Macroeconomic performance and election outcomes

The results of last week’s election in the UK have generated a debate on the role of macroeconomic performance in electoral success and, in particular

The macro performance of the coalition

David Spencer writes that he problem is that the country’s economic performance can be spun in different ways.

Niall Ferguson writes that few governments since 1945 have achieved comparable economic results from such a difficult starting point. The UK had the best performing of the G7 economies last year, with a real gross domestic product growth rate of 2.6 per cent. Far from being in depression, the UK economy has generated more than 1.9m jobs since May 2010. UK unemployment is now 5.6 per cent, roughly half the rates in Italy and France. Weekly earnings are up by more than 8 per cent; in the private sector, the figure is above 10 per cent.

Simon Wren-Lewis writes that he has not come across a single non-City, non-partisan economist who does not concur with the view that the performance of the coalition has been pretty poor (or simply terrible), yet polls repeatedly show that people believe managing the economy is the Conservatives’ strength. This trick has been accomplished by equating the government’s budget with the household, and elevating reducing the deficit as the be all and end all of economic policy. This allowed Cameron to pass off the impact of bad macro management in delaying the recovery as inevitable pain because they had to ‘clear up the mess’ left by their predecessor. For that story to work well, the economy had to improve towards the end of the coalition’s term in office. The coalition understood this, which was why austerity was put on hold. In the end the recovery was pretty minimal (no more than average growth), and far from secure (as the 2015Q1 growth figures showed), but it was enough for media to pretend that earlier austerity had been vindicated.

David Andolfatto writes that austerity evidently killed GDP, but not the labour market. Frances Coppola explains that the rising participation rate, among single mums and the sick & disabled are due to cuts in welfare entitlements, while older people staying on in employment (or returning to it) is due to rising pension age, particularly for women, and low interest rates.

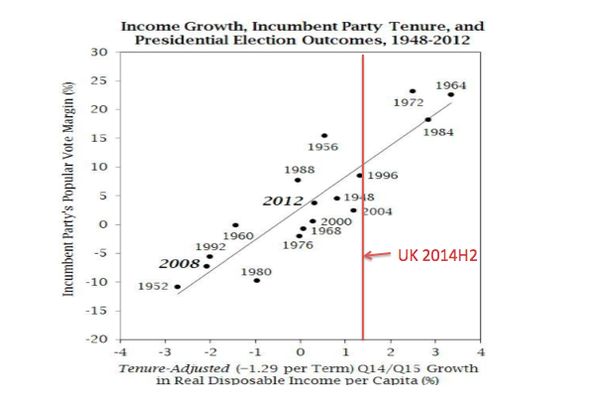

Elections, overall record and improvement in election year

Paul Krugman writes that Britain’s election results are consistent with the general proposition that elections hinge not on an incumbent’s overall record but on whether things are improving in the six months or so before the vote. The Liberal-Conservative coalition imposed austerity for a couple of years, then paused, and the economy picked up enough during the lull to give them a chance to make the same mistakes all over again.

Source: Paul Krugman

Larry Bartels writes that the figure above is derived from the following very simple regression analysis:

Incumbent Party Margin = 9.93 + 5.48 × Income Growth – 1.76 × Years in Office.

Incumbent Party Margin represents the incumbent party’s national popular vote margin in percentage points. Income Growth is measured by the change in real disposable personal income per capita in the second and third quarters of the election year (Q14 and Q15 of the president’s term in the US), also in percentage points. Years in Office is a counter indicating how long the incumbent party has held the White House. The regression parameters are estimates based on data from the 17 US presidential elections since the end of World War II and “explains” more than three-quarters of the observed variation in election outcomes.

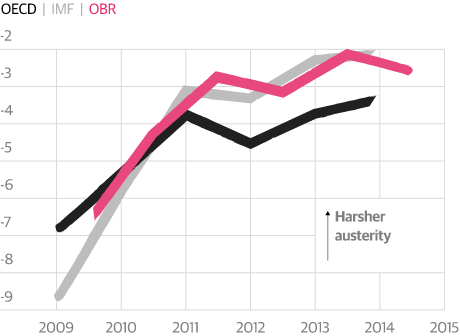

Front loaded austerity and election prospects

Paul Krugman writes that depressing the economy for the first half of your term in office can be a very smart move. If some positive growth, eventually, means that your policies have been successful, then a policy of simply shutting down half the economy for a year or two, then letting it start up again, is a smashing success.

Source: IMF, OECD, and OBR via The Guardian

Cyclically adjusted primary balance, percent of GDP

Simon Wren-Lewis writes that in a demand led recession, austerity leads to some years where growth is less than it would have been otherwise, followed by later years where growth is more than it would have been otherwise. Austerity reduces the level of output from what it otherwise might have been. In the simplest case, once we come out of recession output goes back to the level it would have been without austerity.

Paul Krugman writes that if this counts as a policy success, why not try repeatedly hitting yourself in the face for a few minutes? After all, it will feel great when you stop.

Read more blogs reviews: