The ghost of Deauville

On 19 October 2010, Angela Merkel and Nicolas Sarkozy agreed that in future, sovereign bailouts from the European Stability Mechanism would require th

On 19 October 2010, Angela Merkel and Nicolas Sarkozy agreed that in future, sovereign bailouts from the European Stability Mechanism would require that losses be imposed on private creditors. This agreement was blamed for the increase in sovereign spreads in late 2010 and early 2011. This column discusses recent research on the market reaction to the surprise announcement at Deauville. With the exception of Greece, the rise in spreads was within the range of variability established in the previous 20 days.

The aversion to debt restructuring in the Eurozone has been remarkable, even though public debt ratios in several countries are well above the IMF-identified critical debt overhang threshold of 100% of GDP (IMF 2012). By early 2010, some recognised the urgency of restructuring Greek public debt (Calomiris 2010). But the official position between late 2009 and early 2011 deemed even Greek debt to be sustainable. Beyond the particularities of Greece, general principles were invoked. In the words of Cottarelli et al. (2010), restructuring of advanced countries’ public debt was “unnecessary and undesirable’. The premise was that the Eurozone economies were institutionally strong, and a quick resumption of growth would defang the debt crisis. Strengthening the case, the risks of financial contagion were considered serious.

Over successive financial crises, policymakers have become increasingly wary of financial contagion, and have therefore exercised greater restraint in imposing losses on private creditors (Barkbu et al. 2012). They have preferred ever-greater reliance on international official financing alongside more demanding fiscal adjustment by the crisis countries. This trend was taken to a new extreme in the Eurozone crisis, bolstered by the observation that the distressed countries were ‘advanced’.

The wisdom of such an approach was briefly questioned. By late 2010, assertions of debt sustainability were losing credibility even in official circles. Chancellor Angela Merkel of Germany and President Nicolas Sarkozy of France acknowledged reality by agreeing at their Deauville summit on 19 October 2010 to a forward-looking debt restructuring process. After 2013, they agreed, financial assistance to sovereigns from the European Stability Mechanism would require that losses be imposed on their private creditors.

The Deauville proposal was met with instant fury, not least from Eurozone finance ministers and officials assembled simultaneously in Luxembourg (Forelle et al. 2010). As the drumbeat of criticism continued, Deauville was identified as the universal cause of many ills. The IMF’s Staff Report for the Fourth Review of the Greece programme, published in early July 2011 – just days before the inevitable Greek debt restructuring process – could not resist pinning the blame even for Greek woes on Deauville. The criticisms took their toll. Although the Deauville proposal was subsequently adopted by the European Council, it was eventually watered down and effectively abandoned. The characterisation of Deauville as a Lehman-like moment for Europe has cast a pall over all discussion of sovereign debt restructuring, rare voices notwithstanding (Portes 2011, Buchheit et al. 2013).

The presumed evidence for a Deauville effect is the market pressure experienced by distressed sovereigns in late 2010 and early 2011. The risk premia they paid – the spread between the yield on their bonds and that on German sovereign bonds – increased rapidly. But does the indelible association between the Deauville decision and the rise in spreads hold up to closer scrutiny? To answer that question, we cannot rely on the general increase in spreads; we must shine the spotlight on the days surrounding 19 October 2010.

Assessing the Deauville effect

There was no mystery to the rise in spreads during this period. When Greece received official funds in its first ‘bailout’ in May 2010, its debt ratio was not reduced. And although the decision not to impose losses on private creditors kept them whole for the moment, they became subordinate to the now substantial repayments due to official creditors. For this reason, as Chamley and Pinto (2011) highlighted, the risk faced by private creditors increased and they demanded ever higher spreads. Since it was the expectation that Greek-style programmes would be extended to Ireland and Portugal, the risk premia paid by these other sovereigns also rose. Steinkamp and Westermann (2013) have since traced the increase in spreads during this phase to the expansion of senior official debt.

The question boils down to whether Deauville added to the run-up in spreads. To infer the market’s reaction, I use the changes in spreads on 10-year sovereign bonds following the Deauville announcement (Mody 2013). As in Ait Sahalia et al. (2012), I estimate the ‘abnormal cumulative change’ in bond spreads. The word ‘abnormal’ refers to the deviation from a counterfactual (the evolution of spreads if no policy change had occurred). Following Ait-Sahalia et al. (2012), I use the average daily change over the past 20 market days as the most probable continued change absent the policy intervention.

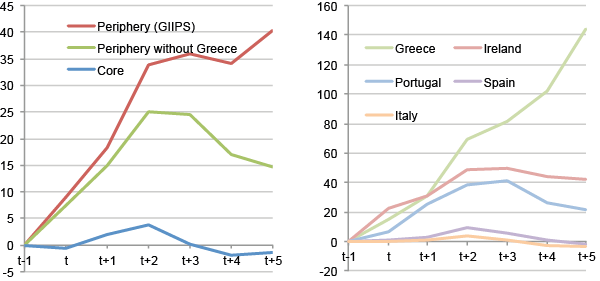

In Figure 1, the rise in spreads on 19 October, ‘t’, is attributed to the Deauville decision, since markets were aware of the decision before they closed that day. For the distressed periphery of the Eurozone, the cumulated abnormal rise by the end of the fifth day after Deauville was about 40 basis points (100 basis points equal one percentage point). Much of the rise was accounted for by Greece, where the increase was almost 150 basis points. For Ireland, the peak rise in spreads was 50 basis points; but, importantly, this peak was reached on the third day after the Deauville decision, after which the abnormal rise began to fade. Similarly, the peak rise for Portugal was 45 basis points on the third day after Deauville, after which the abnormality again receded. The abnormal movement in Spanish and Italian spreads was trivially small.

