Trumping Trade

What’s at stake: Trade is a central topic in the US presidential campaign, with both candidates expressing some degree of criticism about past trade p

Bonus: if watching the debate unsettled you, think that Jonathan Mahler at the NYT had to do it with sounds off and no captioning! The idea was to test the theory that what presidential candidates say during debates is less important than what they look like while they’re saying it. Watch some of his clips, if you have a thing for mute surrealist cinema

A paper by Peter Navarro and Wilbur Ross, both senior policy advisors to the Trump campaign, sets out the Trump camp’s position. They argue that Trump’s trade plans will bring in $1.74 trillion of additional Federal tax revenues. Assuming wages are 44 percent of GDP, they argue that eliminating the US trade deficit would result in $220 billion of additional wages. This additional wage income would be taxed at an effective rate of 28 percent, yielding additional tax revenues of $61.6 billion. Furthermore, businesses would earn at least a 15% profit margin on the $500 billion of incremental revenues, which would translate into pretax profits of $75 billion. Applying Trump’s 15% corporate tax rate, this results in an additional $11.25 billion of taxes. This would leave businesses with $63.75 billion of additional net profit which must be distributed between dividends and retained earnings. If businesses pay out one third of this additional profit as dividends and these $21.25 billion worth of dividends are taxed at a rate of 18%, this yields another $3.8 billion of taxes, after which there remains $17.45 billion of net income. Together, these tax revenues from wage, corporate, and dividend income total $76.68 billion per year and over the standard ten-year budget window, this recurring contribution to the economy cumulates to $766.8 billion dollars of additional tax revenue.

Navarro and Ross then argue that two more sets of revenue should be added to this total. Under the dividend payout schedule, businesses will retain $42.5 billion of cash flow after paying both taxes and dividends. Under the assumptions of the paper, reinvesting this $42.5 billion each year would generate another $120.21 billion of pretax profits and taxes of $18.04 billion over the standard 10-year budget window. Adding these increments to the previous calculation results in a ten-year direct incremental contribution to Federal tax revenues of $766.8 billion in 2016 dollars, which turn into $869.76 billion when a 1.1082 inflation factor is applied. To account for multiplier effects, Navarro and Ross also add a multiplier of 1.0, which would produce a grand total of $1.74 trillion of additional Federal tax revenues from trade .

Marcus Noland, commenting on the Navarro and Ross paper over at PIIE, says that the authors owe much to the literary genre of “magic realism”. Magic realism was developed by Latin American writers in the 1970s, and its most distinguishing feature is a mix of wild juxtapositions and metaphysical leaps. According to Noland, the thinking that gets Navarro and Ross to the $1.74 trillion figure is truly magical. He argues that their assessment of the causes of weak economic growth entirely ignores the ongoing debate about the sources of productivity growth and the possibility that the rate of technological change is slowing. Instead, they focus on trade. Economists generally believe that the magnitude of a nation’s trade deficit fundamentally reflects the difference between saving and investment. Trade policy can affect the sectoral and geographic composition of the deficit, but in the long run the trade balance is determined by the savings-investment balance. If you want to lower the nation’s trade deficit, increasing the saving rate would be the right place to start - , not launching a trade war. But there is no word of this in Navarro and Ross’ paper, which is all about perfidious foreigners and incompetent trade negotiators. Noland accepts that this might make for a more exciting storyline, but it does not constitute a persuasive defense of their solution to the trade deficit.

Marcus Noland, Gary Clyde Hufbauer, Sherman Robinson, and Tyler Moran at the Peterson Institute of International Economics have a report assessing trade agendas in the US presidential campaign.

While Clinton has expressed skepticism about aspects of trade deals in the campaign, Nolan et al. argue that in effect she represents stasis. In her political career, Clinton has not taken a doctrinaire position on trade. As First Lady she supported NAFTA, but while campaigning for the 2008 Democratic presidential nomination, she described NAFTA as “a mistake.” While representing New York in the Senate, she voted in favor of six preferential trade deals (FTAs with Chile, Singapore, Australia, Morocco, Bahrain, and Oman); against two (the Central American Free Trade Agreement and the FTA with Panama); and did not vote on two others (the agreements with Jordan and Peru). She expressed opposition to the FTAs with Colombia and South Korea. Later, while serving as secretary of state, Clinton reversed her opposition to these agreements and helped persuade Congress to pass them.

