The maths behind an amended Greek plan

While Mr Mr Varoufakis’s plan was received coldly by euro-area partners, recent media reports suggest that a compromise is in the making. In this

Last week I published my assessment of Greek Finance Minister Yanis Varoufakis’ draft plan, and promised to do some calculations to illustrate its impacts. Mr Varoufakis abandoned the earlier haircut demand of Syriza that I welcomed as a major step towards a Greek compromise, but noted that some elements of his plan are not feasible and instead I proposed some alternative measures, like a new ESM programme. While Mr Varoufakis’s plan was received coldly by euro-area partners, recent media reports suggest that a compromise is in the making (see for example a Eurointelligence report here).

In this post I present some numerical simulations of a possible plan.

I compare the impact of various measures with an updated version of the benchmark scenario of a model I used in a blog post with Pia Hüttl recently and in a paper with André Sapir and Guntram Wolff a year ago.

I considered the following options:

- Indexing loans to GDP: it is not known at the moment what kind of GDP-indexing the Greek government has in mind. If it is ‘neutral’ in the sense of not leading to an expected gain for Greece, then it could serve as a useful insurance against future GDP shocks, but would not change the expected debt/GDP trajectory. A ‘non-neutral’ indexing (which would lead to an expected gain for Greece) would be seen as a non-transparent haircut by creditors and will likely be rejected. Therefore, in my calculations below I do not consider any impact of a possible GDP-indexing on the expected debt /GDP trajectory.

- Swapping Greek bond holdings of the ECB and NCBs to perpetual bonds: as I argued, this will likely be found equivalent to monetary financing and therefore illegal. Instead, I suggested introducing a new ESM programme for Greece with a very long maturity loan and using this loan to buy back ECB/NCB holdings (or repay them when they mature). In my calculations below I consider results up to 2030, and assume no principal repayment of this new ESM loan by this date. Therefore, for my calculations it does not matter if the ESM loan has an infinite maturity (corresponding to the “perpetual bond” proposal of Mr Varoufakis) or a long but finite maturity with a grace period at least till 2030 (similar to some of the existing loans to Greece).

- The new ESM programme could have a larger volume in order to pay back the more expensive IMF loans early.

- Extending the maturities of existing euro-area loans (EFSF and Greek Loan Facility) by 10 years and eliminating the 50 basis points spread of the Greek Loan Facility can also be considered.

- Mr Varoufakis proposed a 1-1.5 % of GDP primary surplus, well below the targets of the Troika programme. In my simulations I consider two options: 1.5% and 3% of GDP.

The key questions:

- Are elements 2, 3 and 4 above sufficient to counterweight the impact of the smaller primary surplus on the debt/GDP ratio?

- How much would these options delay the repayment of Eurozone loans?

The biggest difficulty in answering these questions is the quantification of the growth impact of a smaller primary surplus. Recent research suggests that the so-called fiscal multiplier is high in recessions (see for example Dell'Erba et al, 2014), and according to the Winter 2015 forecast published by the European Commission last week, the Greek output gap is expected to be -6% of potential GDP in 2015 (despite the expected 2.5% real GDP growth). A lower primary surplus may impact expectations in various ways (for example positively, if the lower surplus is seen as a lower drain on the economy, or negatively, if it is seen as a threat to public debt sustainability) with feedback on future GDP growth.

The overall impact is pretty uncertain. In my simulation I use a “net” fiscal multiplier (i.e. a multiplier that takes into account the revenue-generating impact of the fiscal expansion) as calculated by Dell'Erba et al (2014): they found that during protracted recessions, the five-year cumulative multiplier is 2. Their charts suggest that there are some later impacts too, so I assume that by the 10th year, the cumulative multiplier is 2.5. The multiplier estimate of Dell'Erba et al (2014) considers real GDP and a faster real growth may have an impact on inflation, so the overall impact on nominal growth can be larger. Yet I do not consider this effect, because Greece has high unemployment and should improve its price-competitiveness. In the annex I plot the implied nominal GDP growth rates.

Let me also note that since most of Greek public debt is owned by non-residents, a lower primary budget surplus and thereby a slower repayment of external debt would mean that Greece need to have a smaller trade surplus to keep its balance of payments under control.

