Providing funding in resolution: Unfinished business even after Eurogroup agreement on EMU reform

The recent Eurogroup agreement on euro-area reform foresees a greater role for the European Stability Mechanism (ESM) as a backstop to the banking uni

The Banking Union rule book dictates that when banks are deemed “failing or likely to fail”, they are either dissolved or enter a “resolution scheme”. The ECB’s Single Supervisory Mechanism (SSM) and the Single Resolution Board (SRB) both play crucial roles in the decision as well as the execution of such processes. The SSM typically decides that a bank is failing or likely to fail after consulting the SRB. The SRB then determines whether there are no alternative measures that could avoid the institution’s failure and assesses if resolution is in the public’s interest.

Funding of banks after resolution has recently become part of the euro-area political debate, as the resolution of Banco Popular in June of 2017 showed. Conceptually, two aspects have to be distinguished when considering funding in resolution: how to restore solvency and how to provide liquidity. Solvency is restored through bail-in and/or recapitalisation, including through public funds. Liquidity needs, however, need to be met differently.

Funding in resolution – an unclear framework

The question of which institution is better suited to covering liquidity needs is not independent of the question of how much firepower is required. We take a look at the numbers that were required for a number of cases since 2008.

For example, Germany’s Hypo Real Estate benefited from the provision of guarantees amounting to €145 billion, in the period between 2008 and 2010. This amount was deemed necessary in order to enable the continued operation of the bank when it faced insolvency. The resolution of Dexia in 2008 was backed by French, Belgian and Luxembourg state guarantees amounting to €135 billion, including guarantees for Emergency Liquidity Assistance (ELA) funding from the National Bank of Belgium. On the whole, liquidity support in the form of state guarantees became the most used state support tool during the financial and subsequent European debt crises in 2008-13. European governments approved the whole of €1.5 trillion in capital and asset relief, and €4.3 trillion in guarantees to their ailing banking systems.

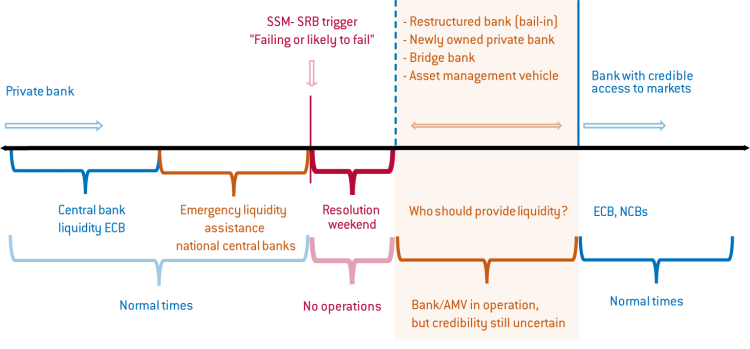

In a recent paper, we have looked at how a bank’s liquidity needs are met after it has been put into resolution. The new institution that emerges from the resolution framework can have one of the following four forms: it can be the same bank but restructured (bail-in); it can be bought and therefore have new ownership; it can be a bridge bank; or it can be an asset management vehicle.

If the institution opens up with a bank licence (i.e. the first three cases), it can get liquidity by borrowing on the market, through ordinary monetary policy operations (from the European Central Bank [ECB] and with standard collateral requirements) and through ELA (from respective national central banks and with laxer collateral requirements).

However, there is one remaining gap in the European framework that needs to be filled: the treaties allow the ECB to provide liquidity only against collateral. What happens if the newly created entity does not have sufficient collateral to meet its liquidity needs? It is not impossible to conceive that the newly created bank, having been through distress, might face greater liquidity needs than what it has in unpledged collateral, until such time as it regains market access. Clarity on liquidity provision is necessary to establish credibility in the market (see Figure 1).

Figure 1: Liquidity provision at different states: a sequence

The ECB needs to provide liquidity to banks after resolution. But in the absence of collateral, a fiscal guarantee or publicly provided collateral is needed for the ECB not to violate the EU treaties that prohibit liquidity provision without collateral. Alternatively, the liquidity needs could be met directly by a fiscal actor such as a treasury.

The current framework is incomplete and that is why the Eurogroup agreement discusses the issue in some detail. First, it is important to understand that, as such, the Single Resolution Fund (SRF) has only limited firepower to provide funding. With its size at €60bn, it could be used in part to support the recapitalisation efforts of the resolved bank, and what remains could be used for liquidity. Given the liquidity needs that we saw at the height of the financial crisis, what remains in the Fund is too small to provide liquidity support in all circumstances. Moreover, if a medium-to-large bank is to be resolved, funding needs can quickly exceed the €60bn available at the SRF. This is why the current framework has a direct ESM recapitalisation instrument. While it was constructed in such a way that it is difficult to activate, it was still an instrument allowing for the ESM to provide capital directly to banks (for an overview, see here). When it comes to liquidity, the current framework only foresees the SRF with no role for the ESM.

