Macroprudential policy: The Maginot line of financial stability

The ability of macroprudential policies to assure financial stability and thus leave central banks free to assign the interest rate tool exclusively t

An open question in central banking circles is whether interest rates should be used as a means to pursue not only price stability but financial stability too. Both the ECB President Mario Draghi and former Fed Chair Janet Yellen clearly showed a clear reluctance to follow this course of action.

Draghi, at his press conference of December 14, said: “We certainly closely monitor the financial stability risks that may emerge from a situation where we had very, very low interest rates for a long period of time, abundant liquidity for a long period of time. So the ground is fertile for these risks. At the same time, we are not seeing systemically important financial stability risks. … We assess whether the markets are closer or not to develop a financial stability situation. … Then we ask ourselves, what is the right answer to this problem? The right answer is to have in place macroprudential instruments that are effective, strong and well-targeted to cope with these risks. Certainly it's not to change monetary policy because of a financial stability risk in a certain part or in a certain market of the eurozone.”

Yellen[1] said something similar in a lecture at the International Monetary Fund, back in July 2014: “It seems clear that monetary policymakers have perceived significant hurdles to using sizable adjustments in monetary policy to contain financial stability risks. … [a] balanced assessment, in my view, would be that increased focus on financial stability risks is appropriate in monetary policy discussions, but the potential cost, in terms of diminished macroeconomic performance, is likely to be too great to give financial stability risks a central role in monetary policy decisions, at least most of the time.

If monetary policy is not to play a central role in addressing financial stability issues, this task must rely on macroprudential policies.

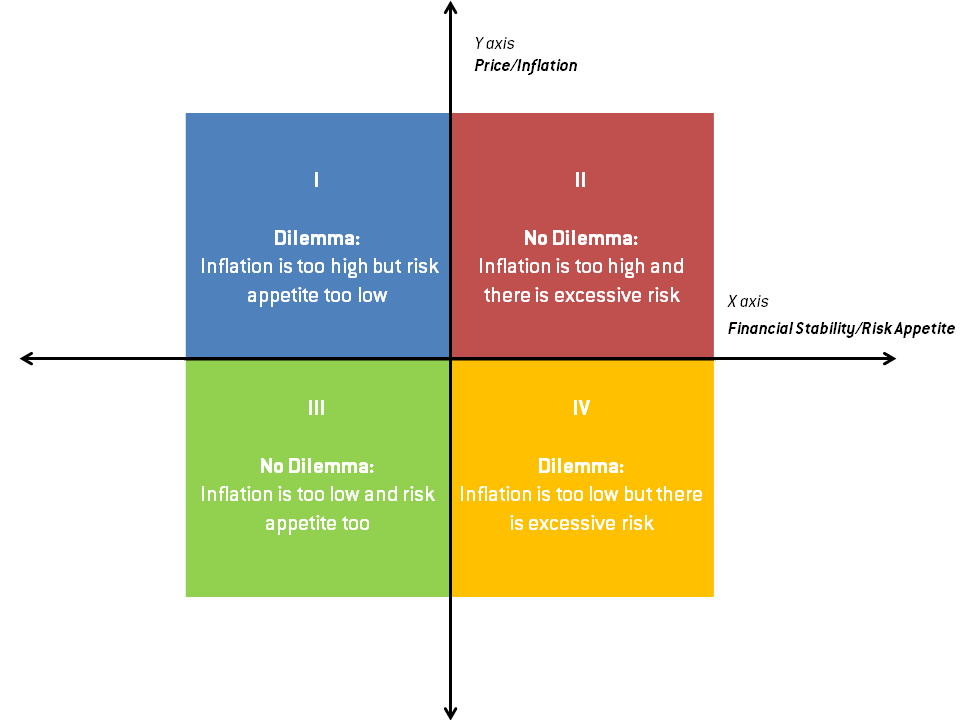

Draghi’s and Yellen’s answers are subtle enough to recognise that in some unlikely cases interest rates could be used to confront a generalised and intense financial stability risk. But they exclude that there exists a pressing, systematic dilemma between price and financial stability. This possible dilemma is represented in Figure 1.

Figure 1. Diagram of central bank dilemma between price/inflation and financial stability/risk appetite.

