Understanding (the lack of) German public investment

An array of data suggests that there is a general lack of investment by all branches of the German government, despite running budget surpluses for se

The German capital stock has grown very little compared to peer European countries (see Figure 1). This development is mostly one of the private sector and underinvestment in the corporate sector. However, the lack of public-sector investment has also contributed.

The aim of this blog post is to zoom in and document the weak public investment in Germany. A decreasing quality of public infrastructure – such as education and digital services, but also roads – will obviously have negative implications for private economic activity and could in turn reduce corporate investment further. It is therefore crucial to understand the public investment story in Germany.

Public (net) fixed capital formation

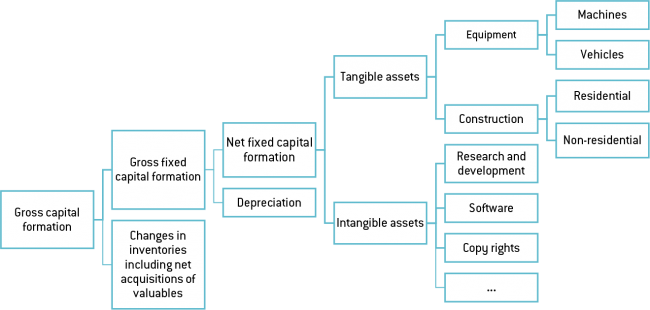

In order to analyse public investment, we rely on “public fixed capital formation”, which comprises public expenditures going into assets (tangible and intangible). It includes all kinds of construction (such as schools and highways), investments into equipment (such as machines or cars) as well as intellectual property. The notation “fixed” excludes changes in inventories. Net-figures are a good measure of “additional” investment activity, as capital does depreciate. And while it is true that the exact time profile of depreciations may differ from that of official national accounting, long-term trends should be unaffected by this. To be on the safe side, we also consider gross figures to get a complete picture.

Figure 2 provides a graphical overview about the definitions of capital formation in an economy.

Figure 2: Schematic diagram of gross capital formation

Source: Based on Destatis (2018a), own illustration.

The comparison of public net fixed capital formation between European countries confirms the weak growth of the entire German capital stock in recent years (as seen in Figure 1). Looking at public net fixed capital formation in relation to the GDP (by which we account for growth of the economy and changing prices), Germany’s weak development is hard to overlook. Figure 3 (right side) shows the average growth rate of public fixed capital formation (as a percentage of GDP) in five-year periods since 1993. It is striking that Germany exhibits by far the lowest net growth rates in four out of the five periods. In the last five years, only Italy and Spain – countries that have suffered from the euro crisis – are at or below German levels.

Especially since the 2000s, Germany has exhibited very low and even negative public fixed net capital formation ratios – below most other European countries. Germany has changed little, yet other European countries have stopped investing in the same pace, thereby lowering their ratios in the direction of the low German levels. That trend can also be found when looking at gross figures (left side of Figure 3). Germany’s public investment ratio declined in the 1990s and early 2000s and stabilised afterwards, while other countries exhibited much stronger public investment. In the last five years, gross public investment in France and the UK has been stronger than in Germany, while Spain and Italy have shown levels similar to Germany’s.

Public investment in Germany

Zooming into Germany, we see that fixed capital formation has been falling for 20 years as a percentage of GDP. The fall can be detected in gross and net numbers and is true for the public and the private sector. (Figure 4)

Starting with private gross fixed capital formation of around 22% and private net fixed capital formation of 8.5% in 1991, Germany had rates of 18.1% and 2.8% respectively in 2017. For the public sector, public gross fixed capital formation fell from 3.2% to 2.2%, while public net fixed capital formation fell from 0.8% to 0.0% (with periods of negative rates) in the same period. Arguing that the fall of Germany’s public investment is only due to looking at gross numbers seems not to be valid, as both gross and net numbers have fallen similarly.

What is behind the fall of public investment in Germany?