Assessing this week’s Eurogroup agreement

The Eurogroup deal includes important decisions on sovereign debt restructuring clauses (which we do not discuss here). It also includes important decisions on reduction of non-performing loans and progress on the bail-in capacity of banks (MREL). The latter should help avoid or minimise public recapitalisation needs of banks. The Eurogroup agreement on the ESM aims to address the weakness of funding for bank resolution. It establishes the possibility of the ESM providinge a credit line to the SRF as a ‘backstop’. The maturity of loans would typically be three years (with a possibility to extend to five years) at a margin rate of 35 basis points, as outlined in the terms of reference. The document states that:

“The common backstop will cover all possible uses of the SRF, according to the current regulation, including liquidity provision, subject to, where needed, adequate safeguards, to be discussed in 2019. These safeguards should be without prejudice to the existing legal competences of the ECB and the SRB. The Direct Recapitalisation Instrument will be replaced by the common backstop at the time it is introduced.”

The agreement also foresees that the ESM would enjoy preferred-creditor status vis-à-vis the SRB and a number of additional safeguards. Such a borrowing facility is not unlike what exists in the United States, where the Federal Deposit Insurance Corporation can borrow from the US treasury (see here). We would welcome it as a step forward.

But does the agreement address all the gaps in the framework of providing funding and, in particular, liquidity to banks after resolution? In our view, important concerns remain:

- The ESM decision-making process of unanimity would remain, making it difficult to come to quick decisions during resolution. The text expresses the intention to work on easier decision-making processes but the issue remains unresolved.

- The ESM direct recapitalisation instrument will be replaced by the credit line, i.e. the loan facility to the SRB. This means that ESM (i.e. taxpayers’) resources cannot be used for bank recapitalisation, as the SRF is funded by bank contributions. The credit line to the SRB helps extend its scope to intervene in crisis times. We interpret this as a step backwards as far as concerns the fiscal needs to complete banking union. Indeed, all resources available to the SRB will be coming from contributions from the banks – after all, the ESM can only lend to the SRB.

- The agreement is silent on how exactly the SRB would provide liquidity support to banks when it borrows from the ESM. In particular, no clarity on the operational details is given.

- For the SRB, it may be unattractive to borrow from the ESM due to the latter’s preferred-creditor status. It may make it impossible for the SRB to go on the market and issue bonds on its own, which in turn could have consequences for its liquidity provisioning operations.

Conclusions and the way forward

For a funding-in-resolution framework to be credible, it has to distinguish clearly between solvency and liquidity needs. The former need to be covered by bail-in and, where necessary, publicly funded recapitalisation. The decision on MREL should help reduce the cost of future banking crises for taxpayers. When it comes to liquidity, however, it is the role of the central bank to meet those needs as they arise. But absent of appropriate collateral, fiscal guarantees would be required for the central bank to be able to provide liquidity without jeopardising its own balance sheet (in line with the Treaties). Alternatively, a fiscal agent (for example, a national treasury) could provide liquidity on its own by borrowing in the markets.

The additional credit line foreseen in the agreement increases the capacity of the SRB to provide funding to banks as it is unlikely that the SRB could borrow at such favourable rates (ESM rate plus 35 basis points) in the markets on its own. Arguably, this construction would allow the SRB to have sufficient funds to recapitalise banks in case of a medium-sized banking crisis, after exploiting the bail-in instruments. For larger systemic crises, however, other forms of public funding would need to be mobilised to recapitalise banks and prevent a major systemic deterioration of the economy through a failing financial system.

Furthermore, the framework provided remains unclear when it comes to liquidity provision after resolution. The question is how the credit line can be used to ensure liquidity provisioning. An ideal framework would either provide a guarantee to the bank concerned, or pledge a bond that could be used as collateral.

- The former guarantee could be pledged as a collateral to the national central bank to receive ELA. This is the way liquidity was ensured during the financial crisis and the guarantees were given by national treasuries. But the scope of the SRB, even with a credit line from the ESM would be limited to guarantees of 120bn – too small to deal with a bigger crisis.

- Alternatively, the SRF could issue bonds to lend to the banks, which it can then use as collateral for normal liquidity operations with the ECB. The current framework is not suitable, however, for such a construction. In particular, borrowing from the ESM would make it more difficult for the SRB to issue bonds with a good credit rating, due to the preferred-creditor status of the ESM.

Overall, we doubt that the new backstop construction is a substantial improvement of the way funding can be provided to banks during resolution processes. The removal of the direct recapitalisation instrument – difficult though it was to use – reduces the scope to use taxpayers’ resources for recapitalisation. While this is in principle desirable, it ignores the importance of public resources during systemic crisis for backstopping the financial system. More importantly, the preferred-creditor status of the ESM would make it more difficult for the SRB to issue bonds of a high rating that could be used as collateral in liquidity operations with the ECB.

Europe’s banking union remains incomplete after the Eurogroup’s agreement on reform of the economic and monetary union (EMU). It continues to suffer not only from a missing European Deposit Insurance System; It also suffers from a lack of clarity on how the roles between national treasuries, the ESM, the SRB and the ECB are divided in bank resolution. This risks creating financial instability. Finally, the currently complex decision-making process is bound to become even more complex with the involvement of the ESM in lending to the SRB. The banking union framework therefore remains incomplete.

About the authors

Related content

The European Central Bank’s timid operational framework update

The European Central Bank announced limited changes to its operational framework – which is probably right given current uncertainty

The European Central Bank, inflation tolerance and the last mile

Price stability is all about climate change

The European Central Bank should bring in cheaper greening funding for banks, to offset the impact of high interest rates on the energy transition