be why Italy’s two-tier system of wage bargaining, which has allowed for firm-level agreements since 1993, has not managed to prevent these macroeconomic imbalances from emerging. There are a number of reasons. First, and foremost, firm-level agreements can exploit selected escape clauses determined in sector contracts, but are not allowed to overrule base salaries set at national level.

However, firm-level agreements do allow for productivity premia which can top up base salaries and, at least in principle, are aimed precisely at anchoring more firmly total compensation and output per worker. The reasons why this variable salary component has not been at least somewhat effective as an automatic competitiveness safety valve are: (i) it represents only a small share of employees’ total compensation, and (ii) only few firms decide to embark on the journey of negotiating firm-level agreements (roughly 30 percent). Productivity premia are therefore small and not widely used.

This might seem at first sight surprising but is rooted in the peculiar industrial structure of the Italian economy, which is characterised by a multitude of very small firms and very few large companies, at least by international standards. Almost 60 percent of firm workers (and therefore of contracts) are employed by a company that has fewer than 20 employees (Figure 5). This compares to 40 percent in the Netherlands, 30 percent in Germany, and 18 percent in the United States.

In general, small firms are less inclined to go down the route of bargaining at firm-level, given the high costs involved. However, this reluctance is exacerbated by the current two-tier system, which seems to be have been designed without taking into account the structure of the Italian private sector. First, as discussed above, firm-level agreements must be negotiated between an employer and in-company work councils (RSA/RSU). However, data from the Italian National Institute for Statistics and National Economic and Labour Council (ISTAT and CNEL, 2013) shows how the presence of in-company RSA/RSUs is proportional to firm size, and in particular only 7.5 percent of small firms (10-49 employees) host work councils, while for firms with 50-199, 200-499 and 500+ employees, the figures are 34.7 percent, 58.8 percent and 61.5 percent respectively.

For firms without in-company work councils, the protocol would be to escalate the negotiation to a local employers’ association, which would liaise with the local labour union representatives. This is obviously far from optimal because it brings the problem back to square one, making it harder to tailor the contract to a company’s specific needs, with potentially high (time) costs, also because firm-level contracts must be renegotiated every three years, and offering limited benefits given the restrictive nature of escape clauses. In fact, there are also some instances of escape clauses in industry-level agreements that prohibit their use by smaller companies7.

The picture that emerges from the ISTAT and CNEL survey is one in which the use of firm-level agreements is strongly inversely related to firm size. In particular, only 27.9 percent of firms with 10-49 employees made use of firm-level agreements in 2012-13, compared to 73.9 percent of companies with 500+ employees. And not all firm-level contracts activate the productivity clauses. All in all, productivity premia are being used only by 9.6 percent of small firms, compared to 63.6 percent of large companies in Italy, for a total of 13.4 percent of all firms.

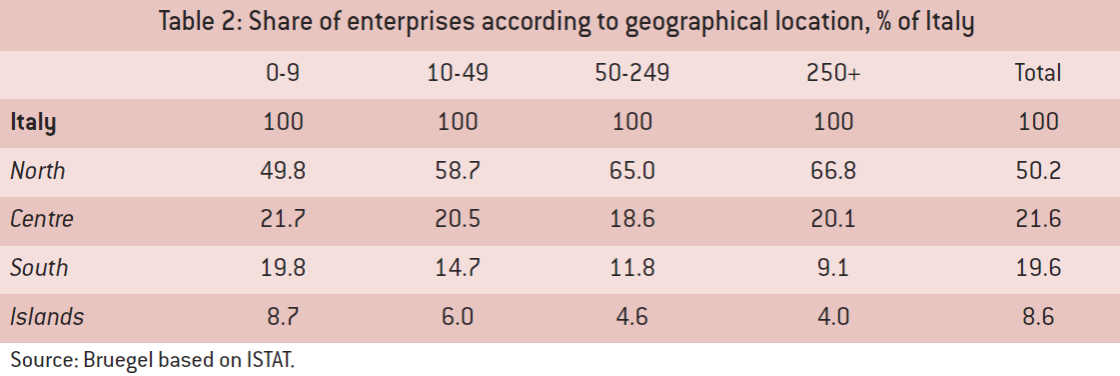

Firm size in Italy also has regional aspects. More than half (50.2 percent) of Italy’s firms are located in the north, and the picture is more bleak when breaking it down by size (Table 2). In particular, 66.8 percent of companies with 250+ employees, the size class making greater use of productivity premia, are located in the north, compared to only 4.0 percent in the Islands. Such a distribution clearly helps reinforce the productivity and competitiveness divergence between the north and the Mezzogiorno.