In the 2016 campaign, Clinton has made enforcement of existing trade laws, aimed at preventing abuses by trading partners, the centerpiece of her trade policy. She supported TPP as secretary of state, calling it “the gold standard” of trade agreements, but she has come out in opposition to it during the campaign. Some TPP advocates hope that the agreement could be ratified during a lame duck session (between the election and the seating of new Congress in January). Others hope that if she were elected, Hillary Clinton could replicate Bill Clinton’s maneuver in the early 1990s, when he opposed NAFTA while campaigning against George H. W. Bush and then supported its passage in office. Nolan et al. argue that this would still have implicit costs, citing estimates according to which each year’s delay in implementing TPP represents a $77 billion to $123 billion permanent income loss for the United States, depending on the discount rate applied Petri and Plummer (2016).

Trump has stated that he would impose a 35 percent tariff on imports from Mexico and a 45 percent tariff on Chinese goods, as a countervailing action against alleged currency undervaluation. He has proclaimed that he would “rip up” existing trade agreements, renegotiate NAFTA and may withdraw from the WTO over the imposition of tariffs, possibly firm-specific, on products made in Mexico by US firms. A first question is whether the President actually has the legal authority to do this kind of thing. In a legal analysis, Gary Clyde Hufbauer argues that there is ample precedent and scope for a US president to unilaterally raise tariffs as Trump has vowed to do. Any effort to block Trump’s actions through the courts, or amend the authorizing statutes in Congress, would be difficult and time-consuming.