Looking at gross numbers, the development of Germany’s public investment seems impressive at first sight (Figure 5). Public gross fixed capital formation as a percentage of GDP has risen from 1.9% in 2005 to 2.2% in 2017; however, that is still far below the early-1990s levels of over 3.0% of GDP (Figure 5, bars, left axis). Especially since 2005, absolute gross numbers have risen considerably from around €43 billion to over €70 billion per year in 2017. However, accounting for inflation as well as the growth of the German economy, the situation does not look as favourable any more (Figure 5, dotted line, right axis).

Looking only at net numbers, the picture does not turn brighter (Figure 6). Net fixed capital formation of the German general government – comprising central, state, and local governments – has been strongly negative since 2007 (minus-€6.7 billion) and still negative since 1997 (minus-€2.2 billion). That means that the value of the capital stock of the entire German government has decreased by almost €7 billion, while the entire German economy grew by almost 30% in the same period. Currently, state (Länder) and federal government spending together only just make up for the falling net capital stock of local governments. The infrastructure of local governments is currently falling in value and these governments live off past investments.

Germany’s particular financial constitution is playing an important role here. On the revenue side, most revenues are generated by central government taxes and then redistributed to the state and local governments with a complicated procedure. Local governments have some taxes they can determine on an individual basis, but the overall room for manoeuvre remains limited.

On the spending side, all three levels of German governments play different roles. Looking at the investment part, the central government can invest in military as well as certain infrastructure projects – such as federal highways, as well as train tracks and railway stations via the state-owned train company. However, the German constitution does not allow interference from the central government in the realm of state and local governments – and therefore certain investments, such as investments in all education-related fields as well as state and local streets. In Germany, the states have the sovereignty over higher education, and therefore decide on investment in universities. On the level of schools, local governments rule on investments in buildings and equipment. In social questions, it is also the responsibility of local governments to invest in social housing.

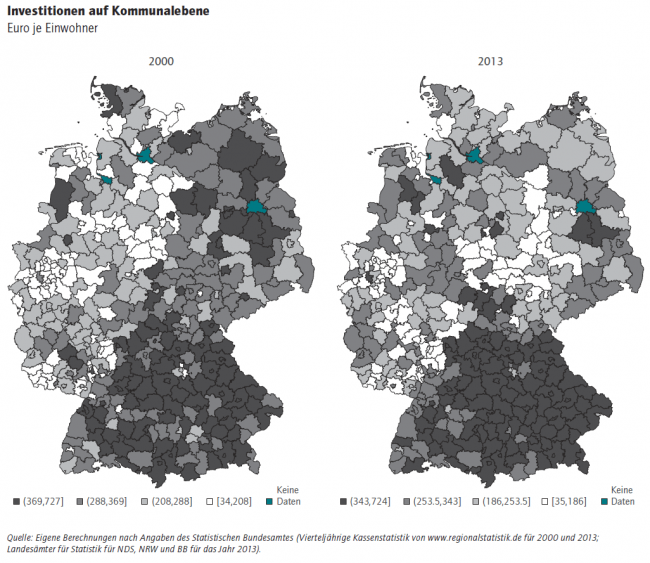

Thus, the standards of German schools, universities, and public facilities can differ substantially between states and cities. A recent study (Arnold et al. 2015) reveals enormous geographic differences in public capital formation. As shown in Figure 7, eastern German local governments spent relatively high amounts in 2000, together with local governments of southern Germany. However, 15 years later, public investments levelled out in most parts of Germany – except for Bavaria. That map in Figure 7 hints at the problem that local public income is unequally distributed; primarily the rich southern communes can invest, while poorer communes – such as in North-Rhine Westphalia – go without the financial means for long-term investment that would improve their economic situation.

Figure 7: Public gross fixed capital formation (by local governments)

Source: Arnold et al. (2015)

As a consequence, a recent initiative of the central government plans to change the German constitution with the aim to facilitate additional support from the central government to the local governments.

Disaggregated into different expenditures

As shown in the section above, net public fixed capital formation varies substantially between different governmental entities. While the public capital stock of federal and state governments has built up, that of the local governments is shrinking currently. Overall, the general government sector did not have significant public net fixed capital formation in the last 20 years. This underinvestment is most apparent in the communes of western Germany, in road and school buildings and in network infrastructure such as broadband cable for faster internet access.