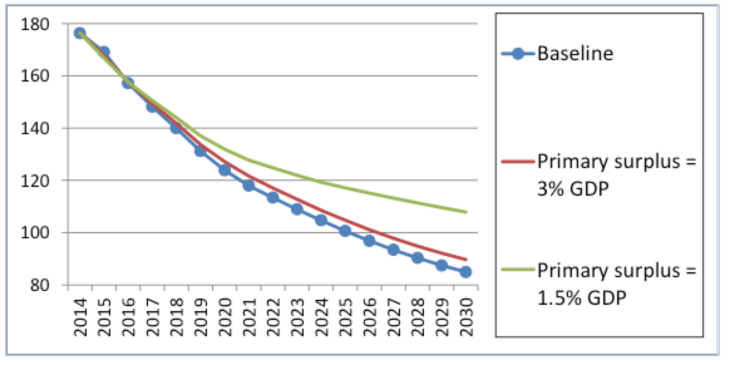

The figures below show my results. Let’s start with the case when the primary budget surplus is lowered but there is no further official support to Greece: the current official loans are repaid as scheduled and the financing gap is fulfilled by borrowing from the market at an interest rate of about 5% (see annex). According to Figure 1, a 3% primary surplus would not make a major difference relative to the baseline scenario in terms of the debt/GDP ratio, but a 1.5% primary surplus would lead to a much higher debt/GDP ratio. Yet in both cases Greece would need to borrow more from the markets: instead of the already quite large €45 billon market borrowing need by 2020 as in our baseline scenario, Greece would need to borrow €66 billion if the primary surplus is reduced to 3% and €87 billion if it is reduced to 1.5%. I do not think it very likely that markets would fund Greece in such amounts (and even more after 2020) at affordable rates.

Figure 1: Debt/GDP scenarios for Greece: Lower primary surplus, no change in official loans

Source: author's calculations

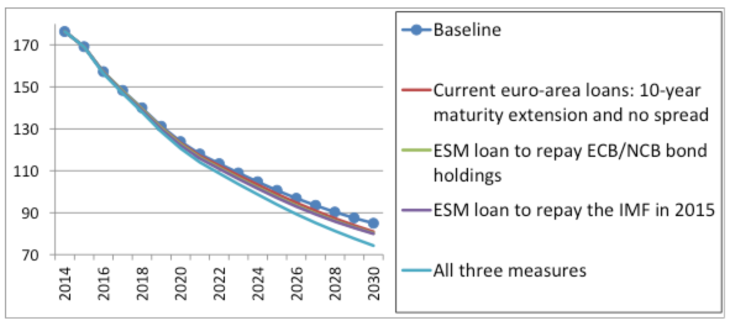

Let me continue with the various possibilities of official lending support to Greece under the assumption that the primary surplus targets are not lowered (Figure 2). One possible measure would be to extend the maturities of current euro-area loans (EFSF and bilateral) to Greece by 10 years and eliminate the 50 basis points spread on bilateral loans. Another option is to take a new and long maturity ESM loan to repay the Greek bond holdings of the ECB and national central banks when they mature. A further option is to repay the IMF in one go in 2015 from a new ESM loan. Individually, these measures would not change the debt/GDP ratio significantly relative to the baseline, but their combined effect would be sizeable, by reducing the debt ratio to 121 in 2020 and 74 by 2030 from the baseline numbers of 124 and 85, respectively.

Figure 2: Debt/GDP scenarios for Greece: Same (baseline) primary surplus, various euro-area measures to help financing

Source: author's calculations

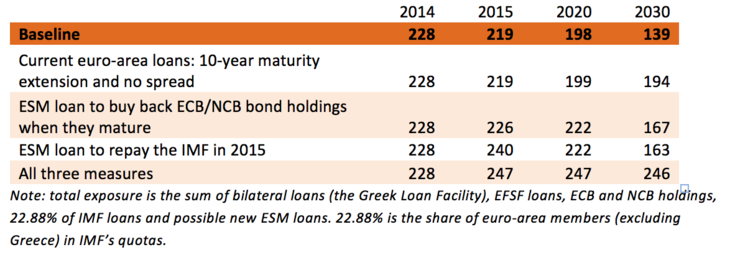

Extended loan maturities and new ESM loans imply that the exposure of Eurozone lenders to Greece is prolonged and/or increased. Table 1 shows that in the current scenario, Eurozone’s exposure would decline to €139 billion by 2030, while if all three financing measures are adopted, it would increase to €246 billion.

Table 1: Total Eurozone exposure to Greece under alternative official financing scenarios (€ billions)

Note: total exposure is the sum of bilateral loans (the Greek Loan Facility), EFSF loans, ECB and NCB holdings, 22.88% of IMF loans and possible new ESM loans. 22.88% is the share of euro-area members (excluding Greece) in IMF’s quotas.