Source: Author´s representation

This diagram adapts an approach used to illustrate possible dilemmas between fighting inflation and unemployment during the era of stagflation in the 1970s, when central banks were torn between the desire to lower the interest rate to support economic activity and the need to raise it to fight inflation.

Quadrants II and IV denote no-dilemmas. For example in quadrant II inflation and risk appetite are too high, and an increase of the interest rate is required. In quadrant IV the opposite situation prevails. In quadrant I there is, instead, a dilemma because inflation is too high, but there is too low risk appetite and therefore it is not obvious whether to increase or decrease the interest rate.

Symmetrically, in quadrant III price and financial stability would require opposite moves of the interest rate because, in this case, inflation is too low – but there are risks to financial stability coming from excessive risk appetite[2]. Thus, according to White[3] (2009), in quadrant III the dilemma takes the specific “clean versus lean” form. Should monetary policy be content to keep inflation in check, and just “clean” the consequences of the crisis once the mania phase is followed by the panic and crash phase? Or should monetary policy be tighter in the mania phase (when there are financial stability risks) than the minimum required to keep prices stable; should it, in fact, “lean against the wind” of excessive optimism, thus surpassing the prescriptions of inflation targeting? According to this latter interpretation, the central bank should, in the middle of market euphoria, keep a more guarded attitude and transmit sobriety to the market, tightening monetary conditions.

Of course there would be no risk of dilemmas if a new class of instruments, namely macro-prudential tools, could be assigned to financial stability – and if the instruments were sufficiently effective – leaving the interest rate exclusively assigned to price stability. This seems to be the position of Draghi and Yellen: in most circumstances, when financial stability risk would emerge, macroprudential tools should be used to preserve financial stability, by acting on some parameters of the financial market. For instance, tools might include limiting the maximum share of the value of a house that can be financed by a mortgage (the so-called Loan-To-Value Ratio), or increasing the equity banks have to keep against a given balance-sheet size (the so-called Dynamic Capital Charges).

The apparent position of Draghi and Yellen is one of several possible views on the effectiveness of macroprudential tools – as well as the relative advantages or disadvantages of assigning interest rates exclusively to price stability, and macroprudential tools to financial stability. Views are indeed quite diverse on this issue. On one hand, the use of the interest rate also for financial stability purposes has the advantage that it “gets in all of the cracks”[4] (Stein 2013), meaning that it covers both banks and non-bank intermediaries. On the other hand, assigning interest rates to price stability and macroprudential tools to financial stability would have the advantage of potentially freeing the central bank from dilemmas.

The issue is further complicated because, as argued by Brunnermeier and Sannikov[5] (2014), the effects of the two classes of tools cannot be clearly separated. For instance, macroprudential measures aiming at maintaining financial stability would inevitably have an effect analogous to a tightening of monetary policy. The neat, if problematic, dilemma approach presented in Figure 1 is in this perspective simplistic, as there is no clear separation possible between macroprudential and monetary policies.

A little recall of basic economic concepts can help better focus on the issue.

Tinbergen[6] (1952) showed that, in a deterministic system, one needs as many tools as there are objectives in order to avoid dilemmas. In a stochastic system, by contrast – as shown by Brainard[7] (1967) – the more tools there are relative to the number of objectives, the better. The issue then is whether macroprudential tools are an effective additional tool to pursue financial stability, separately from price stability.

The problem is that both the interest rate and the macroprudential tool influence both price stability and financial stability. In fact, if each of the two tools only affected one objective, there would be two separate objectives and no problems in pursuing them: each with the assigned separate tool, and Tinbergen – even if not quite Brainard – would be happy. Draghi and Yellen seem to assume that this condition prevails, except for exceptional cases, and thus the central bank will not normally be confronted by dilemma situations.

My reading of the evidence is that this is more of a hope than an uncontroversial conclusion. Substantial work has been dedicated to developing macro-prudential tools from a theoretical and an empirical point of view; nonetheless, the work falls far short of any well-defined set of measures, whose application would be uncontroversial and might lead to reasonably certain results.