Looking at the share of households that are subscribed to fibre-optic communications – which is the latest, fastest, and most forward-looking technology – Germany has most recently ranked fifth among European countries. Latvia, Sweden and Lithuania are leading the rankings. The latest “State of the Internet / Connectivity Report” does not give a rosier picture of Germany’s internet infrastructure. Compared to other European countries, Germany is only in the midfield when it comes to “average connection speed” and the lower mid-range in terms of “average peak connection speed” (average of the highest connection speed).

We have to acknowledge here that simply increasing spending in Germany’s digital infrastructure might not be sufficient to increase the quality. Other countries have shown that private actors can also provide high-quality digital infrastructure. Thus, we reference here also the importance of Germany’s market structure that seems to prevent providing a sufficient level of public good, such as a digital infrastructure.

Regarding the road and rail infrastructure, a study by Bardt et al (2014) highlights the importance of infrastructure for the functioning of the economy. The study shows the results of a survey among companies, in which more than half of the participants indicated that their business was affected in a negative way due to problems in the infrastructure. Another study by Germany’s pro-rail transport alliance emphasises the fact that Germany’s per-capita investment in rail infrastructure is below that of countries such as Switzerland, Austria, Sweden, Netherlands, and even the UK.

As can be seen in Figure 7, public spending (as a percentage of GDP) has been decreasing in crucial sectors that are at the centre of political debate. Education (investments in school buildings etc., not salaries for teachers), housing and defence show declining public investment numbers.

Looking at public gross fixed capital formation[1] as a percentage of GDP, investment spending into the German military forces (e.g. spending on infrastructure and equipment, not salaries) dropped from over 0.30% of GDP in 1991 to almost 0.15% in 2002, and has recently recovered to 0.25% of GDP in 2017.

Investment spending in education – mainly done by the state governments for universities, and local governments for schools – has been declining or, at best, stagnating for 20 years. In 1991, German communes invested 0.19% of GDP in the educational system. Over the years, the value fluctuated around 0.20% and declined to 0.16% in 2017. On the level of the state governments, public gross fixed capital formation in education fell dramatically from 0.23% in 1991 to 0.10% in 2017.

Like in many other European countries, German households’ spending on rents and property is increasing – especially in urban regions. German local governments (which are primarily responsible for investing into housing) have seen their investment ratio more than halved, from 0.19% in 1991 to 0.05% of GDP in 2017.

The changing nature of German public investment can also be found in the numbers. As shown in Figure 9, public net fixed capital formation in construction – residential and non-residential – has decreased considerably in recent years. Public residential construction has always been quite low, but has decreased to levels around and even below zero. For non-residential construction, public net fixed capital formation has even been below zero since 2003. The latter measurement is quite extreme, considering that this item includes crucial infrastructure such as roads, schools, and universities that are important in securing the long-run growth potential of an economy. While ignoring construction, German governments used up their investment spending on equipment as well as intellectual property. The latter item is somewhat illustrative of the growing importance of the digitalisation of the economy, expressed – for example – by investment in software.

Back to normal after the reunification?

Obviously, when comparing German investment figures from 1990s to the 2000s, one must consider the one-time effect of the reunification and the massive increase of both public and private investment spending in the new Bundesländer of the former East Germany state. As shown in Figure 10, we see a considerable increase of spending (in absolute and relative figures) in the new Länder after 1990 with a reduction after the mid-1990s and then very constant nominal spending in the 2000s.

The Bundesländer of the former West Germany experienced increases in public spending in the late 1990s, around 2006 and in the last three years. Still, the ratio of spending in investment to GDP decreased from 20.9% in 1991 to 16.9% in 2017, showing the structural weakness in the levels of both public and private investment.