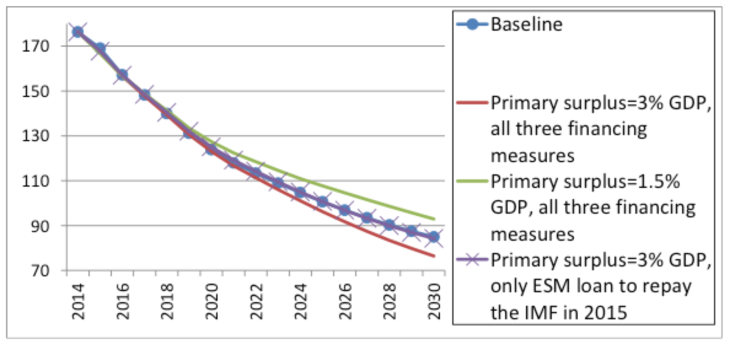

Finally, Figure 3 looks at the combined impact of the three financing options and a lowered primary surplus. The financing measures I considered would not able to counterweight the impact of the lowering of the primary surplus to 1.5% of GDP, but they would more than offset the impact of a lowering to 3%. If the 3% primary surplus is combined with only one of the three main financing supports, the resulting debt/GDP scenario becomes very similar to the baseline. As an illustration, Figure 3 shows the case when the primary surplus is 3% and among the financing support measures only a new ESM loan is granted to repay the IMF loans early.

Figure 3: Debt/GDP scenarios for Greece: Lower primary surplus and additional euro-area financing support

Source: author's calculations

Key questions related to this plan

What is the essence of this deal?

- Beyond the short-term funding gap, which may be filled with a “bridge agreement”, there is a more fundamental medium to long-term problem: market borrowing rates for Greece will likely remain too high, even if an agreement is reached and thereby current market yields fall. If Greece only gets a short-term fix, debt sustainability problems may return in a few years and in the meantime the resulting uncertainty could hold back economic activity.

- The ESM is able to offer loans at a much cheaper rate than the market. One may regard a new ESM programme as “throwing good money after bad”, but this is not true: without providing a new loan, the previous loans may indeed turn to bad, but a new loan could shield the previous loans.

- The difficult choice euro-area partners face is whether to help Greece with new cheap loans in order to improve the sustainability of Greek public debt and to hope that the current and future Greek governments will meet the country’s commitments in the next decades, or do not offer any new help, which would significantly increase the risk of losses on current loans. The choice will likely be political.

Why would Greece request a new ESM programme which would have new conditions attached?

The reality is that Greece will not be able to repay its maturing debts without new financing. Its options are limited:

- Relying on markets would be simply too expensive and an eventual increase in short-term treasury bill issuances would not be a lasting solution.

- As I noted, swapping ECB-held Greek government bonds for perpetual bonds will not work.

- After Greece’s clumsy attempt last week to threaten Eurozone partners by asking for assistance from Russia, the Greek government has probably realised that this is a bad idea which would have far-reaching consequences.

- The only reasonable option is to get more funding from euro-area partners.

If Greece pays back the IMF from a new ESM loan, then the government can declare its success in turning down the ill-famed Troika. A new ESM programme would come with new conditions which could involve some of the government plans, and so could be better sold to Greek voters.

What if there is no agreement?

In the absence of an agreement between Greece and euro-area partners, two scenarios could emerge:

- the Syriza government could default on some of its obligations, which would have damaging consequences and may lead to a Grexit (see our earlier blogpost on this issue here);

- the Syriza government could fail, forcing new elections, which would have uncertain results. A possible victory of the New Democracy party may lead to an agreement with euro-area partners, but a new election could easily lead to political paralysis, which could again lead to a Greek default and possible wide-ranging consequences.

Many of Syriza’s election pledges have to be reconsidered, and they have already given up a number of them. But they will not give up all their promises. It is clearly in the common interests of euro-area partners and the new Greek government to find a reasonable compromise.

Annex: The model and the main scenario assumptions

The annex of a blogpost we wrote with Pia Hüttl last month presents the essence of our model. Here I only compare our baseline scenario with the projections of the European Commission and the IMF, and specify the primary balance, growth and market interest rate assumptions.

