Incorporating political risks into debt sustainability analysis

DSA applies to crisis countries only, but an early warning system identifying vulnerabilities is relevant for all countries. A more general, less stri

When lenders such as the International Monetary Fund or the European Stability Mechanism want to assess whether a country meets the criteria for receiving international assistance, they carry out a debt sustainability analysis (DSA). This involves debt simulations and scenarios that evaluate the likelihood of countries meeting their future obligations. The Greek debt crisis, however, exposed the drawbacks of traditional debt sustainability analysis. During crisis episodes uncertainty is high, and therefore focusing on average dynamics, or on a few scenarios, can conceal potential risks. DSA applies to crisis countries only, but an early warning system identifying vulnerabilities is relevant for all countries. A more general, less stringent, debt vulnerabilities analysis (DVA) could be used to assess countries’ debt management policies and identify vulnerabilities, without leading immediately to policy consequences.

DVA would not carry the significant connotations of DSA. For instance, it could be used to spot when a country has debt that is non-decreasing from very high levels, even though that country might pass the DSA test. The Dutch State Treasury Agency evaluates its public debt management practices every three years, even though its debt-to-GDP ratio is only 50%. The agency carries out a comprehensive analysis prior to a political review, including an evaluation of vulnerabilities, and the implications for policy are transmitted to the Dutch parliament by the finance minister (the 2019 evaluation is available here).

Such broader analysis could, in particular, account for political risks that are currently used to guide expert judgment by the institutions, but are not part of DSA. The IMF makes references to political risks and policy uncertainty in its Article IV Consultation reports[1], while the European Stability Mechanism uses governance and/or political risk ratings in its Sovereign Vulnerabilities Index, and the European Central Bank uses such ratings to generate a heat map, classifying countries in the bottom ratings tercile as RED, those in the top tercile as GREEN, and those in the middle as YELLOW. Such broad-brush treatment of political risks is useful, but unlikely to be effective.

Political instability and economic policy uncertainty can be key determinants of sovereign debt dynamics, but are not captured adequately, with quantitative rigour, by traditional DSAs. When the IMF, the ECB or the ESM carry out DSAs, they take into account risk factors including the country’s fiscal consolidation path, GDP growth and financial assumptions relating to the sovereign bond yields. They also consider debt aging costs, macro (bank) stress tests, inflation shocks, structural shocks, contingent liabilities and privatisation receipts. We argue that political risk factors can also be quantified, and should be part of debt analysis.

Our suggestion becomes attractive because the systematic quantification of political risks has been receiving increasing attention, driven in part by the compilation of databases that facilitate cross-sectional studies. Such databases include the Ifo World Economic Survey-WES (25 years of semi-annual data for 66 countries), the World Bank (25 years of annual data for 214 countries), the ICRG index (40 years of annual data for up to 140 countries) and the Dallas Fed’s Economic Policy Uncertainty index (25 years of monthly data for 21 countries). Impetus has also been created by theoretical models and empirical evidence that the markets price political risks.

Building on these advances, political risks can be incorporated in DSA (and DVA) and can materially affect the conclusions. We first identified (see Gala et al, 2018) two key quantifiable aspects of political risk, and second distinguished between short-term ambiguity about the political factors that cannot be measured, and long-term risks that are modelled probabilistically. Third, we used a combination of narrative scenarios about the short-term ambiguity, and calibrated probabilistic scenarios for long-term risks (see Zenios et al, 2019), to obtain a comprehensive heatmap of high-risk debt dynamics. As an example of what happens when political risks are included, we looked at recent developments in Italy (see below).

Short-term political ambiguity and long-term uncertainty

To incorporate political risks in DSA, we were faced with the problem of uncertainty specification, which has been daunting economists for a very long time (see for example Knight, 1921, and Arrow, 1951). We needed to account for short-term ambiguity (ie which government wins the election, what policies will they implement, will a country be able to follow an adjustment programme?) and for the long-term volatility on the path towards a well-estimated expected future state, if we think that such an equilibrium state exists. In general, it is not possible to estimate reliably an election outcome or what policies a new government will pursue.