Reviewing the international comparison and the historical perspective since 1990, it is fair to argue that Germany exhibits currently a very low level of gross fixed capital formation, in the private as well in the public sector. For 20 years, German governments have relied on past spending in investments and allowed the public capital stock to lose substantial value.

Status of public finances

The problem of low levels of public investments is not born of a lack of available funds. As shown in Figure 11, the German general government (central, state, and local governments) have all been running large surpluses for several years.

However, as briefly discussed before, aggregated data on surpluses does not provide any information on the regional distribution of financial means. Not only might too many surpluses be concentrated at the Länder-level when needed instead at local level, a few local governments might also be very affluent compared to others still running fiscal deficits.

Budgetary plans

The budget proposed recently by the new federal finance minister does not seem to constitute a significant change to the previous picture (Wolff 2018). Germany also does not seem willing or able to plan and put in place the infrastructure projects to meet the budget allocations.

The new German finance minister should allocate funds for upgrading the network infrastructure[2] in Germany. It has to be ensured that local governments are provided with sufficient financial support to keep up with their tasks. Here, the new government seems at least determined to improve the situation, but it could take some time before additional money flows to the communes in need.

We are aware that the entire question of German capital formation goes beyond the spending decisions of the government. Germany’s government has to ensure that the regulatory environment is set in a way that public and private investment is facilitated.

The numbers presented above suggest that there is a general lack of investment by all branches of the German government. Per-capita ratios of public net fixed capital formation have been falling for sectors such as education, construction, and military. However, there is evidence that the quality of the infrastructure of schools and, especially, universities influence educational outcomes. That Germany’s industry-heavy economy relies on a well-functioning transport grid, roads and tracks, is without question. And without a fast and reliable internet infrastructure, Germany will not be able to stay competitive in developing upcoming digital technologies.

[1] We use gross instead of net fixed capital formation due to the inevitability of net figures.

[2] Cost estimates range between €50-80 billion.

References:

Allianz pro Schiene (2017). EU-Ranking: Deutschland knausert beim Schienennetz. July 12, 2017. https://www.allianz-pro-schiene.de/presse/pressemitteilungen/eu-ranking-deutschland-knausert-beim-schienennetz/. Accessed 06/06/2018.

Arnold et al. (2015). Große regionale Disparitäten bei den kommunalen Investitionen. DIW Wochenbericht Nr. 43. 2015. https://www.diw.de/documents/publikationen/73/diw_01.c.517381.de/15-43.pdf.

Bardt et al. (2014). Die Infrastruktur in Deutschland. Forschungsberichte aus dem Institut der deutschen Wirtschaft Kön Nr.95. 2014. https://www.iwkoeln.de/fileadmin/user_upload/Studien/IW-Analysen/PDF/Bd._95_Infrastruktur.pdf.

European Commission (2018). Macro-economic database AMECO. Accessed 06/06/2028.

Destatis (2018a). Volkswirtschaftliche Gesamtrechnungen, Arbeitsunterlage Investitionen, 4. Vierteljahr 2017.

Destatis (2018b). Staat erzielt im Jahr 2017 Überschuss von fast 37 Milliarden Euro. Press release Nr.059 of February 02, 2018. https://www.destatis.de/DE/PresseService/Presse/Pressemitteilungen/2018/02/PD18_059_813.html. Accessed 06/06/2018.

Wolff (2018). Germany’s Government Still Has an Allergy to Investing. Bloomberg. May 14, 2018. https://www.bloomberg.com/view/articles/2018-05-14/germany-s-new-government-isn-t-on-a-spending-spree-after-all. Accessed 06/06/2018.

About the authors

Related content

The European defence industrial strategy: important, but raising many questions

The European defence industrial strategy helps to focus thinking but has significant flaws

EU savers need a single-market place to invest

Proposals to leverage the single market to boost retail investment could lead to a product citizens will trust

The impact on the European Union of Ukraine’s potential future accession

This report evaluates the impact on the EU of a possible EU accession of Ukraine, focusing on economic consequences and institutional developments.

Bringing the reform of European Union fiscal rules to a successful close

EU fiscal rules must not unnecessarily restrict green investment.