Central and eastern Europe: uncertain prospects of economic convergence

This year countries of Central and Eastern Europe celebrate two important anniversaries: 25 years since the beginning of post-communist transition (19

This year countries of Central and Eastern Europe celebrate two important anniversaries: 25 years since the beginning of post-communist transition (1989) and 10 years since the first wave of EU Eastern Enlargement (2004). Such anniversaries provide a good occasion to look both back and ahead and summarize both successes and failures.

Do these anniversaries allow us to claim successes and look optimistically into the future? Yes and no. One does not need sophisticated analysis to understand how radically this region has changed during the last quarter of century – in terms of its political and economic systems, geopolitical arrangements, living and civilization standards, infrastructure, etc. However, one can also ask some difficult questions such as, for example, have all opportunities of economic and political progress been grasped? Was the entire 25/10-year period (depending on which anniversary we are talking about) successful? Perhaps we could claim bigger successes 5 or 7 years ago (before the global and European financial crisis started) than now? And what about the future? Is further economic progress automatically guaranteed?

A simple convergence analysis

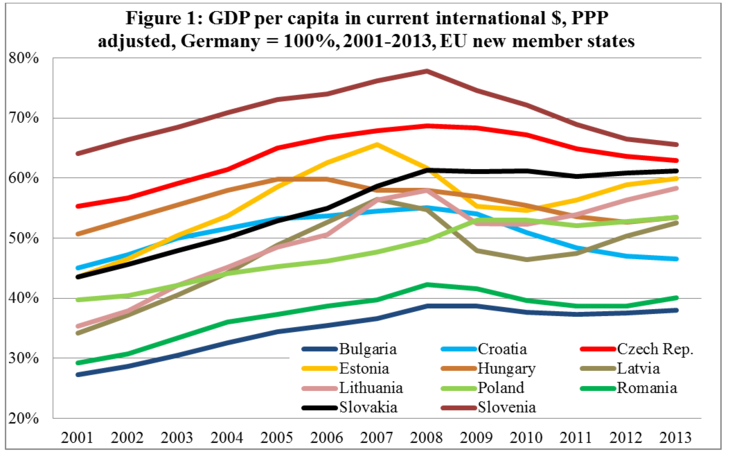

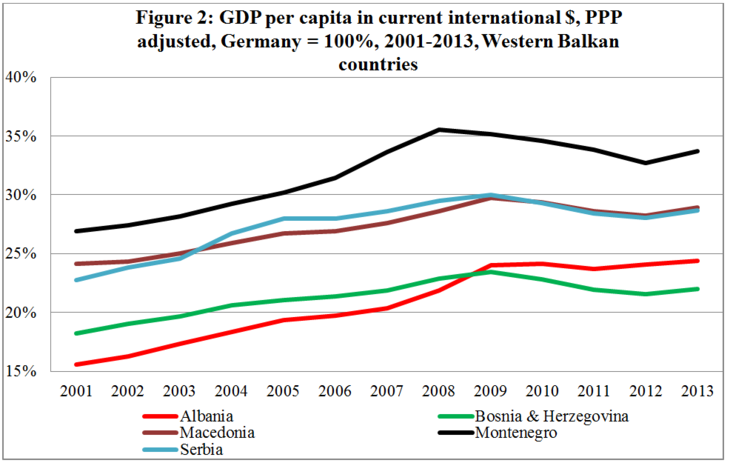

Economic convergence may be interpreted and measured in many ways. Here we use [1] a very simple approach – we compare GDP per capita in current international dollars, in PPP terms of each central and Eastern European (CEE) country with that of Germany based on the IMF World Economic Outlook October 2014 database statistics.

The choice of Germany as a benchmark is motivated by its role as the largest EU national economy and major economic and trade partner of most of CEE economies on the one hand, and its largely positive but rather modest rate of growth in 2000s and 2010s [2], on the other.

We analyse the period between 2001 and 2013, i.e. after the end of dramatic period of transition related restructuring and related prolonged output decline (in early and mid-1990s) and the series of emerging-market crises (in the second half of 1990s) which affected part of the region. Figures 1 and 2 present results of our analysis for two country subgroups, i.e., current EU members (including Croatia which joined the EU on July 1, 2013) and EU actual and potential candidates in the Western Balkans region (except Kosovo for which the respective data is not available).

Convergence followed by de-convergence

In both country groups we can clearly distinguish two sub-periods – until 2007/2008 with rapid catching up (convergence) and after 2008 with either de-convergence or no progress in further convergence.