This is somewhat surprising, given that the concept of macroprudential policy was introduced in the late 1970s,[8] and therefore should have had ample time to mature into trustable instruments. Two explanations can be given for this extra-long incubation period: either macroprudential policy is extremely complicated, requiring decades to be developed; or its development was delayed by strong bureaucratic inertia, particularly in central banks, which could only be surpassed under the pressure of the crisis. Both explanations are probably relevant.

Let me give some background to the view that we cannot trust the ability of macroprudential measures to assure financial stability.

The papers analysing macro-prudential tools and trying to measure their effectiveness (see for instance: Akinci and Olmstead-Rumsey, 2015; Lim et al., 2011; Kuttner and Shim, 2013; Cerutti et al., 2015; Dell’Ariccia et al.[9], 2012) generally start with a complex definition of what these tools are, often providing different – even if largely overlapping – definitions. The difficulty is not surprising, considering that macroprudential tools are not intrinsically different from micro-prudential ones; the two even overlap to some extent with what, back in the 1970s and 1980s, were disparagingly called direct measures – such as limits on bank credit[10].

The common end result of such definitions is a “macroprudential index”, resulting from the summation of different measures prevailing at a certain point of time in a given country. This approach cannot distinguish the intensity of the different measures, nor even whether they are actually binding. To better comprehend the inevitable limitations of this kind of exercise one may compare the “macroprudential stance” that these indexes attempt to gauge, against the simplicity of the monetary policy stance as measured by the rate of interest.

The evidence about the effectiveness of macroprudential measures is gradually accumulating. The results achieved so far can, in my view, be summarised as follows:

- Macroprudential measures influence the rate of growth of bank credit

- The effect is more significant on bank lending connected to house purchases

- The evidence about an effect on house prices is less conclusive

- The recourse to macroprudential measures has been much more frequent in emerging than in advanced economies, and only after the beginning of the Great Recession did the usage of such measures increase in advanced economies

- The effect of macroprudential measures is asymmetric, being stronger in booms than in busts

- Macroprudential measures, like direct measures in the 1970s, are liable to elusion and circumvention. In particular there is evidence of a shift of intermediation from the banking sector, the sector most impacted by these measures, towards the non-bank sector and towards foreign intermediation

- Finally, macroprudential tools mostly tend to be used in association with other tools (monetary and fiscal); moreover their effectiveness is increased by this joint use, thus they appear more as complements than as substitutes for other measures.

An additional problem with macroprudential measures is that their institutional basis does not look solid. Both in the euro area and in the United States the institutional set up of macroprudential policies does not yet appear to have reached a fully settled situation that would consistently lead to effective policies.

In the euro area, macroprudential policy is shared between national authorities on one side, and the European Systemic Risk Board (ESRB) and the ECB on the other side. National authorities have the most important operational responsibilities, because they can impose as well as lift macroprudential measures. The ECB only has an asymmetric power of “topping up” national measures, meaning that it can add to, but not subtract from, national measures. Against the reality of national authorities imposing very different macroprudential measures in their jurisdictions, the topping-up power of the ECB is difficult to use. The ESRB, on its side, only has the power to issue warnings and recommend macroprudential measures. However, the General Board of the ESRB – including the national authorities that would be the main subjects of its recommendations –must agree with these. This approach de facto limits the effectiveness of this tool, because decisions have to be taken on a qualified majority basis when consensus cannot be reached. As a result, the effectiveness of the ESRB – created in 2010 on the basis of a recommendation of the 2009 De Larosière report, and chaired by the ECB President – is far from having been clearly established. Overall, while the framework in the euro area should be able to deal with idiosyncratic, national financial stability risks, it is unclear how an aggregate macroprudential policy for the euro area could be achieved.

In the United States the regulatory setup is complex and liable to lead to some confusion. In addition, United States regulatory reform is overwhelmingly focused on dealing with the too-big-to-fail problem, thus on Systemically Important Financial Institutions (SIFIs), and less on other potential sources of financial instability. A summary description of the American situation is that the Fed has, in principle, reasonably comprehensive macroprudential tools for a minority of the American financial system, but fewer tools (and some potential gaps) for the rest. Indeed the Dodd-Frank reform gave a responsibility of overall oversight to the Fed, including its power – in principle – to override other regulators in the use of microprudential tools for macroprudential purposes.

The Fed has, in particular, a number of potentially macroprudential tools to use with banks and bank holding companies (conglomerates), such as setting minimum credit standards for consumer lending, mortgages etc. In addition, the Fed can apply countercyclical capital buffers to SIFIs, be they banks or non-banks, but not to non-SIFIs. The designation of a financial entity as SIFI is a responsibility of the Financial Stability Oversight Council (FSOC). In practice, however, the designation of non-banks as SIFIs has turned out to be very difficult. General Electric reacted to this designation by just disposing of its financial activities. When the insurance company Metlife was designated as a non-bank SIFI, it sued the federal government (and FSOC in particular), saying that the standards were illegal and it won – at least the first degree of judgment. AIG was, with some controversy, judged not to be a SIFI by the FSOC.

The FSOC, like the ESRB, has the ability to issue recommendations to regulators to apply macroprudential measures to the institutions under their supervision. As in the case of the ESRB, however, the practical ability to do this is, in a 14-member committee filled with individual supervisors who are protective of their own mandates, extremely difficult. In conclusion, the somewhat trenchant assessment of Fischer[11] (2015) about “the relative unavailability of macroprudential tools in the United States” looks justified.

As shown above, both in the United States and in the euro-area, formally, the central bank is assigned an important, even dominant, role in the setting of macroprudential policies. According to some observers this raises issues of legitimacy, since macroprudential tools are seen as unsuitable for non-elected central banks. Whatever view one has on this institutional issue is, however, irrelevant in answering the fundamental question of whether the risk of dilemmas for the central bank is eliminated in the new regulatory landscape. The answer to this question does not depend on whether macroprudential measures are decided by the central bank or by any other institution; the critical point is whether macroprudential measures can assure financial stability on their own, and thus avoid putting the central bank in a dilemma in the use of its monetary policy tools.

It is indeed likely that the new regulatory set-up, in particular the use of macroprudential tools, will reduce the frequency and/or the depth of financial instability episodes. One may even hope that the intense ongoing work to further develop macroprudential weaponry will reinforce its effectiveness to the point where it will be able to conclusively deal with financial instability risks.

Hope, however, is not enough; one should therefore agree with Borio[12] (2015): The experience so far indicates that it would be imprudent to rely exclusively on these [macroprudential] frameworks, or even prudential regulation and supervision more generally, when seeking to tame the financial booms and busts that have caused such huge economic costs. Financial cycles are simply too powerful. ……other policies, not least monetary and fiscal, should also play a role. (p. 6)

Somewhat analogously, the most recent assessment of the Maginot line is not that it was a waste of resources by the French state because it did not protect from a German invasion: in a way it fulfilled its objective of making an attack by German forces along the common border impossible. The real problem was not having properly prepared for the eventuality that Germans would not care about Belgian neutrality, and attack through that country instead. Similarly, the conclusion of this post is not that macroprudential measures are useless in the pursuit of financial stability, but rather that one cannot count on that instrument alone to achieve that objective. This leaves open, in my view, the risk of dilemmas for central banks in the use of the interest rate. Draghi and Yellen are probably right that there is no pressing financial instability risk at present, but its occurrence sometime in the future cannot be excluded. Central banks cannot just hope that dilemma situations will not arise, they must rather prepare for the risk of dilemmas.

This post is based on an excerpt of a book by Francesco Papadia and Tuomas Välimäki, Central Banking in Turbulent Times, to be published in March (in May in the US) by Oxford University Press.

[1] Janet L. Yellen, Monetary Policy and Financial Stability. 2014 Michel Camdessus Central Banking Lecture, International Monetary Fund, Washington, D.C. 2 July 2014. There is consistency in her statements on this issue as she had already said something similar in 2011: “The evolving – though by no means settled – consensus is that monetary policy is too blunt a tool to be routinely used to address cyclical risks to financial stability, and that more targeted micro- and macroprudential tools should be used to address these risks. I agree that targeted prudential policies should be the first line of defense against threats to financial stability. However, because their effectiveness in practice is not yet proven, I would not rule out the possibility that monetary policy could be used directly to support financial stability goals, at least on the margin. Janet L. Yellen: Pursuing financial stability at the Federal Reserve. Fourteenth Annual International Banking Conference, Federal Reserve Bank of Chicago, Chicago, Illinois, 11 November 2011.