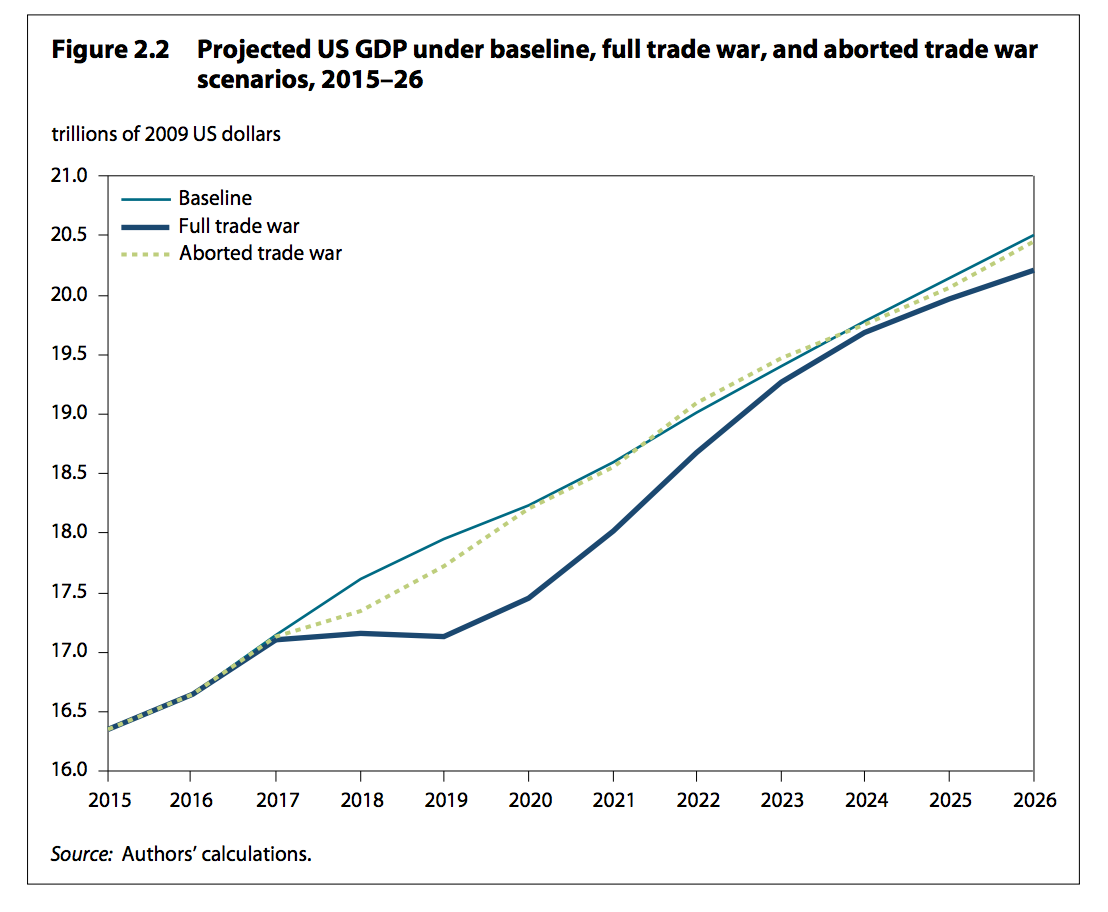

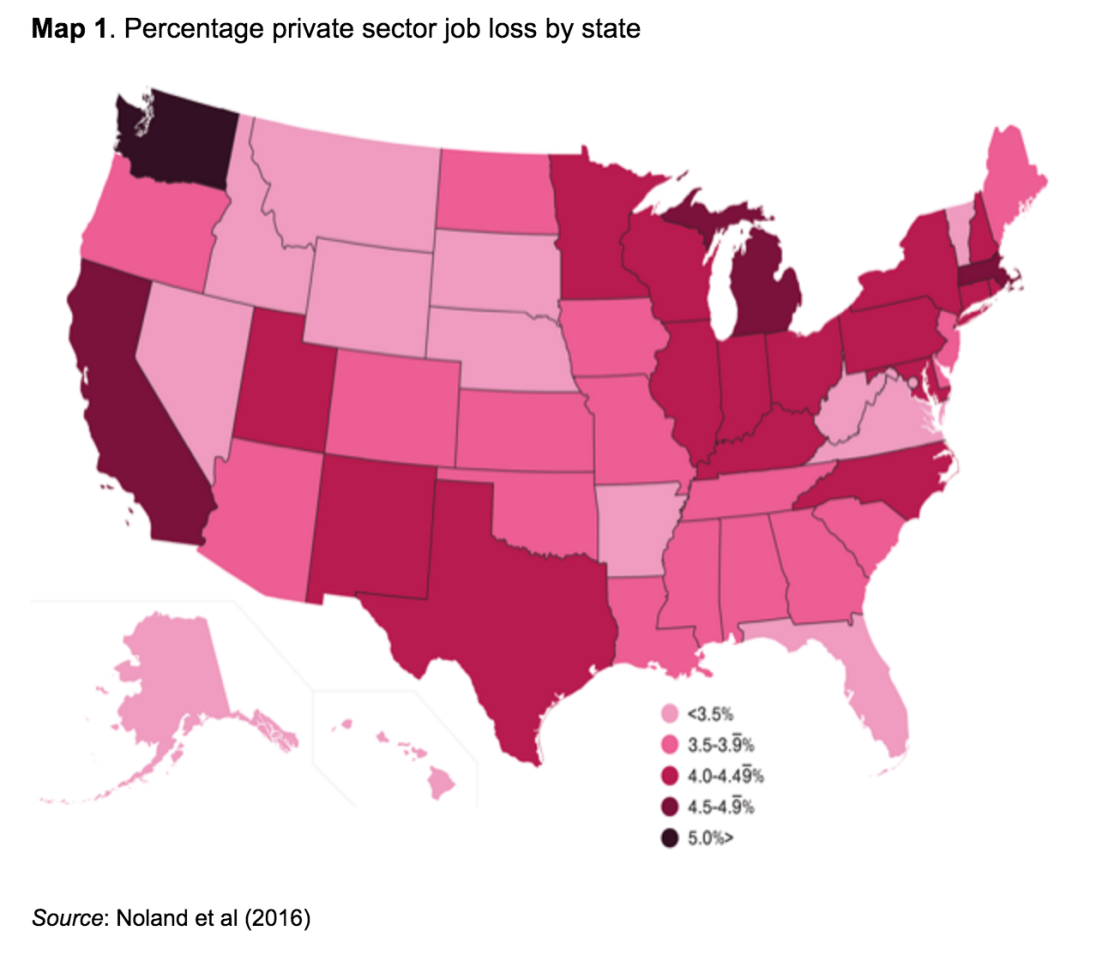

A second question regards the economic effects. Nolan et al. extend a macroeconomic model from Moody’s Analytics and estimate that Trump’s proposals on international trade, if implemented, could unleash a trade war that would plunge the US economy into recession and cost more than 4 million private sector American jobs. In a separate chapter Noland analyzes the impact of trade policies advocated by both Trump and Clinton on the United States’ foreign policy interests. Pulling out of the TPP, as both candidates promise to do, would weaken US alliances in Asia and embolden its rivals, thus eroding US national security. Noland also warns that abrogation of NAFTA, as Trump threatens, would deliver a severe blow to Mexico’s economic and political development that could increase, not decrease, the flow of illegal migrants and drugs into the United States (see figures 1 and 2). An earlier comprehensive analysis of Trump’s economic policies by Moody’s is accessible here.