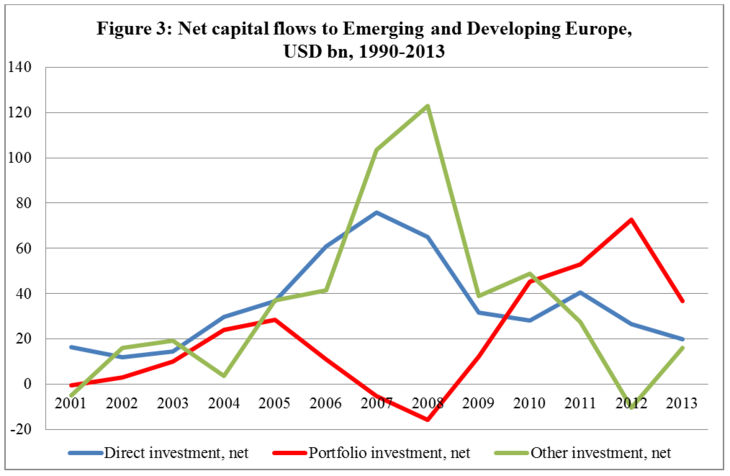

It is quite easy to name factors behind the rapid convergence experienced in the first sub-period: (1) post-transition growth recovery (effects of transition related reallocation of factors of production); (2) joining the Single European Market (or partial access in case of EU candidates); (3) global economic boom which resulted in large-scale capital inflows to the region (see Figure 3). The first two factors had a one-off character and the third one – short-term effect, which was largely reversed during the following crisis.

Note: According to IMF WEO geographical grouping Emerging and Developing Europe includes (as of October 2014) the following CEE countries: Albania, Bosnia and Herzegovina, Bulgaria, Croatia, Hungary, Kosovo, Lithuania, Macedonia, Montenegro, Poland, Romania, Serbia, and Turkey.

When the global financial crisis hit the region in 2008-2009 (in Baltic countries it started earlier, in 2007, and Hungary stopped converging in 2005) the convergence trajectory changed for worse everywhere. However, we can distinguish substantial differences across both country sub-groups.

The four EU new member states with the highest income per-capita level in early 2000 have recorded a steady decline in their relative GDP per capita levels after 2008

The four EU new member states with the highest income per-capita level in early 2000s, i.e., Slovenia, Czech Republic, Hungary and Croatia, have recorded a continuous decline in their relative GDP per capita levels, as compared to Germany after 2008. Three Baltic countries experienced an even sharper decline in 2008-2010 but then returned to rapid re-convergence (however, only Lithuania managed to exceed its pre-crisis convergence level yet). The somewhat similar growth pattern, i.e., first decline and then recovery can be observed in Western Balkan candidate countries (except Albania), Romania and Bulgaria although with smaller amplitudes of changes in their convergence trajectories (especially in the case of Bulgaria). Finally, Poland, Slovakia and Albania managed to continue their convergence vis a vis Germany after 2008 although at a very slow pace.

Future growth challenges

Looking ahead, one must ask what kind of challenges will be faced by CEE countries in their future development, and whether they will have chance to return to their pre-2007/2008 convergence trajectory (which many people in the region continue to believe). Clearly the pre-crisis growth bonanza based on large-scale capital inflow (which, in turn, was the consequence of underestimation of the region’s risk premia – see Luengnaruemitchai & Schadler, 2007) and the above mentioned one-off factors is unlikely to come back anytime soon. We live in a different world now.

Let us look briefly at long-term growth factors as determined by neo-classical growth theory. The demographic trends will be increasingly unfavourable, resulting in declining cohorts of working-age populations. Although this is a common European problem (including Germany, which serves as the benchmark in our analysis) and we compare GDP per capita figures, the Eastern part of the continent will experience sharper decline in this respect than their higher-income Western European neighbours (it is also necessary to take account of East-West labour migration which will continue until the current income gap diminishes substantially).

