Should the EU have the power to vet foreign takeovers?

Should the EU have the power to vet foreign takeovers? André Sapir and Alicia Garcia-Herrero debate the issue, which has become topical in view of rec

In July, the German government expanded its powers to block the foreign takeover of German companies. The decision was a reaction to the accelerating acquisition of German high-tech firms by Chinese companies, including the landmark purchase last year of Kuka, Germany’s largest maker of industrial robotics, by Midea, a Chinese appliance maker.

The move by the German government followed almost immediately an aborted attempt by France, Germany and Italy to set up an EU mechanism to monitor and, if needed, veto third country buyouts.

According to press reports, the three countries’s demand was met with strong opposition from a majority of EU countries at this year’s June European Council summit. As a result, the summit conclusion did not include an invitation to the Commission to “examine the need and ways to screen investment from third countries in strategic sectors”, as a previous draft had proposed. Instead it simply called on the Commission to “analyse investments from third countries in strategic sectors, while fully respecting member states’ competences”.

But this setback for France, Germany and Italy may only be temporary. The Financial Times recently reported that, in his State of the Union speech on 13 September, the European Commission president, Jean-Claude Juncker, “will call for more rigorous screening of foreign takeovers of European companies, as it seeks to address mounting concerns about a surge of Chinese investment into the bloc’s high-tech manufacturing, energy and infrastructure sectors.”

So, should the EU rethink its position and give the Commission the power to vet foreign takeovers? Here two Bruegel scholars give different answers to this timely question.

André Sapir: YES, but…

There are three reasons why the EU should have the power to vet foreign takeovers.

The first reason is that 13 of the EU’s 28 members already have national legislation for screening takeovers to evaluate whether they constitute a threat to national security or other public policy goals.[1] Having an EU mechanism instead of national mechanisms would be preferable. It would be better for the functioning of the single market. Having different national rules creates problems for dealing with firms that operate in several EU countries. Better to have a single EU rule for the smooth functioning of the single market. An EU-level vetting process also offers greater size and leverage. Having a single EU rule gives each EU country greater leverage over foreign countries than having a national rule.

There is obviously a counter-argument to this reasoning. It is that 15 EU members do not feel the need for legislation to screen foreign takeovers, presumably because they consider that foreign investment is always desirable. Moreover, even among the 13 countries that currently have a system to vet foreign takeovers, there are many differences in the rules which reflect differences in national preferences.

The question, therefore, is whether the benefits of a single EU rule (smoother functioning of the single market and greater leverage vis-à-vis foreign countries) outweigh the costs associated with different national preferences. This is obviously a difficult question. However, we should remember that EU members have extended, with the Lisbon Treaty, the EU’s exclusive competence in the field of trade to cover foreign direct investment (with the exception of dispute settlement between investors and states). This implies that EU countries may be willing to forego national preferences for common EU action in the area of foreign takeovers as well.

The second reason is that the United States has long vetted foreign takeovers, through its Committee on Foreign Investment (CFIUS. CFIUS has sometime even prevented foreign firms from buying EU companies. For instance, last year CFIUS blocked the purchase of a US-based unit of Philips, the Dutch giant, and of a German-based chip equipment maker, Aixtron, by Chinese companies on national security grounds.

The third reason is China. There is a strong asymmetry between the EU and China regarding the treatment of foreign investment by state authorities. This asymmetry basically stems from the fact that Chinese state-owned enterprises (SOEs) are “bigger, more pervasive and more dominant than their EU counterparts”, as Alicia Garcia-Herrero and Jianwei Xu explain in a recent Bruegel paper. The implication is that Chinese investors in the EU are often connected to the Chinese state, which potentially raises national security issues that are rarely scrutinised by EU states. Typically, whether they are connected to the Chinese state or not, Chinese investors are treated on equal footing with EU investors in the EU. On the other hand, EU investors in China are rarely connected to EU states, yet they often encounter great difficulty both in setting up production and, if they succeed, in competing with local firms that benefit from state connections.

An EU mechanism to vet third country buyouts, including from China, would strengthen the hand of the EU in its bilateral investment negotiations with China. These started more than three years ago and are making slow progress due to the vexing (for the EU) SOE question.

Taken together, these three reasons seem compelling in favour of setting up an EU mechanism to monitor and, if needed, stop foreign takeovers.

There are, however, two important questions that need to be addressed before signing up to the idea.

