Italy’s bail-in headache

Weakness in the Italian banking sector is a major concern for the euro area. Retail investors stand to lose out if BRRD bail-in rules are strictly app

The current market concern about Italian banks is hardly surprising. I have discussed at length Italian banks’ poor performance in previous stress tests, as well as the Non-Performing Loans (NPLs) that afflict them. I have also looked at two “creative” episodes of bank resolution conducted in summer and autumn 2015, involving the first cases of junior debt bail-in in Italy. The problems in the Italian banking system have remained unaddressed until very recently, when a government guarantee scheme for NPLs (known as GACS) and a backstop fund (Atlas Fund) were created.

The European Banking Authority (EBA) stress tests due at the end of the month may highlight the need for further recapitalisations, and there has been much talk recently on how this should be addressed — particularly regarding the troubled Monte dei Paschi di Siena). Market research estimates that Monte dei Paschi di Siena’s capital shortfall alone could range between EUR 2 and EUR 6 billion[1].

In evaluating the various options, three problems will need to be addressed. First, the balance between public and private contribution to the banks’ recapitalisations and the implications for banks’ creditors. Second, the need to preserve financial stability and avoid spillovers from weaker banks to the rest of the system, or from Italy to other countries. Third, the consequences of mis-selling which occurred in the past and has significant consequences for today’s situation.

The rule

Under EU state-aid rules, additional capital requirements should in the first place be covered from private sources. The fact that a bank requires extraordinary public support is normally a trigger for resolution (Art. 32.4.d). In this case, the Bank Recovery and Resolution Directive (BRRD) foresees a mandatory preliminary bail-in of 8% of total liabilities before public capital can be used.

The prospect of bank resolution in Italy is complicated by the fact that a large share of banks’ bonds is held by retail investors who - as evident in the previous cases of resolution in 2015 - often had little awareness of the actual risk they were signing up to.

In Italy about a third of bank bonds are held by household retail investors (figure 1). This is a much larger percentage than in most other euro-area countries and it is partly due to the preferential tax treatment of interest income on bonds, which was in place between 1996 and 2011. The last IMF Article IV estimates that for the majority of the 15 largest Italian banks (i.e. those supervised by the Single Supervisory Mechanism) the 8% BRRD requirement would currently imply bail-in of retail investors in subordinated debt. For about two-thirds of these banks, losses would also be imposed on some senior debt (EUR 200bn of which is held by retail investors). For Monte dei Paschi di Siena, if the shortfall were in the upper part of the range estimated by market research, the 8% bail-in requirement would imply bail-in of all or almost all junior debt (which amounts to 5 billion).

The exception

Article 32(4.d) of the BRRD contains an exception to this rule. It state that “extraordinary public financial support” does not trigger resolution if it is required “in order to remedy a serious disturbance in the economy of a member state and preserve financial stability” and granted that it is “at prices and on terms that do not confer an advantage upon the institution.”

This exception is limited to solvent institutions; the extraordinary public support shall be of a precautionary and temporary nature, and not be used to offset losses that the institution has incurred or is likely to incur in the near future. Moreover, the extraordinary injections are limited to the amount necessary to address a capital shortfall established in a stress test, asset quality reviews or equivalent exercises, such as the EBA stress tests due at the end of the month.

If these conditions are met, then the State could provide a precautionary recapitalisation without triggering the resolution procedure and the associated 8% bail-in requirement. The precautionary recapitalisation would result in a case of state aid, which is normally subject to a lower burden sharing requirement, limited to equity and junior debt.

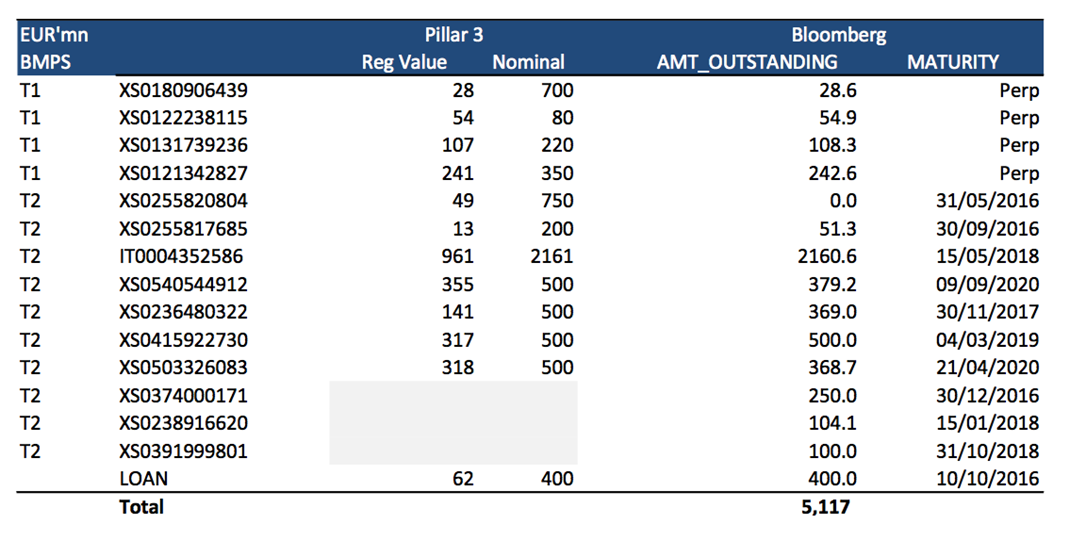

This solution would reduce but not eliminate the political burden of bail-in, because Italian retail investors hold about half (EUR 31bn) of total bank junior debt, which would still need to be bailed in (figure 2). For the troubled Monte dei Paschi di Siena, outstanding subordinated debt amounts to EUR 5bn, of which almost 65% was sold to retail clients (table 1 and Repubblica).

Table 1 - outstanding Monte dei Paschi di Siena junior debt

Source: Morgan Stanley research

The exception to the exception

Theoretically, there could be a way to limit junior bail-in under Article 32. The application of Article 32 results in a state aid case, which is governed by Article 107 TFEU. For this aid to be approved, it would need to be seen as remedying “the damage caused by [...] exceptional occurrences” (Article 107(2.b)) or remedying “ serious disturbance in the economy of a member state” (Article 107(3.b)). Article 107 (3.b) was used in cases of state aid to banks during the global financial crisis and more recently, whereas article 107(2.b) has traditionally been used in the stricter case of natural disaster.

Assuming that the Italian government can make a sufficiently strong case for aid to be approved under one of these two articles, which would require demonstrating the existence of a clear link between Brexit and banks’ capital problems, then the question is what burden sharing requirement would apply.

The European Commission’s Banking Communication of 2013, which gives details on the application of state aid rules to support measures for banks in the context of the financial crisis, states that “adequate burden-sharing will normally entail, after losses are first adsorbed by equity, contributions by hybrid capital holders and subordinated debt holders”[2].

However, Recital 45 in the Banking Communication argues that “an exception to the requirements [...] can be made where implementing such measures would endanger financial stability or lead to disproportionate results”, an argument that the Italian government could theoretically use to call for suspending bail-in of retail junior bondholders.

The exception could cover “cases where the aid amount to be received is small in comparison to the bank's risk weighted assets and the capital shortfall has been reduced significantly in particular through capital raising measures”. It is not obvious that a bank like Monte dei Paschi di Siena would be able to reduce significantly its capital shortfall through private capital raising, but the recently created Atlas Fund, which is structured to qualify as a private investor, could be used to invest and reduce the shortfall.

The problem is that Atlas has only EUR 1.75bn left after underwriting the capital raise of two smaller banks earlier this month. Whether EUR 1.75bn would be considered a “significant reduction” of the shortfall will depend on the size of the shortfall that will come out of the EBA stress tests. Assuming the shortfall for MPS is between 2 and 6 billion, Atlas could potentially cover between 87% and 29% of it, assuming that no other banks need similar help.

The headache

The Italian government evidently faces a thorny political conundrum. On the one hand, the stress test and the current market pressure will most likely warrant a strengthening of banks’ capital position to reassure investors. On the other hand, BRRD normally makes the use of public funds subject to at least a minimum bail-in of junior debt, which is bound to hit a large proportion of retail savers.

While bail-in of junior bondholders has happened as recently as last year in Italy, wiping out retail investors is a dreadful perspective at this time for a government which faces a crucial referendum in October and which received worrying signals from recent local elections. Calls against bail-in requirements have also come from the governor of the Bank of Italy. Meanwhile, the president of the Italian Banking Association recently stated that BRRD is against the Italian Constitution, whose Article 47 says that the Republic "encourages and protects" saving.

Avoiding a bail-in of junior bond-holders might be possible in the convoluted way discussed. This would require that (i) the Italian government obtains the green light for a precautionary recapitalisation under Article 32(4.d) of BRRD; (ii) the resulting state aid is approved under Article 107 TFEU and (iii) the “financial stability” clause in the 2013 Banking Communication is granted to suspend burden sharing of junior bondholders. Even assuming that all these conditions fall into place, the most important question remains whether burden sharing should actually be avoided. In my view, there are three reasons suggesting it should not.