Looking ahead dramatic challenges will be faced with respect to investment

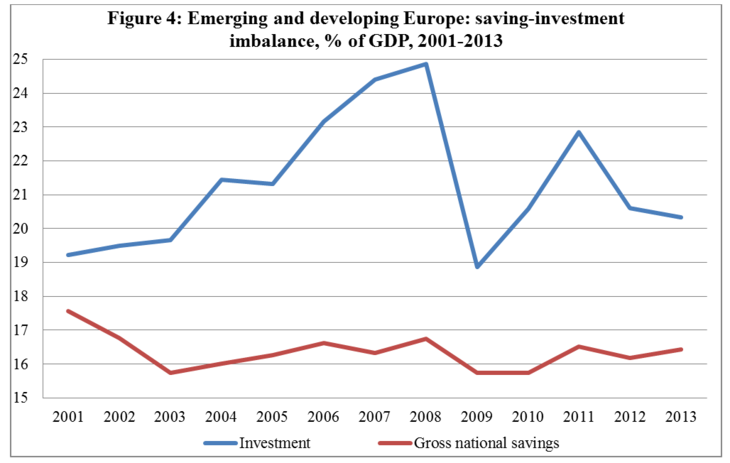

However, even more dramatic challenges will be faced with respect to investment. The short-term investment boom (between 2003 and 2007) was based on imported savings (capital inflow – see Figure 3) causing large current account imbalances (see Figure 4). When capital inflow stopped in 2008 the investment rate had to come down, in some countries (Baltics, Bulgaria, part of Western Balkans) substantially. Historical experience demonstrates that sustainable catching-up growth requires higher investment rates, at least 25% of GDP, and such a level was approached only once, in 2008 (see Figure4).

Low-saving trap and reform stagnation

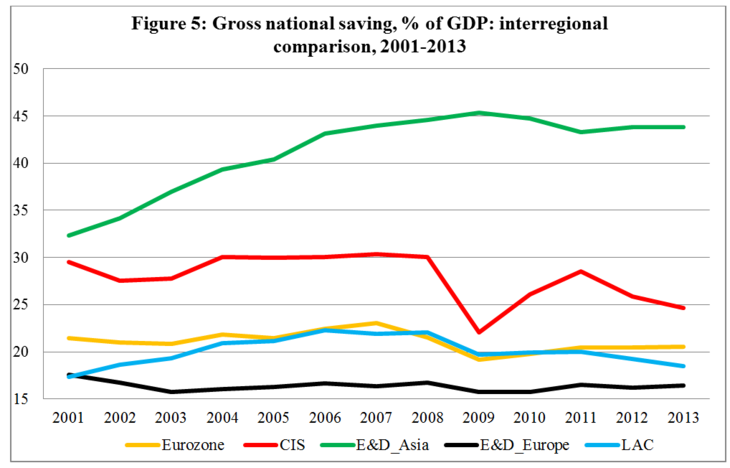

The bottom line is that the gross saving rate in CEE economies is very low, in the range of 16-17% of GDP, the lowest among emerging-market regions and much lower as compared with the Eurozone (see Figure 5). It did not improve after the crisis as one could expect. Without an increase in the gross saving rate, CEE countries will have rely on large-scale import of saving, in the range of 8-10% of GDP annually, to reach the desired investment rate of 25% of GDP (see above). Such massive net capital inflow seems very unlikely in the post-crisis environment of financial deleveraging. As demonstrated by Figures 3 and 4, it reached the level of ca. 8% of GDP only once, in 2008, and most of it came in the form of short-term capital. The size of net foreign direct investment has been much smaller and declining in recent years. Needless to say, excessive reliance on short-term capital inflows may increase external macroeconomic vulnerability in the case of adverse shocks, as several countries learned in 2008-2009.

One can only speculate on the reasons for so low a gross saving rate. Several hypotheses come to mind: public sector dissaving, consequence of population aging (which is usually associated with private dissaving), excessive publically financed social welfare programs (which may discourage private saving) or the crowding out effect related to EU cohesion and regional funds transfers. However, all these factors except the last one are also present in the Eurozone where the gross saving rate is 5 percentage points of GDP higher, on average, than in non-Eurozone CEE countries (see Figure 5). This important question definitely needs further investigation.

Finally, the third growth factor, improvement in total factor productivity, played an enormous role in the first two decades of transition (see EBRD, 2013, p. 12, Chart 1.3) unlike in other emerging-market regions (even in Emerging Asia its role was much less prominent). This was the effect of two factors mentioned before, i.e., transition related reallocation of factors of production and integration with the Single European Market. However, these one-off sources of productivity growth are already gone. On the other hand, economic and institutional reforms which could enhance further productivity growth have been halted or even reversed in some countries. The title of the 2013 EBRD Transition Report (‘Stuck in Transition?’ – see EBRD, 2013) is very telling in this respect. In a slightly more nuanced and diplomatic way the same observation has recently been repeated in the IMF anniversary report on the region (Roaf et al., 2014).