The south is also penalised because, as nominal wages are already set high by national contracts, there is less room for manoeuvre than in the north to top them up with productivity premia at firm-level. Lower base wages would instead allow better use of productivity bonuses, contributing to the revival of labour productivity. Starting from Lazear (2000), the literature is unanimous in finding strong productivity improvements associated with the introduction of monetary incentives (for evidence on Italy, see for example Lucifora and Origo, 2012). This is because individual workers may exert increased effort – incentive effect – and because of a relocation effect, whereby workers will have an added incentive to join high-productivity firms (Petrin et al, 2011)8.

A reform proposal

Over the past two decades, Italy’s social partners have come together several times to amend the system of collective bargaining, not only in 1993 as mentioned above, but also in 2009 and 2014. As Eurofound (2015) neatly puts it, Italy’s “whole industrial relations system appears to be searching for a new structure”. In strict economic terms, bringing wage bargaining to the firm-level would be the first-best solution. As such, extending the use of escape clauses is often presented by economists as a silver-bullet. However, our analysis suggests it would not be, given that most (small) firms are still unlikely to be able to exploit the escape clauses fully within the current setting. Micro-enterprises have proven unready to enter into time-consuming, repetitive negotiations with labour unions, and the latter cannot be bypassed within the current constitutional order. As such, extending the use of escape clauses should be part of a more holistic reform of collective bargaining.

A comprehensive reform should rather be composed of a wide variety of measures, aimed at (1) alleviating the problems connected to the current system already in the short term, and (2) fully addressing them over a longer term.

For the short term, collective wage bargaining, and in particular the determination of base salaries, should unequivocally be moved from the national to the regional9 level for all contracts, in the public and private sector. This (second best) measure is aimed at tackling immediately the geographical differences we have discussed, and should be seen as a first step in the direction of wage decentralisation.

While at first sight it might sound problematic that the government of a unitary state should pay its employees differently based on their location, it is crucial that this reform applies also to the public sector. If, as a result of regionalisation, salaries in lower-productivity regions were to begin adjusting in the private sector only, the gap between public and private sector wages would widen. As discussed by Giordano et al (2011), relatively high wages in the public sector crowd out the private sector, draining the most skilled workers, forcing firms into a wage race to the top (Lamo, Perez and Schuknecht, 2008), leading to deteriorating competitiveness and greater unemployment problems. Caponi (2014) shows how this phenomenon is already at play in Italy, contributing to up to 40 percent of the unemployment gap between the north and the south. Crucially, this problem would not be addressed by simply promoting firm-level bargaining or escape clauses.

In terms of political feasibility, this regionalisation should not be seen as overly controversial. First, this is already common practice for selected sectors such as agriculture, construction and tourism. Second, a move to the regional level could hardly be seen as a radical attack on the current system of centralised wage bargaining, but is rather common practice among even highly centralised countries with a high degree of territorial heterogeneity (eg Germany). Third, parts of the labour unions (most notably CISL, and partially UIL10) have expressed their readiness to make more use of regional-level bargaining, which currently in Italy is used to a very limited extent. Finally, a somewhat similar mechanism, which allowed for differentiation in salaries at sub-national level based on living costs, was in place in Italy for almost 20 years in the immediate post-war period. This suggests a similar arrangement could be compatible with Italy’s constitutional order.

Once this decentralisation step is taken, a consortium of competitiveness councils could be established at the regional level given that this is where the collective bargaining would take place, in line with the spirit and rationale of Sapir and Wolff (2015). This would be aimed at ensuring a better tracking of productivity and wage developments.