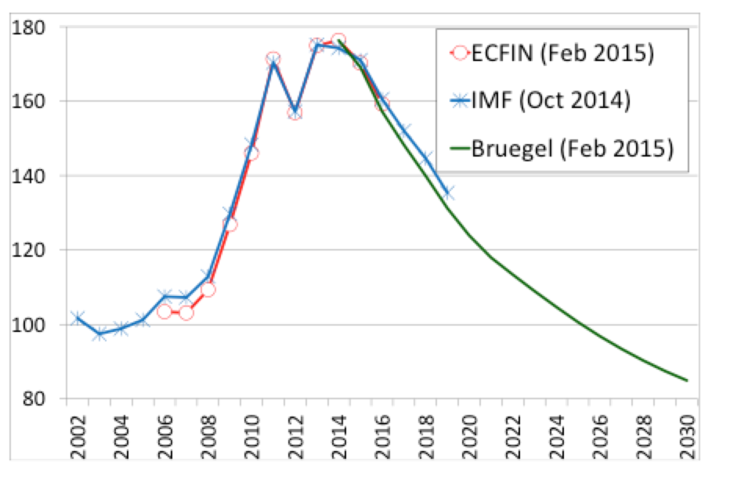

Our baseline scenario for the public debt/GDP ratio is practically equal to the European Commission’s February forecast for 2015-16, and slightly more optimistic than the IMF’s October 2014 projection for these years. This difference may be explained by the lowering of the interest rates and their expected future values from October 2014 to February 2015.

Figure 4: Our baseline scenario in comparison with the February 2015 Commission and October 2014 IMF debt projections

Source: author's calculations

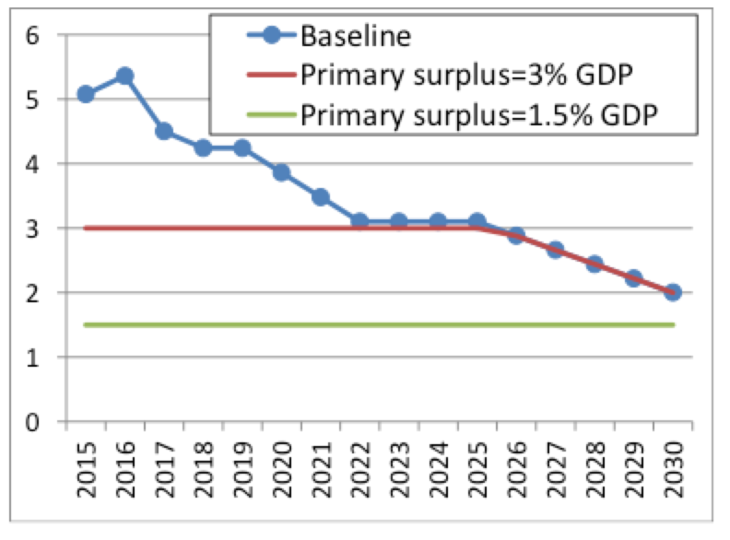

The baseline primary balance scenario was designed as follows:

- 2015-16: European Commission’s February 2015 forecast;

- 2017-19: IMF’s October 2014 forecast;

- 2020-22: we assumed that the primary surplus is gradually reduced to 3.1% of GDP, which the average primary surplus for successful consolidations in advanced economies as calculated by Abbas et al (2013);

- 2026-2030: we assumed a gradual reduction to 2% of GDP.

We considered the alternative 3% and 1.5% of GDP primary surplus scenarios as indicated on the chart below.