Not only was the rise in non-Greek spreads small, it was within the range of variability established in the previous 20 days. For example, the standard deviation of the four-day cumulative changes (corresponding to the announcement plus three subsequent days) for Portugal was 31 basis points. So, the Portuguese increase in spreads at 45 basis points was 1.5 standard deviations of the rise in spreads. Put another way, there was one four-day period in those past 20 days when the cumulative rise was above 45 basis points. Similarly, the average level of the Irish sovereign yield in the five days after Deauville was 6.44% compared with 6.61% in the five days ending on 30 September. Thus, markets had only recently perceived the same degree of risk on Irish and Portuguese bonds as in the days after Deauville.

Figure 1 Sovereign bond market reactions to the Deauville agreement, 19 October 2010

Cumulative Abnormal Change (basis points)

Thus, attributing the rise in risk spreads in October and November 2010 to Deauville is unwarranted. If Deauville were the causal factor, a more decisive rise in spreads around the announcement should have been evident. In particular, the fall in the Irish and Portuguese abnormal spreads on the fourth and fifth days after the announcement, and the absence of a noticeable change in Italian and Spanish spread dynamics, imply that Deauville created no obvious break with the past. These findings also point to the absence of contagion – another charge against Deauville. The relative rise in spreads on the first three days reflected exactly the differences in the perceived credit risks of the different countries – high for Greece, lower for Ireland and Portugal, and even lower for all others.

A concern with such analyses is that the announcement may have been anticipated, and so the rise in spreads may have occurred already. But as Forelle et al. (2010) describe, the Merkel–Sarkozy agreement was a surprise – it hit those present at the Luxembourg Eurogroup meeting “like a bomb”. Hence, the evidence, such as there is, points to Deauville being essentially a non-event. At best, pre-existing market perceptions were reinforced.

Some implications

Attributing the rise in spreads in late 2010 and early 2011 to Deauville requires invoking unspecified lead and lag mechanisms. If there was a villain, it was the preferred strategy of outsized official financing and fiscal adjustment. That strategy did not improve debt sustainability. But private creditors, now increasingly junior to official creditors, faced higher risk of disorderly and arbitrary restructuring.

Deauville sensibly recognised that debt will not always be repaid. In such cases, temporarily appeasing private creditors does not help; instead, lowering the costs of debt restructuring through orderly mechanisms is the right way forward. Deauville would have initiated a move away from reactive debt restructuring – resorting to it when left with no other choice – to a proactive approach. For this reason, it was a necessary first step to re-establishing a credible ‘no bailout’ regime, crucial to the architecture of the Eurozone (Mody 2013).

The decision to go back on Deauville was unfortunate. It was based on a superficial reading of the evidence – a reading that has remained a self-serving focal point for the critics of debt restructuring. Even if the market had reacted adversely to Deauville, the decision to change course would not have been the logical conclusion. A rise in spreads in that case would only have revealed a sizeable subsidy arising from the untenable expectation that private creditors will always be bailed out. Today, despite new proposals (Buchheit et al. 2013), the ambivalence towards debt restructuring and the risk treatment of sovereign debt continues, leading to policies that increase moral hazard and risks of future instability. Where debt is unsustainable, wishing it away is not wise policy.

This piece was published by VoxEU on January 7th, 2014.

References

Ait-Sahalia, Y, J Andritzky, A Jobst, S Nowak and N Tamirisa (2012), “Market Response to Policy Initiatives during the Global Financial Crisis”, Journal of International Economics 87, pp. 162–177.

Barkbu, B, B Eichengreen and A Mody (2012), “Financial Crises and the multilateral response: What the historical record shows”, Journal of International Economics 88(2), pp. 422–435.

Buchheit, L C, B Weder di Mauro, A Gelpern, M Gulati, U Panizza and J Zettelmeyer (2013), “Revisiting sovereign bankruptcy”, VoxEU.org, 12 November.

Calomiris, C (2010), “The Painful Arithmetic of Greek Debt Default”, American Enterprise Institute.

Chamley, C and B Pinto (2011), “Why Official Bailouts Tend Not to Work: An Example Motivated by Greece 2010”, The Economists’ Voice, 8.1, February.

Cottarelli, C, L Forni, J Gottschalk and P Mauro (2010), “Default in Today’s Advanced Economies: Unnecessary, Undesirable, and Unlikely”, Fiscal Affairs Department, International Monetary Fund, Washington DC.

Forelle, C, D Gauthier-Villars, B Blackstone and D Enrich (2010), “As Ireland Flails, Europe Lurches Across the Rubicon”, the Wall Street Journal, 27 December.

International Monetary Fund (2012), “The Good, the Bad, and the Ugly: 100 Years of Dealing with Public Debt Overhangs”, World Economic Outlook, October, Washington, DC.

Mody, A (2013), “Sovereign Debt and its Restructuring Framework in the euro Area”, Bruegel Working Paper 2013/05, Brussels, forthcoming in Oxford Economic Papers.

Portes, R (2011), “Restructure Ireland’s debt”, VoxEU.org, 26 April.

Steinkamp, S and F Westerman (2013), “The role of creditor seniority in Europe’s sovereign debt crisis”, Osnabrück University and CESifo.