We adopted narrative scenarios for variables with ambiguous immediate outcomes, to see what the bad outcomes might be, and calibrated probabilistic scenarios for long-run uncertainty to estimate appropriate risk metrics. We ran the DSA model for a range of plausible values for the critical variables that are affected by political events, such as government surplus and country GDP growth. For the long-run risks, we calibrated scenarios of economic, fiscal and financial variables, accounting for political effects. Using this approach, we identified values for ambiguous variables with high probability of bad outcomes, so that they can be avoided. The result was a comprehensive heatmap of high-risk debt dynamics, with quantile optimisation for those aspects of the problem that are amenable to scenario calibration, and identification of narrative scenarios with bad outcomes that must be avoided, for the ambiguous aspects.

Italy as a case study

We applied our model to the 2019 budget agreement between the Italian government and the European Commission. We assessed whether Italy can stay on a non-increasing debt path with gross financing needs below an IMF-specified threshold of 20% of GDP, and demonstrated the material effects of political risks (note: our assessment criteria are less stringent than those of official DSAs).

We started with a scenario tree covering GDP growth, the primary balance and the risk-free rate of euro-area five-year AAA rated sovereigns, but without political variables. The scenario tree was calibrated to Italy’s conditions and observed market data, using historical volatilities and correlations. To the scenarios of risk-free rates, the model added premia capturing the response of borrowing rates to debt levels.

A significant short-term political risk was the fiscal stance of the new Italian government after the 2018 elections. We parametrically changed growth and primary balance projections to cover plausible outcomes, and evaluated, using the calibrated long-term scenario trees, the likelihood of debt stocks and gross financing needs staying within the thresholds. The result was a heatmap that shows the likelihood of debt dynamics remaining within the thresholds for a wide range of the ambiguous variables. We used the model to draw the heatmap and assess Italian debt dynamics under three scenarios: (i) no policy change; (ii) the new Italian government achieves its growth and surplus projections; and (iii) Italy reaches the targets in the agreement negotiated with the European Commission. We assessed if the outcomes of each scenario would violate the thresholds, and, therefore, must be avoided.