Figure 1

Figure 2

On the morning after the debate, Paul Krugman said that Trump on trade was “ignorance all the way”. Krugman points in particular to Trump’s statements in which he seemed to think that Mexico’s VAT tax rate is actually an unfair trade practice on US imports to Mexico. In a follow up post, Krugman points out that the Republican campaign’s white paper on economics has a VAT discussion that is utterly uninformed, suggesting Trump was probably saying ignorant things fed to him by incompetent economic advisers. More broadly, Trump’s whole view on trade is that it is all about dominance, and that the US is weak. And even if you think we have pushed globalisation too far - Krugman says - even if you are worried about the effects of trade on income distribution, that is just a foolish way to think about the problem. So “Trump blustered more confidently on the subject of trade than on anything else, but he was talking absolute garbage even there”.

Both Krugman and Tyler Cowen quote a paper by Joel Slemrod on the subject of whether VAT promotes exports. Slemrod argues that this is not the case, and suggests a three-step process to convince oneself. First step, understand why a uniform VAT is equivalent to a uniform RST [retail sales tax]; both tax domestic consumption regardless of where goods or services were produced. Second step, calmly reassure oneself that, as is intuitive, an RST does not favor domestic over foreign production and neither encourages nor discourages exports or imports. This implies step three: that a VAT (like an RST) neither encourages nor discourages exports or imports. If step three fails, return to steps one and two until fully convinced.

Greg Mankiw agrees with Krugman on Trump’s advisers. Their analysis of trade deficits boils down to the following: We know that GDP=C+I+G+NX (consumption + investment + public spending + trade balance). The trade balance (NX) is negative, therefore, if we somehow renegotiate trade deals and make NX rise to zero, GDP goes up! They calculate this will bring in $1.74 trillion in tax revenue over a decade, but of course you can't model an economy just using the national income accounts identity. Trade deficits go hand in hand with capital inflows, so an end to the trade deficit means an end to the capital inflow, which would affect interest rates, which in turn influence consumption and investment. Mankiw argues that such calculations might make sense in the simplest Keynesian Cross model, in which investment is exogenously fixed and consumption only depends on income. But that is surely not the right model for analyzing the impact of trade policy over the course of a decade.

Jared Bernstein writes that, before the first presidential debate fades into the next news cycle, we need to realize that we need a new paradigm for trade policy. The outsider campaigns of Trump and Sanders, along with the realities of the many people and communities hurt by globalization, have elevated international trade as a major issue in this election. Trump advertises an unrealistic nostalgia, a return to a time when trade flows were a fraction of their current size. His statements during the debate underscore the fact that there is no coherent plan to get back there even if we wanted to. Clinton correctly points out that “we are 5 percent of the world’s population; we have to trade with the other 95 percent.” She aspires to reshape, not restrain, globalization. What’s needed is a framework for the type of “smart, fair trade deals” that Clinton says should be the norm. Yes, that framework should include enforceable disciplines against other countries’ currency management, something both candidates support. But much more is needed.

Bernstein refers to a proposal paper published by himself and Lori Wallach, which include both process reforms and new negotiating objectives. Bernstein and Wallach argue that the process by which trade agreements are negotiated must change in the direction of enhanced transparency and accountability. They also propose a set of initiatives that should be part of what they call the “new rules of the road for trade”. These initiatives include enforceable currency disciplines, enforceable and substantive labor and environmental rights and standards, tighter terms regarding “rules of origin”, facilitating export opportunities, combating transshipment and selecting appropriate trade partners. Bernstein and Wallach argue that their ideas, if adopted, would increase the transparency of trade negotiations, reduce corporate influence over the eventual agreements, discontinue protectionist practices and provisions that put sovereign laws and taxpayer dollars at risk, and strengthen environmental, health, and labour standards in the US and abroad.

About the authors

Related content

How Europe can sustain Russia sanctions

Russia's war in Ukraine has underscored the need for Europe finally to invest more in its own defence and security. Such an outrageous act of aggressi

The microeconomics of Christmas

Review of major contributions to the literature on the controversial topic of the deadweight loss of Christmas.

Global supply chains: lessons from a decade of disruption

This paper revisits the effects of three shocks on the functioning of global supply chains.