The first concerns the scope of the strategic sectors or assets that would be scrutinised by the new mechanism. This is crucial to ensure that this mechanism serves genuine security concerns rather than protectionist interests.

The second question concerns the heterogeneity of preferences within the EU. For instance, there is understandable worry is some EU countries, especially those where foreign direct investment is badly needed to improve their growth prospects, that an EU mechanism to vet takeovers may slow down the inflow of such investment. One way to deal with this issue, and more broadly with the heterogeneity of preferences within the EU towards, would be to let EU states activate the EU mechanism at their request rather than having the EU decide when to activate it, except under certain well-specified conditions.

Combining these two questions, the scope and the heterogeneity, one could have a two-level system. Under certain narrow conditions, the EU mechanism would need to give its green light for a foreign takeover. Under somewhat broader conditions, the EU mechanism could be involved if the relevant member state so wishes.

For the cases when the involvement of the EU mechanism would be mandatory, the body in charge of the mechanism (presumably the European Commission) would make a recommendation to the Council, which would ultimately decide whether to block or not the proposed takeover.[2]

Alicia Garcia-Herrero: NO, but…

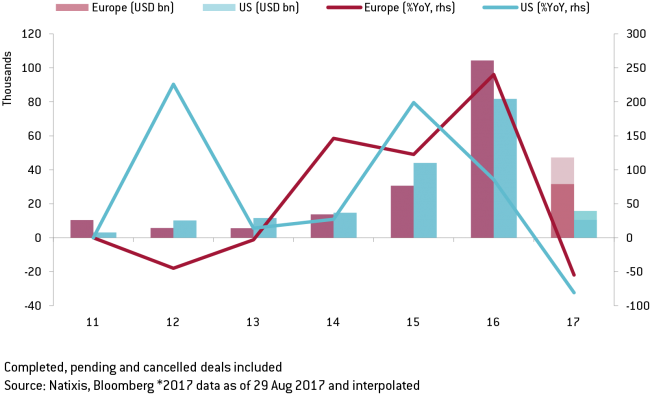

There are many reasons for the rising chorus of voices asking to protect European companies from foreign buyers. But China comes to mind first. Chinese companies have been acquiring foreign targets at an astounding pace, with over 30 billion USD in confirmed deals in 2016 and close to USD 100 billion if we were to add all deals which have been announced and not completed. Beyond the high numbers, one should note that both the announced and the completed Chinese acquisitions of European targets were larger than those of US targets (See Chart 1).

The sharp slowdown in mergers and acquisitions (M&A) in 2017 is actually not only for European targets but for China’s M&A globally (with a 20% reduction in the first half of 2017)[3]. In the absence of a global slowdown or tightening of financial conditions, such a sharp slowdown in Chinese M&A can only be explained by the recent change of direction of the Chinese government as regards foreign acquisitions, or at least “too exuberant” in less economically important sectors.

Chart 1 - Cross Border M&A Deals by Chinese Corporates

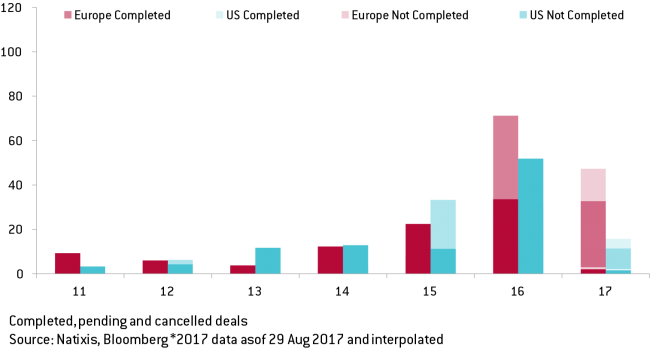

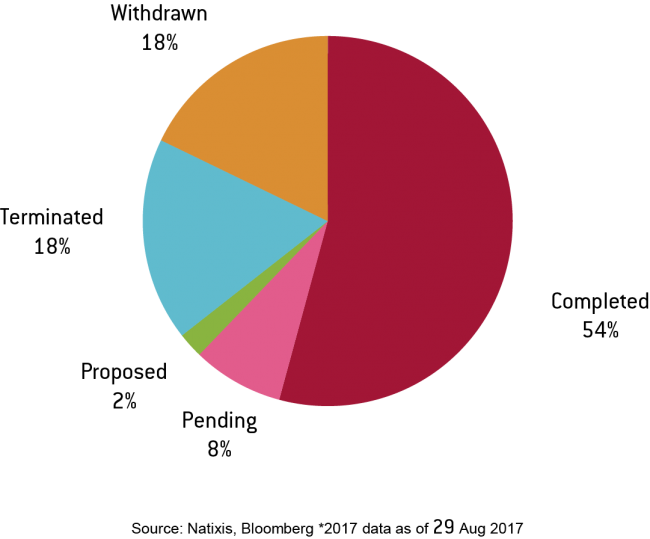

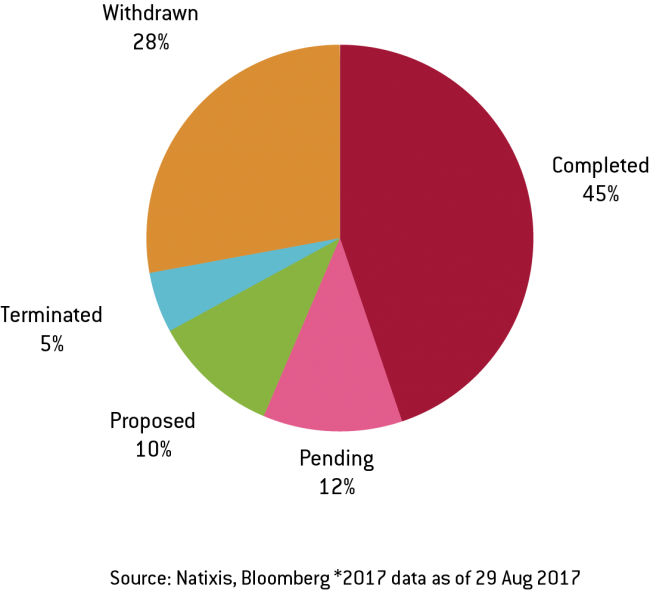

However, the headline figures hide a more interesting story. Fewer Chinese takeovers succeed in Europe than in the US. When analysing the M&A data more carefully, it appears that a smaller percentage of deals has been completed successfully in Europe as compared to the US during the last few years (Chart 2). This evidence runs counter to the presumption that an investment protection agency, like CFIUS, would reduce the number of deals completed. In reality, there are many other reasons why potential merger and acquisitions do not come through, the most obvious one being the lack of agreement on the terms between the two parties as well as the difficulties that the buyer may find to finance the operation. In fact, when one looks at US M&A operations in Europe, the percentage of deals that are completed is nearly as low as those of Chinese corporates trying to acquire targets in Europe (Chart 3 a,b c). In other words, it seems difficult to argue that Chinese investors are being pushed out of Europe, at least not more than US investors.

Chart 2 - Cross Border M&A Deals by Chinese Corporates by Deal Status (USD bn)

Chart 3a - Cross Border M&A Deals by Chinese Corporates by Deal Status (2011 - 2017, Europe)

Chart 3b - Cross Border M&A Deals by Chinese Corporates by Deal Status (2011 - 2017, US)

Chart 3c - Cross Border M&A Deals by US Corporates into Europe by Deal Status (2011 - 2017)

While the aggregate numbers do not show a clear protectionist trend in Europe yet, the reality is that warning signals are rising. There are a number of reasons for this. The first, and probably most important, is related to China’s economic model and, more importantly, company ownership structure. Still today, 64% of China’s listed corporates are state-owned, which raises eyebrows in European circles regarding potential national security threats. A second one, also important, is Europe’s fear of losing its comparative advantage as China moves up the ladder, which can be facilitated through the technological transfers embedded in China’s acquisition of European high-tech companies.

While understandable, such arguments need to come to terms with standard economic theory by which openness to foreign direct investment (FDI) should bring net benefits to a country. As for international trade, openness to foreign investment promotes competition and, thus, benefits consumers. Full openness to foreign investors should, thus, be the first-best approach. But this is with one very important assumption, namely that all countries follow the same reasoning: there is no free rider, or at least not a systemically important one.