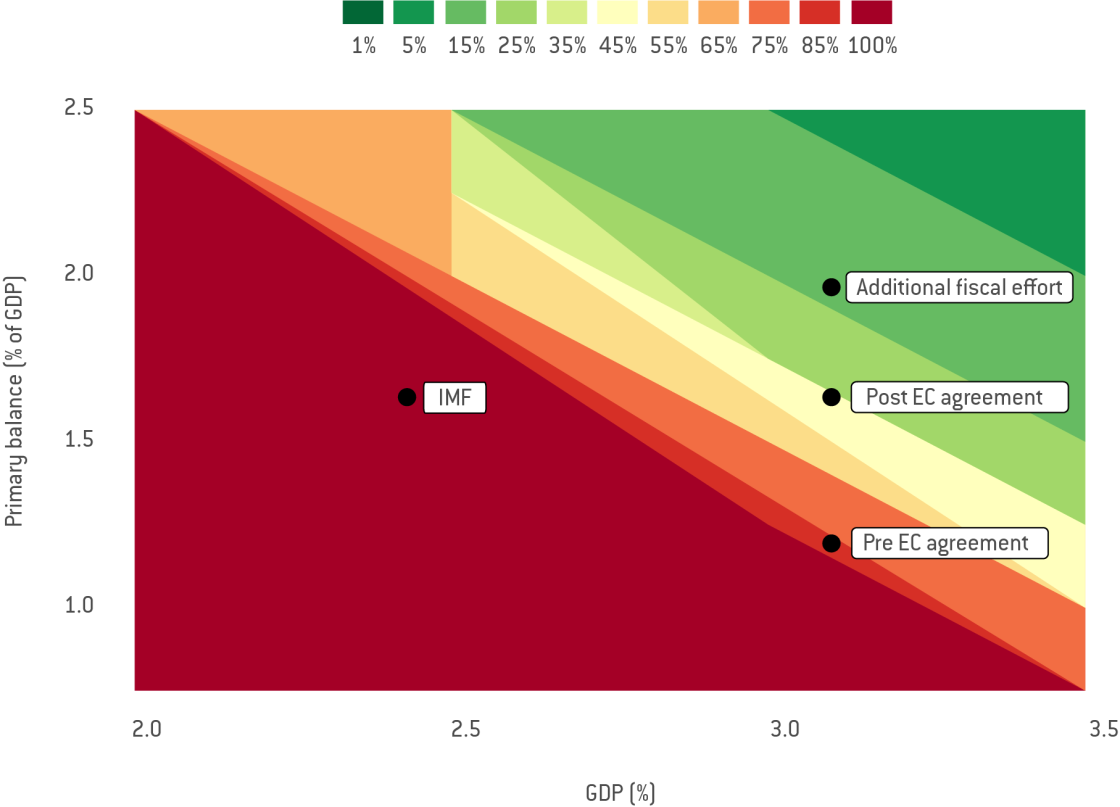

Figure 1 shows the heat map, with dark green denoting an extremely low probability (0.01) of unsustainable dynamics, and red denoting a very high probability (0.85). Note that for a wide range of combinations of GDP growth and primary balance, the dynamics are unsustainable with very high probability. Italy is clearly vulnerable. The map also locates our narrative scenarios: ‘IMF’ denotes projections from the IMF World Economic Outlook report for 2018. Under our model calibration, and without any change in policy, the debt dynamics are highly likely to be unsustainable. ‘Pre- agreement’ corresponds to the Italian government targets before the budget agreement with the European Commission. It improves on the previous policy but is still in the red zone. ‘Post-agreement’ presents further improvements, shifting Italy into the yellow zone, with a probability of 0.55 for sustainable dynamics. The wisdom of a policy with a 0.55 chance of achieving its objectives is questionable and additional fiscal effort would be needed to increase to 0.85 the probability of remaining within the thresholds (green). Using the model, we estimate that with a total fiscal effort of 3.5% of GDP over twelve years, capped at 0.3% per annum, Italy can reach this target. This finding is in agreement with Sapir (2018) that Italy should have been running a higher primary surplus consistently to avoid finding itself in its current predicament, although our estimates for the extra effort are lower.

Figure 1: Probability of Italian debt violating thresholds on debt stock or gross financing needs. Source: Authors calculations using the model of Zenios et al (2019).