First, the “constitutional right to save” argument that is being made by some in Italy is certainly appealing to the public but it is misplaced. The whole idea neglects the fundamental difference between savings and investment. Placing savings into banks’ junior bonds is an investment, and it bears risk. The Italian constitution does not and should not grant a right to be always and unconditionally bailed out of bad investment decisions. Indeed, allowing investors to believe this would be dangerous. What people should be granted is the right to receive proper information and not be misled into risks of which they are not aware or which they are not prepared to take.

This brings me to the issue of mis-selling, which surely plays an important role in today’s situation. Monte dei Paschi di Siena offers a good example. Its largest outstanding junior bond, due in 2018, was sold in the banks’ branches to anyone willing to invest at least EUR 1000. Coincidentally, this is the same minimum investment required for buying Buoni Ordinari del Tesoro — a type of (safer) government bonds in which Italian households traditionally invest. The Italian Securities and Exchange Commission signed off on this back in 2008.

Mis-selling should obviously have been better prevented in the past, but it does not per se justify the bailout of all junior bondholders today. It would be wrong to assume before investigation that all junior holders were unaware of the risk they took, and it would set a tricky precedent. The Italian government should rather opt for bailing in junior debt now and establishing an ex-post compensation scheme for the retail investors who can be truly considered victims of mis-selling.

This has been done already, to compensate the retail holders involved in the Italian resolution cases of 2015. They have been bailed in, and then given the option to ask for a reimbursement of 80% of the sum spent to buy their junior bonds, provided that they had bought before 12 June 2014, that they owned less than EUR 100 000 in property assets at the end of 2015 and that their 2014 income was below EUR 35 000 euro. It would be odd and confusing to protect junior bondholders ex ante now that BRRD is in force, after bailing in very similar investors last year.

Second, the risk to financial stability, which is at the core of the argument to justify bail-in suspension, is unclear. Junior bail-in has already occurred in 2015 without major consequences. Now, the banks resolved in 2015 were admittedly tiny compared to Monte dei Paschi di Siena. Nevertheless, there is no evident reason why a precautionary recapitalisation combining bail-in of junior debt with a credible compensation scheme for mis-selling and the protection of senior creditors should necessarily result in financial instability (see also Nicolas Véron on this here).

The government may prefer to avoid bail-in rather than compensating it, because the shock will be immediate and compensation will take time, probably too long to prevent a political backlash before the October referendum. But this is a political risk, not a financial stability issue.

Lastly, the handling of the Italian banking issue has very important implications at the EU level. This is the first time that the BRRD rules would be tested in real life under stress, after entry into force in January 2016. The rationale for having BRRD rules was to finally provide certainty about how banking problems in the EU will be dealt with in the future, and ensuring a coherent application is crucial for establishing the credibility of the new regime.

There is no easy fix to this delicate puzzle. Bail-in is going to be painful in a country that scores low in terms of financial literacy and where households hold a third of all bank debt. But bending the rules to avoid even the junior bail-in that comes with the flexibility of a precautionary recapitalisation would create dangerous confusion with unpredictable effects at the EU level. The best compromise is between the two extremes: a precautionary recapitalisation with burden sharing for junior debt, protection of senior creditors and a credible reimbursement scheme for those who were wronged due to unlawful practices which should have been better prevented.

[1] Morgan Stanley, “European Banks: Stress tests - the trigger to recapitalise Italian banks”, July 6th; Moody’s, “Moody's reviews Banca Monte dei Paschi di Siena's long-term deposit and senior unsecured ratings for downgrade”, July 15th

[2] The European Court of Justice ruled on the legitimacy of this requirement on 19th July 2016, stating that Member States are not “compelled” to implement this burden sharing before granting aid, but if they don’t they take the risk that the Commission will rule the aid as incompatible with the internal market, with the consequence that aid will need to be recovered from the beneficiary bank. In my view this does not alter the substance of the Banking Communication procedure.

About the authors

Related content

Fast and furious: how digital bank runs challenge the banking-crisis rulebook

The speed of recent bank failures has shown the need for more systemic protection of the financial system.

Climate change, the next big financial threat

A warming planet poses new risks to European sovereign debt. How can the continent protect itself?

Capital markets union - why now?

What is hindering the EU from achieving a Capital markets union?

Next steps for the European Anti-Money Laundering Authority

At this invitation-only event Raluca Pruna discussed the state of the legislation to create an EU Anti-Money Laundering Authority