[2] I. Agur and M. Demertzis argue, in “Will Macroprudential Policy Counteract Monetary Policy’s Effects on Financial Stability?” (IMF Working Paper WP/15/283, December 2015), that, in theory, the direction in which monetary policy pushes macroprudential regulation depends on the state of the financial cycle. Empirically, however, they recognize that the sign is negative, as is usually assumed.

[3] White, W. R. (2009). Should Monetary Policy ‘lean or clean’?. Working Paper No. 34, Globalization and Monetary Policy Institute, Federal Reserve Bank of Dallas. Weinberg, J. (2015). Federal Reserve Credit Programs During the Meltdown. [online] Available at: https://www.federalreservehistory.org/essays/fed_credit_programs#footnote3.

[4]The full quotation is “while monetary policy may not be quite the right tool for the job, it has one important advantage relative to supervision and regulation--namely that it gets in all of the cracks. To the extent that market rates exert an influence on risk appetite, or on the incentives to engage in maturity transformation, changes in rates may reach into corners of the market that supervision and regulation cannot.” (p. 17) Stein, J. C. (2013). Overheating in Credit Markets: Origins, Measurement, and Policy Responses. [Speech] at the Restoring Household Financial Stability after the Great Recession: Why Household Balance Sheets Matter research symposium sponsored by the Federal Reserve Bank of St. Louis, St. Louis, Missouri, February 7, 2013.

[5] Brunnermeier, M. K., and Sannikov, Y. (2014). A Macroeconomic Model with a Financial Sector. American Economic Review Vol. 104, No 2, pp. 379-421.

[6] Tinbergen, J. (1952). On the Theory of Economic Policy. Amsterdam: North-Holland Publishing Company.

[7] Brainard, W.C. (1967). Uncertainty and the Effectiveness of Policy. The American Economic Review. Vol. 57, No. 2, Papers and Proceedings of the Seventy-ninth Annual Meeting of the American Economic Association, pp. 411-425.

[8] Maes, I. (2010). Alexandre Lamfalussy and the origins of the BIS macro-prudential approach to financial stability. PSL Quarterly Review, Vol. 63, No. 254, September 16, 2010, pp. 265-292.

[9] Akinci, O., and Olmstead-Rumsey, J. (2015). How Effective are Macroprudential Policies? An Empirical Investigation. Board of Governors of the Federal Reserve System, International Finance Discussion Papers, No. 1136. Kuttner, K. N. and Shim, I. (2013). Can non-interest rate policies stabilise housing markets? Evidence from a panel of 57 economies. BIS Working Papers No 433 Monetary and Economic Department. Cerutti, E., Claessens, S. and Laeven, L. (2015). The Use and Effectiveness of Macroprudential Policies: New Evidence. IMF Working Paper Research Department, March 2015. Dell’Ariccia, G., Igan, D., Laeven, L. and Tong, H. with Bakker, B. and Vandenbussche, J. (2012). Policies for Macrofinancial Stability: How to Deal with Credit Booms. Washington DC: International Monetary Fund.

[10] An example in Italy were the “Vincolo di Portafoglio” and the “Massimale sul credito”. In the UK an analogous measure was called “The Corset”.

[11] Fischer, S. (2015). Macroprudential Policy in the U.S. Economy. Speech at the "Macroprudential Monetary Policy," 59th Economic Conference of the Federal Reserve Bank of Boston, Boston, Massachusetts.

[12] Borio, C. (2015). Macroprudential frameworks: (too) great expectations? Contribution to the 25th anniversary edition of Central Banking Journal. BIS speeches.

About the authors

Related content

The European Central Bank’s timid operational framework update

The European Central Bank announced limited changes to its operational framework – which is probably right given current uncertainty

Don’t look only to Brussels to increase the supply of safe assets in the European Union

A sufficient supply of safe assets denominated in euros is critical if the European Union is to achieve a full banking and capital markets union.

Central banks: uncertainty is the problem, not managing the trilemma

Regaining price stability is difficult but doable; the bigger problem facing central banks is economic uncertainty.

The European Central Bank’s latest move tells a clear story

The European Central Bank is right not to over-react to recent banking problems.