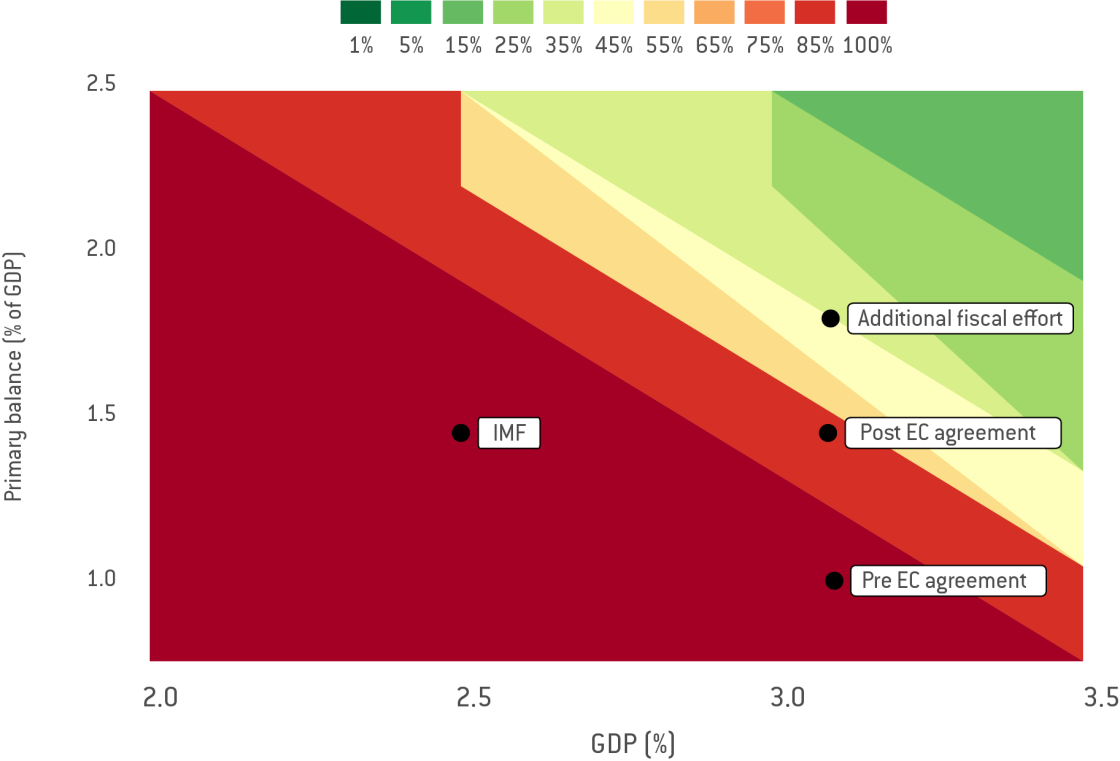

We then incorporated long-term political risks. We generated a new scenario tree with political stability and economic policy confidence state variables, calibrated to Italy’s volatile political variables around estimated long-term trends. To calibrate the political state variables, we assumed that they converge long-term to their historical averages of 4.5 (out of 10) for stability and 15.5 (out of 100) for policy. We also estimate volatilities from the historical ratings for Italy, namely a standard deviation of 1 for stability and 11 for economic policy confidence. The political variables are correlated with growth, primary balance and interest rates, with historical correlations from -0.44 to 0.75, respectively. Regression estimates of the bond yield sensitivities to these factors are then added to the refinancing costs scenarios, adjusted according to the endogenous debt risk premium. We re-ran the model including political risk premia and redrew the heatmap (Figure 2).

Figure 2: Probability of Italian debt violating thresholds on stock or gross financing taking political risks into account. Source: Authors calculations using the model of Zenios et al (2019).

From this, a marked increase in the area that denotes a high probability of unsustainable dynamics can be seen. With political vulnerabilities taken into account, more combinations of growth and primary surplus are highly likely to violate the thresholds. Under our model, the agreement with the European Commission, which was estimated to have a slightly better than 0.50 chance of success, would only have a 0.15 chance of success when political risks are accounted for. The additional fiscal effort that restores sustainability with a probability of 0.85, is now borderline light green, with a 0.65 to 0.55 chance of success. Clearly, ignoring the political risks can lead to excessive optimism and wrong decisions.

References

Arrow, K. J. (1951) ‘Alternative approaches to the theory of choice in risk-taking situations’, Econometrica 19: 404–437

Gala, V., G. Pagliardi and S.A. Zenios (2018) ‘International politics and policy risk factors’, working paper, available at https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3242300

Knight, F. H. (1921) Risk, Uncertainty, and Profit, Boston, MA: Hart, Schaffner & Marx; Houghton Mifflin Company

Sapir, A. (2018) ‘High public debt in euro-area countries: comparing Belgium and Italy’, Policy Contribution 15/2018, Bruegel

Zenios, S.A., A. Consiglio, M. Athanasopoulou, E. Moshammer, A. Gavilan and A. Erce (2019) ‘Risk management for sovereign financing with sustainability conditions’, Globalization Institute Working Paper 367, Federal Reserve Bank of Dallas, available at https://www.dallasfed.org/~/media/documents/institute/wpapers/2019/0367.pdf

[1] See, for instance, the 2018 Financial Stability Report and the 2018 Global Outlook Reports. Such references appeared 26 times in the 2016 Article IV report for Greece, 12 times in the 2018 report, and four times in 2019.

About the authors

Related content

How effective has the pandemic emergency purchase programme been in ensuring debt sustainability?

The ECB’s pandemic emergency purchase programme has improved substantially the debt dynamics of euro-area countries, with durable effects.

The risks from climate change to sovereign debt in Europe

European Union institutions and national fiscal authorities should incorporate climate risk in debt sustainability analysis.

The ripple effect of financial education

A financial literacy course for university students in Cyprus also improved the financial knowledge of their parents.

Climate change, the next big financial threat

A warming planet poses new risks to European sovereign debt. How can the continent protect itself?