China, the second largest economy in the world and second largest foreign direct investor in 2016, is the fourth most restrictive country for FDI in a sample of sixty-three major countries, after the Philippines, Saudi Arabia and Myanmar.[4]

With this background, and given the size of China’s domestic market and the increasingly globalised business of corporations, it seems farfetched to solve Europe’s challenges with Chinese investment with a new European agency in charge of investment protection. Such an agency could potentially stop some of the most problematic deals, especially if related to European-level security threats. But it would not solve a much wider issue for European interests, namely the threat of unfair competition - not only in Europe but actually globally.

Such unfair competition could stem from Chinese corporates preferential – sometimes even oligopolistic – access to the world’s largest – but also very protected – market in many sectors, namely that of China.[5] In fact, the combination of such a protected market with the very large share of state ownership complicates matters even further: European concerns on national security issues cannot always been disentangled from competition issues.

In that regard, pushing for more market access in China seems like the best way for European companies to protect themselves and, clearly, also a more optimal solution globally. There are two ways forward to ensure this first-best solution (equally free access by foreign investors in China and Europe). The first is multilateral and the second is bilateral.

The multilateral route is extremely difficult, if not impossible with the current international financial architecture. Multilateral processes for investment liberalisation are less institutionalised than for trade and, even there, there is no room for optimism in the current geopolitical juncture.

The latter option, the bilateral route, is currently being pursued by the Chinese government and EU Commission, which have been negotiating a bilateral investment agreement since late 2013. Unfortunately, the prospects for China agreeing to open its market to foreign investors on an equal footing, in exchange for keeping its ability to purchase companies is Europe, are quite dim. China’s access to M&A deals is relatively ample (USD 30 billion in completed acquisitions in 2016 says it all) so the only threat is that action is taken to reduce it. The reality is that it will take time for the EU to come up with a formalised vetting system as member states clearly have different opinions in this issue. It is much more likely that member states come up with new restrictions at the national level, further harming the European single market.

Moving to a second-best world – in which granting free access to Chinese investors does not correspond with more market access for European companies in China – Europe may prefer a more realistic and quicker solution to deal with any potential threats stemming from Chinese purchases of European corporations. The most obvious one is the application of Europe’s competition rules. More specifically, Chinese companies operating in Europe – or exploring new acquisitions in Europe – need to comply with European competition rules, which include the avoidance of a dominant position negatively affecting the functioning of the European Single Market.

The Glencor-Lonhor case in 1999 shows that EU Commission’s powers can go as far as refusing a merger of two foreign companies already approved by the local regulator if it creates a dominant position globally, affecting the good functioning of the European single market. This case is increasingly relevant for China, which has embarked on a process of mergers to rationalise large SOEs, creating national champions to compete globally. The most recent Google case, relating to its abuse of dominance in search, also constitutes a good warning signal for Chinese tech companies with global/European ambitions of.

More generally, EU competition policy could become a convenient substitute for a European-level investment protection policy in the same way as EU competition policy has long been known for being used for trade policy purposes (especially for antidumping).[6] Beyond competition policy, Europe can make use of its very high environmental and labour protection standards, which every company operating in Europe should comply with. The fundamental principle is that the best way to keep an open investment environment is to protect Europe’s single market with its existing rules and regulations – which not only European companies but also foreign ones need to abide to.

In sum, beyond the wishful thinking of a first-best world, full application of European competition policy and other rules and regulations to protect the European single market seems to be quickest and most efficient way to go to confront potential issues with Chinese investment.

[1] According to the European Parliamentary Research Service, the following countries have national legislation in place: Austria, Denmark, Finland, France, Germany, Italy, Lithuania, Netherlands, Poland, Portugal, Romania, Spain and the United Kingdom.

[2] Röller and Véron (2008) already proposed an EU mechanism to vet foreign investments, but with a different balance between EU and national interests than proposed here.

[3] M&A 2017 Mid-Year Review and Outlook Press Briefing, PWC

[4] OECD FDI regulatory restrictiveness index, http://www.oecd.org/investment/fdiindex.htm, 27 March 2017.

[5] The way in which Chinese companies may exercise such unfair completion is well documented in Garcia-Herrero and Xu’s Policy Bruegel Policy Note: “ How to Handle State-Owned Enterprises in EU-China Investment Talks”, June 2017

[6] See Nicolaïdis and Veron 1997 *Competition Policy and Trade in the European Union”, in Richardson and Graham, Global Competition Policy, Peterson Institute for International Economics

About the authors

Related content

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

China’s ‘new productive forces’ risk overcapacity bubble

India's economy can overtake China's if it can stay on track