Who’s (still) exposed to Greece?

Following the recent elections, Greece has come under pressure. Fear is growing about the stance of the newly elected government and there have been s

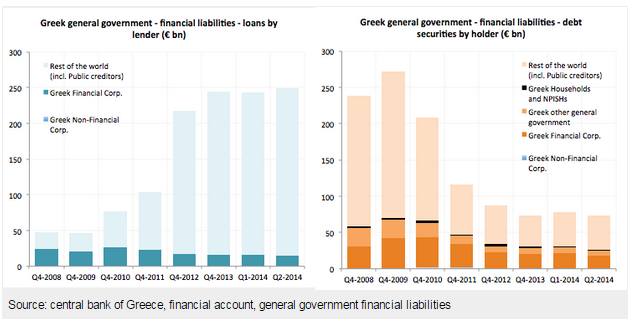

Since the start of the crisis, the structure of Greek debt has changed considerably (almost 80 percent of government financial liabilities are now accounted for by loans, against slightly less than 20 percent back in 2008). At the same time, the weight of public creditors has increased among the creditors of the government. Figure 1 shows a breakdown of the Greek general government financial liabilities across the main creditor sectors (with public creditor included in non-residents). At the end of 2013, debt due to official creditors amounted to 216 billion of loans (IMF/EU loans) and 38 billion of securities (under SMP). This means that, at the end of 2013, official creditors accounted for about 94 percent of the total loans due to non-residents and 89 percent of the total securities held by non residents.

The government is not the only Greek sector to which foreign investors are exposed

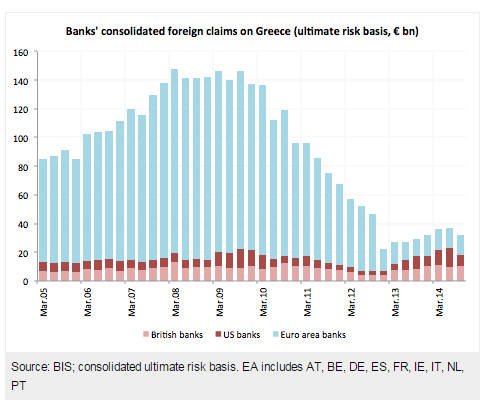

But the government is not the only Greek sector to which foreign investors are exposed, and official creditors are not the only investors in Greece. After Greece came under market pressure and eventually obtained an EU/IMF macroeconomic financial assistance programme in 2010, foreign banks started to rapidly reduce their exposure to Greece (figure 2). Euro area banks’ consolidated foreign claims on Greece – which peaked at about 128 billion euro in 2008 – reached a low of about 12 billion euro in September 2013. UK banks’ exposure reached a peak of 13 billion in March 2008 and dropped to 4.3 billion in December 2012. US banks’ exposure instead was about 14 billion in September 2009 and down to 2.5 billion at the end of 2012.

Interestingly, the only country where banks have been continuously increasing their exposure to Greece since 2013 is Germany

Interestingly, US and UK banks have been increasing their Greek exposure again, since March 2013, reaching back to levels not very far from those of end 2009 /early 2010. US banks’ exposure to Greece as of September 2014 was in fact 8 billion (down from 13 billion in June) and UK banks’ exposure was 10 billion. Euro area banks have behaved very differently and total exposure to Greece has in fact continued to decline in almost all countries. Even more interestingly, the only country where banks have been continuously increasing their exposure to Greece since 2013 is Germany. German banks’ foreign claims on Greece in fact reached 32 billion in March 2010, dropped to as low as 3.9 billion at the end of 2012 and went back to around 10 billion in June 2014. Therefore the recent increase is small compared to the historical level, but it has been continuous (at least until September 2014).