The way ahead

Even if CEE economies manage to return on the convergence path its speed will be much slower than it used to be before 2008

The above analysis leads to some important conclusions. First, even if CEE economies manage to return to the convergence path, its speed will be much slower than it was before 2007/2008. That means the timetable of catching up with the richest Western European nations like Germany will be much longer than one would have thought ten years ago. Second and more importantly, in order to return to the convergence path (even more slowly than before the crisis) several important policy challenges must be addressed.

The low domestic saving rate is one of them. CEE economies can no longer expect that large-scale capital inflow will be able to close the saving-investment gap as seemed to be possible in the short period of the mid-2000s.

Another challenge will relate to the steadily decreasing cohorts of working-age population. However, gradual increases in the effective retirement age and the labour market participation rate, and the adoption of more flexible migration policies could ease at least partly the deficit in labor resources.

A well-designed reform agenda could boost productivity growth. Among the most urgent reform measures are the modernization of excessive welfare state provisions (to reduce labor costs), increasing the flexibility of the labour market, adjusting education to the needs of contemporary labour markets, fiscal consolidation, a return to privatization, improving the business and investment climate, governance and rule of law, fighting corruption and organized crime, etc.

In structural terms, most CEE economies tried to build their comparative advantages in manufacturing (mostly in the intermediate stages of global production chains) and service sectors. They competed with lower wages and salaries (as compared to Western Europe) of the relatively well-educated labour force. This was enough to encourage several trans-national corporations to base their production and service centres in the region. However, as labour costs (direct and indirect) in CEE gradually increase and the competition of lower-cost emerging-market producers (especially in Asia) becomes stronger, those comparative advantages may disappear. Moving up the value chain and towards more knowledge-intensive sectors (the natural market niche for higher-wage economies) requires improving innovativeness, and higher spending on research and better education.

Similar reforms in other non-CEE EU economies, especially in northern Mediterranean ones, can provide a much needed synergy and long-term demand boost. On the EU level, deepening the Single European Market, particularly in services and infrastructure sectors, completing the Banking Union and strengthening fiscal and macroeconomic discipline will help to improve growth prospects for the entire continent, including its CEE part. Finally, on the global and interregional level the pro-growth impulses should include progress in trade liberalization and financial sector reform, improved coordination of macroeconomic policies between the main players and well-balanced deal in respect to policies addressing climate changes.

This is an uneasy agenda in political terms. However, if not implemented soon, five years from now the 30th anniversary of transition and 15th anniversary of the first EU Eastern Enlargement will be celebrated in more pessimist moods.

I would like to thank Guntram Wolff and Zsolt Darvas for their critical comments to the earlier version of this article. Obviously I accept the sole responsibility for its content and presented opinions, conclusions and policy recommendations.

References:

EBRD (2013): Transition Report 2013. Stuck in Transition?, European Bank for Reconstruction and Development, London

Luengnaruemitchai, P. & Schadler, S. (2007): Do Economists’ and Financial Markets’ Perspectives on the New Members of the EU Differ?, IMF Working Papers, WP/07/65

Roaf J., Atoyan R., Joshi B., Krogulski K. et al. (2014): 25 Years of Transition: Post-Communist Europe and the IMF, Regional Economic Issues, Special Report, International Monetary Fund, Washington, D.C.

[1] This is a revised and reedited version of my presentation delivered at the Conference on ‘Building Market Economies in Europe: Lessons and Challenges after 25 Years of Transition’ organized by the National Bank of Poland and International Monetary Fund in Warsaw, October 24, 2014. The original presentation was titled ‘CEE and CIS Economies: Uncertain Prospects of Economic Convergence’. The main difference with the original presentation is leaving CIS economies out of this paper. They require a separate analysis as they followed a slightly different path of economic development.

[2] Germany recorded two years of GDP in this period: by 0.4% in 2003 and 5.1% in 2009, according to the IMF World Economic Outlook, October 2014 database.

About the authors

Related content

European Union cohesion project characteristics and regional economic growth

A new approach, which estimates 'unexplained economic growth', provides insights into the types of European Union cohesion projects that produce bette

The role of Cohesion policy in the fight against COVID-19 with Elisa Ferreira

How can cohesion funds help the National, regional and local communities that are on the frontline in countering the coronavirus and the resulting eco

Cross-border, but not national, EU interregional development projects are associated with higher growth

Our calculations reveal that places where EU regional development projects bind together participants from different countries experience higher econo

Deep Focus: Making a success of EU cohesion policy

Bruegel senior fellow Zsolt Darvas talks to Sean Gibson in this Deep Focus podcast about how the EU can improve its cohesion policy, citing the best e