One word of caution is warranted. Some will oppose such measures, claiming they penalise the south, which would eventually see lower nominal salaries compared to the north. While a uniform economic development of the country can surely be regarded as desirable, artificially equalising salaries is a Pyrrhic victory. As the example of Germany’s reunification illustrates (Box 1), excessively high nominal wages with respect to productivity are likely to have contributed to the south’s higher level of unemployment and low investment levels. In order to achieve territorial convergence, the government should rather concentrate on increasing productivity levels in the south, by means of investment in infrastructure, human capital, improving the efficiency of the public sector11, combating organised crime and so on.

Furthermore, measures should be taken to alleviate the current difficulties small and medium enterprises have in using firm-level agreements, and thus productivity premia. This could take several forms, such as outlawing the limitation of escape clauses based on firm size and removing the 15-workers requirement to set up work councils (RSU). Finally, the current preferential tax rate on productivity premia (10 percent up to a ceiling of €2000 per worker) could be further strengthened for small enterprises.

While all these measures will surely help, in order to address more radically some of the problems associated with the current two-tier system of wage bargaining, measures should be taken so that, in the long run, the Italian industrial structure evolves into a less fragmented, small-company-based, economy. In order to reach that stage, as numerous studies have pointed out, policy needs to include: (i) radical product market liberalisation, (ii) improving firm access to credit and financial markets, (iii) improving judicial efficiency, and (iv) reforming bankruptcy laws (see for example Calligaris et al, 2016; Clementi and Hopenhayn, 2006; OECD, 2003; Giacomelli and Menon, 2013; Kumar et al, 1999). This consolidation is not only likely to expand the use of firm-level agreements and productivity clauses, completing the process of full wage decentralisation, but also to improve Italy’s productivity and competitiveness overall (Tiffin, 2014). As Altomonte et al (2016) show, large firms are more likely to invest more in R&D and innovate, be more successful on international markets and exploit global value chains. Moreover, large firms tend to attract better management, which in turn fosters productivity, profitability, growth and firm survival (Bloom et al, 2014).

Conclusions

As a country that has experienced over the past two decades rising nominal wages, flat productivity and essentially no GDP-per-capita growth, Italy’s economic malaise is undeniable. Policies could be put in place to ensure, at least over the short run, that Italy retains its price competitiveness. It must be noted, however, that as stressed by Altomonte et al (2016), competitiveness in developed countries is connected very strongly with non-price elements. This suggests that, after having reformed collective wage bargaining in order to tackle some of the large macroeconomic disequilibria engendered by it, particularly within the country, Italy’s government should focus on reviving the country’s ailing productivity growth.

Many of the reforms we have suggested are self-reinforcing. Ensuring widespread use of productivity premia is likely to foster productivity itself. At the same time, pushing through reforms that allow firms to grow will increase their productivity and also grant them easier access to firm-level agreements.

A reform of collective wage bargaining, which ultimately involves a spontaneous agreement between social partners, can only be effective if widely discussed with representatives of labour unions and industry associations ex ante. When in the past governments tried to implement such reforms by decree (eg in 2011, at the peak of Italy’s sovereign debt crisis), there was industrial conflict and a suboptimal take-up of the reform’s innovations. In this context, the government’s willingness to discuss the introduction of a statutory minimum wage, to complement wages implicitly set by industry-wide contracts, could surely improve the political feasibility and palatability of a progressive decentralisation of wage bargaining.

About the authors

Related content

The great fiscal lever: An Italian economic obsession

In the Italian macroeconomic context, many are convinced that if only we had a large enough fiscal lever, we could set in motion an economy that has s

Improving the efficiency and legitimacy of the EU: A bottom-up approach

The 2019 European elections promise to be a watershed moment for the EU. A recent Bruegel paper made the case for restructuring the Union’s model of g

The Value of Money, Controversial Economic Cultures in Europe: Italy and Germany

A discussion of Italian and German macro-economic cultures and performances.

An alpine divide? Comparing economic cultures in Germany and Italy

A discussion of Italian and German macro-economic cultures and performances.