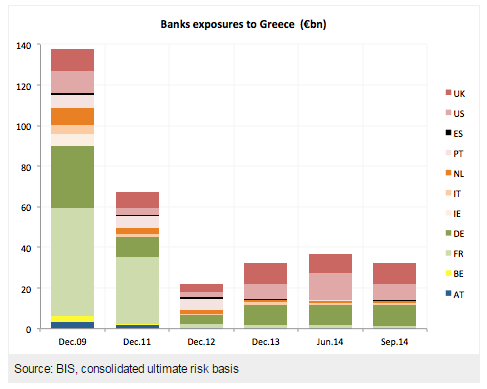

As of the latest available data (September 2014), euro area banks’ exposures to Greece amounted to 96.6 million for Austria, 29.4 million for Belgium, 1368 million for France, 10203 million for Germany, 55.9 million for Ireland, 800 million for Italy, 923 million for the Netherlands, 263 million for Portugal and 301 million for Spain.

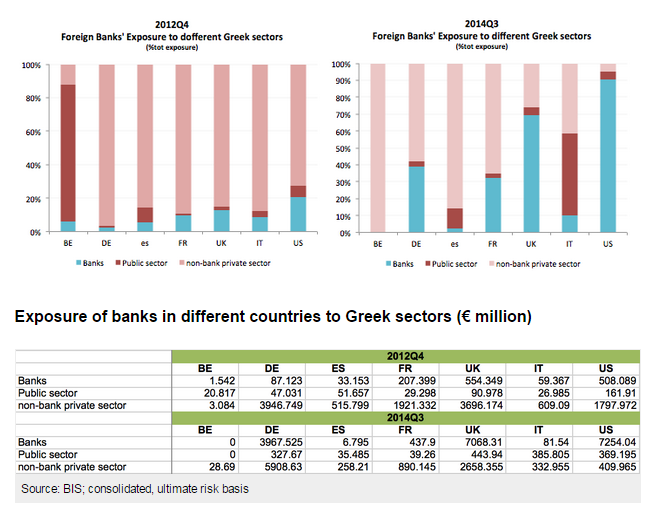

The composition of such exposures, however, varies across countries and has significantly changed over time. Figure 3 compares the exposure of selected foreign banks to Greek sector as of september 2014 versus December 2012 (chosen as a starting point because so that comparison is made between two post-PSI dates).

In 2012, exposures to the Greek private non-financial sectors accounted for the largest share of banks’ exposure to the country, with the exception of Belgian banks. In 2014, exposures to Greek banks have significantly increased as a share of total exposures in all countries but for Belgium and Spain. In terms of absolute numbers, only Belgium and Germany have increased their exposure to the Greek private non-financial sector. In absolute numbers, also exposure to the public sector has increased everywhere (apart from Belgium), but the only country where public exposure has significantly increased as a share of the total is Italy.

Since 2012, private investors have been timidly and slowly coming back to Greece

Anybody who has followed the development of the euro crisis knows about the important increase in the weight of public creditor for Greek government debt. The data show, however, that since 2012 (when the ECB introduced the OMT programme) private investors have been timidly and slowly coming back to Greece. While exposures of euro area banks are still at very low levels compared to the pre-crisis period, it is tempting to interpret this as a first trace of normalisation and a resumption in confidence, which the present political turmoil risks reverting.

Read our special Eye on Greece section

This article was republished in italian on lavoce.info

About the authors

Related content

GNI-per-head rankings: The sad stories of Greece and Italy

No other country lost as many positions as Greece and Italy in the rankings of European countries by Gross National Income per head, between 1990 and

After the ESM programme: Options for Greek bank restructuring

With the end of the Greece support programme, authorities now have scope to focus on the legacy of NPLs and excess private-sector debt. Two wide-rangi

What will it cost the European Union to pay its economic recovery debt?

Servicing the EU debt until 2058 seems feasible, despite increased borrowing costs, but member countries must make choices about budget funding

ΕΥΡΩΕΚΛΟΓΕΣ ΚΑΙ ΤΟ ΜΕΛΛΟΝ ΤΗΣ ΕΥΡΩΠΗΣ

Είναι γεγονός ότι οι τωρινές εκλογές λόγω της ανάπτυξης των κομμάτων του λαϊκισμού είναι κάπως διαφορετικές από τις προηγούμενες. Αλλά πιστεύω ότι όλε