Figure 5: Primary balance (% GDP) in the baseline and alternative scenarios

Source: author's calculations

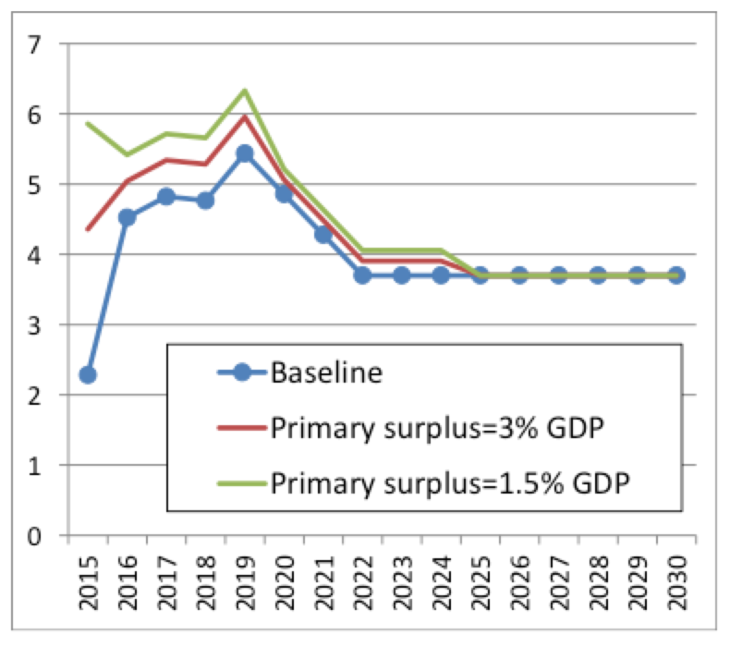

The baseline nominal GDP growth scenario was designed as follows:

- 2015-16: European Commission’s February 2015 forecast;

- 2017-19: IMF’s October 2014 forecast;

- 2020-22: we assumed that nominal growth is gradually reduced to 3.7% of GDP, which is the Consensus Economics long-term forecast for Spanish growth.

Figure 6 shows annual growth scenarios of the baseline scenario and the scenarios with the reduced primary surpluses.

Figure 6: Nominal GDP growth rate (% per year) in the baseline and alternative scenarios

Source: author's calculations

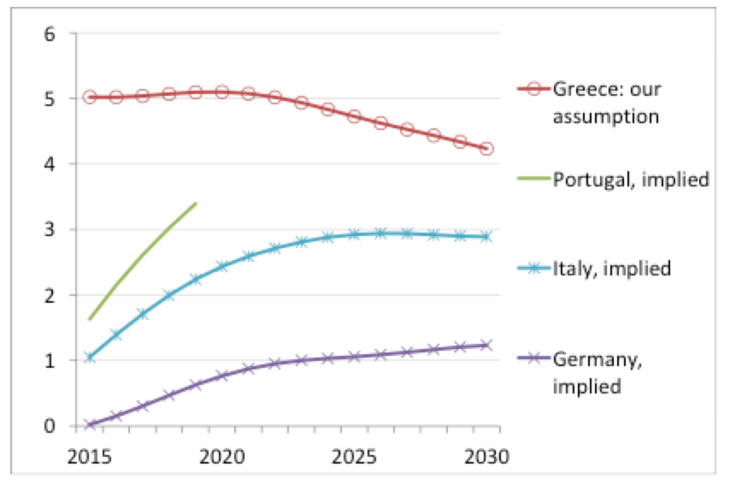

Since current and market-based expectations for Greek yields are heavily influenced by the current financial market tensions, I do not use current Greek yields. In our previous work we calibrated the interest rate at which Greece would be able to borrow from the market on the basis of expected Portuguese interest rates (plus an assumed spread). Unfortunately Portuguese yields are not available for maturities over 10 years and therefore I chose to base the Greek market interest rate on expected German interest rates. Specifically, I assumed that if an agreement is reached between euro-area lenders and Greece, in 2015 the 6-year maturity Greek borrowing rate will be 500 basis points above the German 6-year interest rate, which spread gradually declines to 300 basis points by 2030. The chart below shows the expected interest rates for Germany, Italy and Portugal and our assumption for Greece. Our assumption implies an approximately 5 percent interest rate on new market borrowing in the next few years, which may be too optimistic. If so, the benefit of obtaining an ESM programme would be larger than the benefit I have calculated.

Figure 7: Expected 6-year government bond yields of Germany, Italy and Portugal and our assumption for Greece

Source: author's calculations

Note: “implied” means market expectations for future interest rates, as derived from the term structure of interest rates using data of 6 February 2015.

About the authors

Related content

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and

ΕΥΡΩΕΚΛΟΓΕΣ ΚΑΙ ΤΟ ΜΕΛΛΟΝ ΤΗΣ ΕΥΡΩΠΗΣ

Είναι γεγονός ότι οι τωρινές εκλογές λόγω της ανάπτυξης των κομμάτων του λαϊκισμού είναι κάπως διαφορετικές από τις προηγούμενες. Αλλά πιστεύω ότι όλε

After the ESM programme: Options for Greek bank restructuring

With the end of the Greece support programme, authorities now have scope to focus on the legacy of NPLs and excess private-sector debt. Two wide-rangi

A new statistical system for the European Union

Quality statistics are essential to economic policy. In this essay, Andreas Georgiou demonstrates the existence of fundamental risks inherent in the E